Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

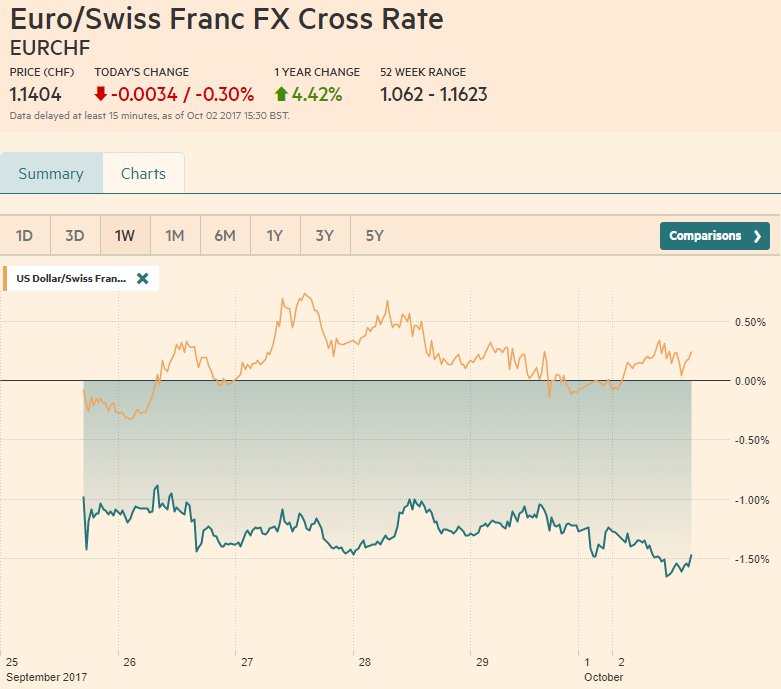

Swiss FrancThe Euro has fallen by 0.30% to 1.1404 CHF |

EUR/CHF and USD/CHF, October 02(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is broadly higher as the quarter-end positioning losses seen at the end of last week area reversed. Developments in the US are seen as dollar positive, while the Catalonia-Madrid conflict, and slightly softer EMU manufacturing PMI weighs on the euro. The UK also reported a disappointing manufacturing PMI, and more differences with the Tory government are taking a toll on sterling. Japan’s Tankan Survey was stronger than expected, but the rise in US Treasury yields and the LDP’s slippage in the opinion polls has seen the greenback return to JPY113 from a JPY112.20 low before the weekend. US 10-year yield reached nearly 2.37% earlier today, its highest level in 2.5 months. The focus on US tax cuts and the heightened speculation that Warsh could be the next Fed chair are factors thought to be lifting yields. We suspect the market may be jumping to a conclusion about Warsh, as he is just one of several candidates under consideration. |

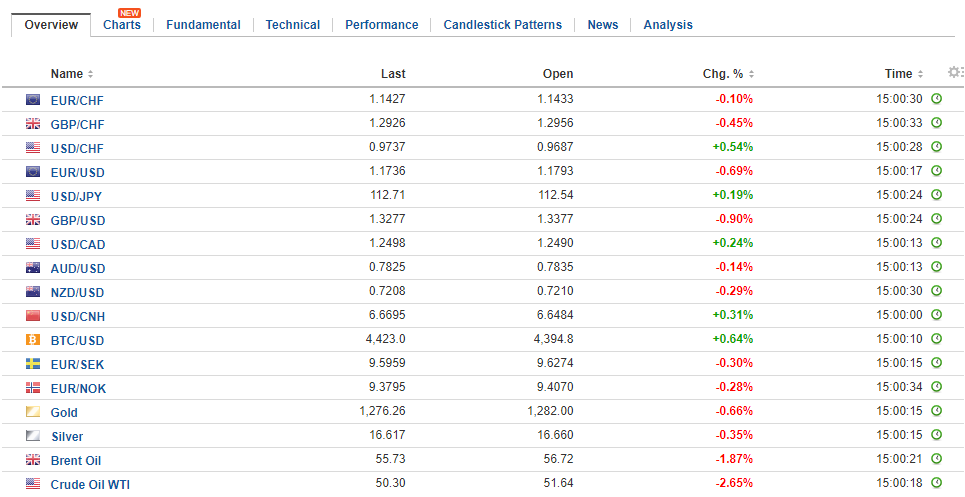

FX Daily Rates, October 02 - Click to enlarge |

| We had thought odds of Yellen;s reappointment was higher than the market had seemed to believe, but the betting markets have adjusted. We think that given the nearly complete turnover among the Board of Governors, there is pressure for some continuity and preservation of institutional memory. In this respect, perhaps Governor Powell, the remaining Republican-appointee on the Board, may be the compelling alternative to Yellen.

We remain impressed that the market’s new found confidence in a Fed hike in December was not shaken by the disappointing core PCE deflator seen before the weekend. The Fed funds have been steady at 1.16% for the effective average since the June hike. Assuming no chance of a hike in November, and If an allowance is made for the end of the December, where the effective average Fed funds rate would slip 10 bp for the last three days of the month (Friday, Saturday, and Sunday), then fair value for the December contract IF the Fed were to hike would be about 1.29%. The implied yield is 1.255% presently, or a nearly 72% chance of a hike has been discounted. In the CME’s interpolation, there is a nearly 77% chance of a hike priced in, while Bloomberg’s calculation puts it at nearly 70% chance. |

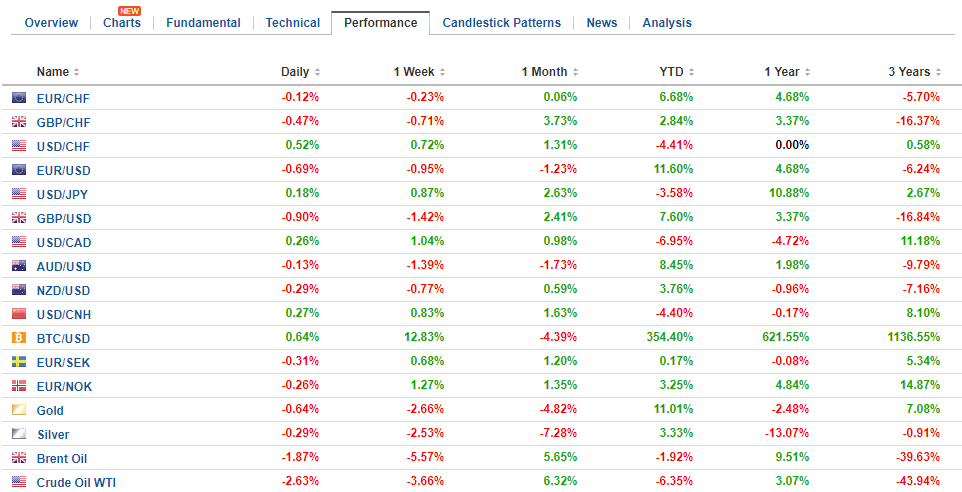

FX Performance, October 02 - Click to enlarge |

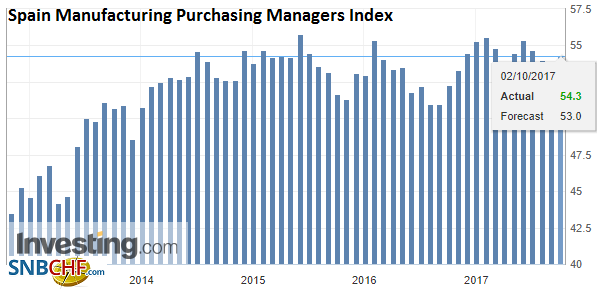

SpainSpain’s assets are underperforming in the wake of the weekend conflict between the Catalonians seeking to participate in an independence referendum that the Spanish Supreme Court ruled was illegal. The tragedy lies in both sides pursuing their interest. It seems easy for journalists and many other observers to express sympathy for the Catalonians, but few would be as supportive if it were happening in their own country. Of course, the violent treatment of the illegal voters is not only reprehensible, but it is also counter-productive. At the same time, the national government cannot simply stand may and see 20% of its economy be severed. What did the US do when parts of the South took the 1860 election as a referendum on independence? What would Germany do if Bavaria threatened to have an independence referendum? There are other parts of Spain that are watching to see if they can strike out as well. The northern part of Italy will hold a referendum soon as well. Spanish shares are off more than 1.2%, with financials down nearly twice as much. Materials and healthcare are the only two sectors gaining today. The Dow Jones Stoxx 600 is up about 0.25%. Of note, the DAX gapped higher after gapping higher before the weekend. It is within 0.5% of the record high seen in June. Spanish 10-year bond yield is up seven bp, nearly twice the increase seen in Italy today. Core bond yields are little changed. |

Spain Manufacturing Purchasing Managers Index (PMI), Sep 2017(see more posts on Spain Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

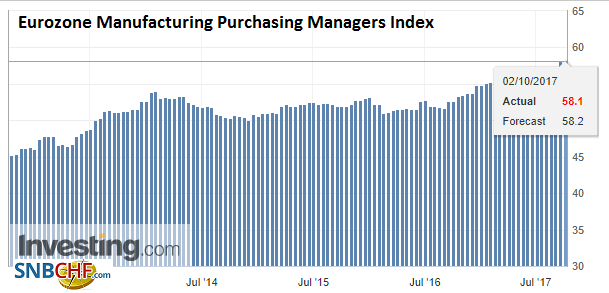

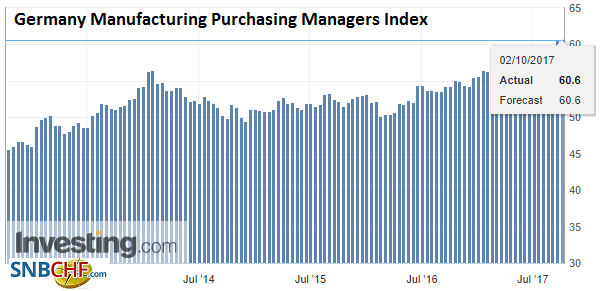

EurozoneThe eurozone manufacturing PMI came in a smidgen below the 58.2 flash reading at 58.1. This still represents an increase from the 57.4 reading in August, and it suggests the regional economy finished Q3 with positive momentum. Germany’s report confirmed the flash reading of 60.6. |

Eurozone Manufacturing Purchasing Managers Index (PMI), Sep 2017(see more posts on Eurozone Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

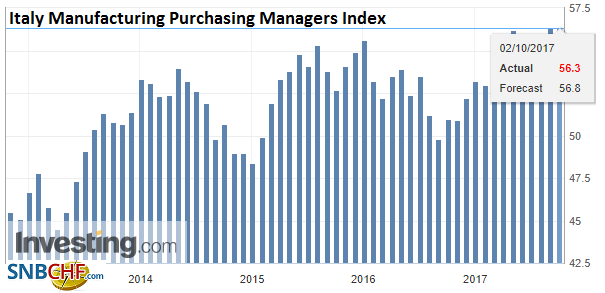

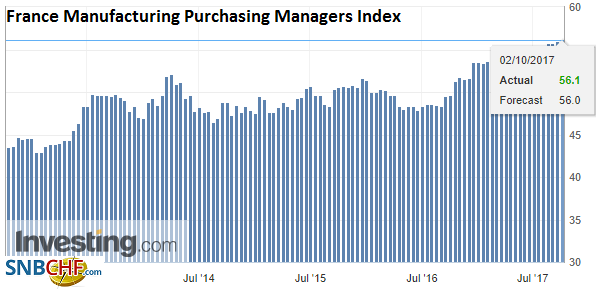

| France ticked up to 56.1 from the 56.0 flash and the 55.8 in August. Spain’s manufacturing PMI surprised on the upside at 54.3 from 52.4 It snapped a three-month decline and is the highest reading since June. Italy disappointed with an unchanged 56.3 reading. The median forecast had expected a modest increase. |

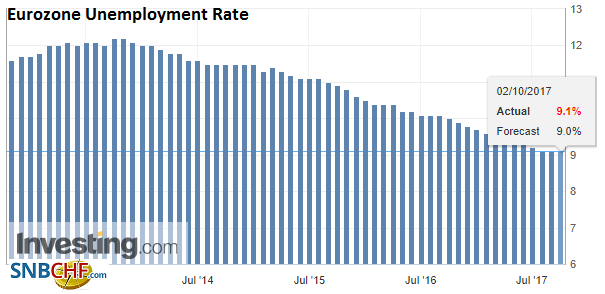

Eurozone Unemployment Rate, Aug 2017(see more posts on Eurozone Unemployment Rate, ) Source: Investing.com - Click to enlarge |

United KingdomThe UK also disappointed. The manufacturing PMI slipped to 55.9 from a revised 56.7 reading in August. It had originally been reported at 56.9. The decline was larger than expected. The UK reports the construction PMI tomorrow and the services PMI on Wednesday. Despite today’s report and the outright contraction in July services consumption reported before the weekend, the market remains heavily leaning to a November rate hike. Interpolating from the OIS suggests around an 80% chance of a hike then. The implied yield on the December Short Sterling futures contract is 53.5 bp and the peak last month was 56 bp. |

U.K. Manufacturing Purchasing Managers Index (PMI), Sep 2017(see more posts on U.K. Manufacturing Purchasing Managers Index, ) Source: Investing.com - Click to enlarge |

Italy |

Italy Manufacturing Purchasing Managers Index (PMI), Sep 2017 Source: Investing.com - Click to enlarge |

France |

France Manufacturing Purchasing Managers Index (PMI), Sep 2017 Source: Investing.com - Click to enlarge |

Germany |

Germany Manufacturing Purchasing Managers Index (PMI), Sep 2017 Source: Investing.com - Click to enlarge |

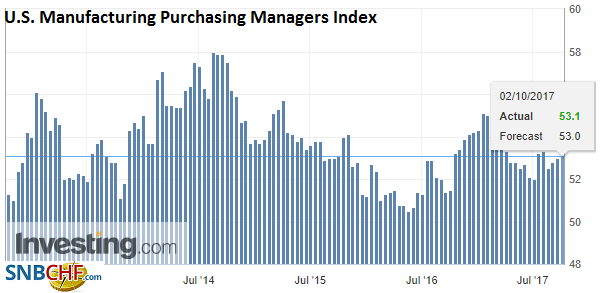

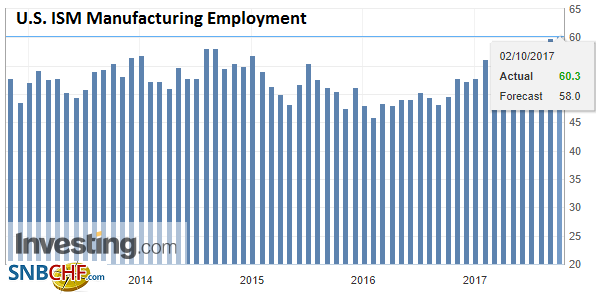

United States |

U.S. Manufacturing Purchasing Managers Index (PMI), Sep 2017 Source: Investing.com - Click to enlarge |

U.S. ISM Manufacturing Employment, Sep 2017(see more posts on U.S. ISM Manufacturing Employment, ) Source: Investing.com - Click to enlarge |

|

U.S. ISM Manufacturing Purchasing Managers Index (PMI), Sep 2017 Source: Investing.com - Click to enlarge |

Japan’s Tankan Survey showed sentiment among large manufacturers is at its best level in a decade. Sentiment was generally firm. However, there were a couple of disappointing elements. First, despite the optimism capex plans were shaved to 7.7% from 8.0%. Second, the large companies expect the dollar to average JPY109.29 in the fiscal year ending March 2018. So far, it is averaging a little above JPY111 during the fiscal year. However, it may be better to understand this not as a forecast but more revealing something closer to their internal hedges. That interpretation is consistent with our discussions suggesting that Japanese businesses have not a problem with JPY110.

The dollar looks set to trade between two large option strikes that are to expire today. One is struck at JPY112.50 ($850 mln), and the other struck at JPY113 ($470 mln). There does not appear to be significant nearby strikes for the euro, but there is a large (~1.6 bln euros) struck at $1.1770 that expires tomorrow.

Last week’s low in the euro was set near just above $1.1715. We suggest the topping pattern that has been carved points to a move toward $1.1600, with the mid-August lows near $1.6660 offering intermittent support. While the near-term technical readings are stretched, we see the medium term technicals at their strongest for the dollar for many months. Sterling has been driven below the 20-day moving average and may close below its for the first time since late-August. With today’s break, it has retraced more than 61.8% of the rally spurred by the BOE’s hawkishness and is through the 38.2% retracement objective since that late August low (~$1.3320). The next area of support is seen near $1.3220. The low from the day the BOE met was near $1.3155.

The dollar-bloc currencies are also under pressure. The US dollar is moving through CAD1.25. Support is now pegged near CAD1.2420 and potentially extends toward CAD1.2600 near-term. The Australian dollar is flirting with support at $0.7800. It has been frayed, and the corrective upticks have been limited. A convincing break would be a bearish technical development and project toward $0.7600, with an initial target near $0.7730.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF,Eurozone Manufacturing PMI,Eurozone Unemployment Rate,France Manufacturing PMI,Germany Manufacturing PMI,Italy Manufacturing PMI,Japan Manufacturing PMI,newslettersent,Spain Manufacturing PMI,U.K. Manufacturing PMI,U.S. ISM Manufacturing Employment,U.S. ISM Manufacturing PMI,U.S. Manufacturing PMI,USD/CHF