| S&P futures rose 0.1% on the last trading day of the month, trailing European and Asian markets boosted by China’s July Mfg. PMI, which despite declining from from 51.7 to 51.4, and missing expecations of 51.5, saw the construction index rise to its highest level since December 13, sending Chinese iron ore futures surging and the European commodity sector broadly higher.

In equities, the MSCI All-Country World Index advanced 0.1%, and the MSCI Emerging Market Index increased 0.3%, while MSCI’s broadest index of Asia-Pacific shares outside Japan reversed early losses to rise 0.25%. Stocks have rebounding from Friday’s selloff spurred by raw-material producers on “optimism the global economy is gathering momentum” amid “evidence points to resilient global growth, with investors assessing numbers from the world’s top three economies” according to Bloomberg. As noted above, China’s official factory gauge showed continued expansion in June, even as it slipped amid government efforts to curb financial risks. Japan’s industrial output expanded in June, while data Friday showed the U.S. economy accelerating in the second quarter. Investors remained wary after North Korea conducted a missile test late on Friday that it said proved its ability to strike the U.S. mainland. The U.S. responded by flying two bombers over the Korean peninsula on Sunday. But early jitters dissipated somewhat, with the Korean won reversing losses. The dollar was down 0.2 percent at 1,120.7 won, after jumping almost 0.7% on Friday. South Korea’s KOSPI fell 0.2%. |

IOEU7 COMB Comdty, Jul 2017 - Click to enlarge DCE Iron ore futures +6.43% pic.twitter.com/z7TDGWHOkQ — Sunchartist (@Sunchartist) July 31, 2017 |

| “The geopolitical overhang will likely keep topside moves in check early in the week as the disorganized U.S. and China policy towards North Korea is not helping matters,” Stephen Innes, head of Asia-Pacific trading at OANDA, wrote in a note.

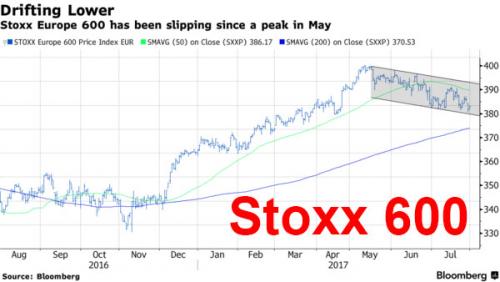

In Europe, Anglo American, Rio Tinto Plc and BHP Billiton helped underpin the advance in the Stoxx Euro 600 Index as miners also propelled the MSCI All Country World Index toward a ninth month of gains. HSBC shares jumped as much as 3.7% to the highest since November 2014 on a $2 billion buyback as profit rose. Shares have climbed 26% this year, with the lender accounting for 13% of Hang Seng Index’s 24% YTD gain, most after Tencent. Despite today’s 0.3% gain, the Stoxx 600 is flat for the month of July, in contrast with a gain of 2% for S&P 500 over the same period, according to Bloomberg. European stocks have been hurt by a strengthening euro which has fueled concerns for European earnings. |

Stoxx Europe, Aug 2016 - 2017 - Click to enlarge |

| “Global expansion dynamics are well underway,” analysts at Candriam Investors Group wrote in a report. “The European recovery is well on track and is leading to above-trend growth in 2017-18. This has led us to increase our profit earnings expectations for euro-zone equities. The economic news flow is starting to become more supportive in the U.S., while emerging markets are benefiting from a good economic momentum.”

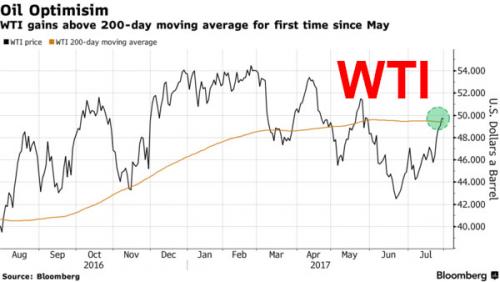

There is however, a latent risk: as Citi notes, political headlines may manifest themselves “the proposed healthcare bill is on life-support, tax reform is back in the news (though not yet on the table), and we await further reaction from the Trump administration to the diplomatic spat with Russia and to North Korea’s latest missile test – which, according to Korean newswires, may be imminently followed by another launch.” A quick look at the FX book shows the Canadian dollar is biggest loser within G-10, while the yen and euro are mixed. Sovereign yields are near unchanged with the T-note yield at 2.29%. Asian stocks are broadly higher led by Australia and China. Chinese shares rose 0.6%, buoyed by several leading companies’ forecasts for strong mid-year earnings. The blue-chip index and the Shanghai Composite both rose 0.6 percent. Japan’s Topix index closed 0.2 percent lower after swinging between gains and losses. Australia’s S&P/ASX 200 Index rose 0.3 percent and South Korea’s Kospi index added 0.1 percent. Hong Kong’s Hang Seng Index added 1.1 percent. HSBC was among the biggest contributors to the advance (more below). West Texas crude traded above $50 a barrel for the first time since May, while copper rose to a two-year high and iron ore surged. |

WTI Price and WTI 200-day Moving Average, Aug 2016 - 2017 - Click to enlarge |

In the Asian session, the dollar index climbed with gains tempered by tensions over the weekend between U.S. and Russia, as wells as North Korea. In Europe, Euro, EGBs largely unchanged as euro area July inflation matches estimates. Pound slips against dollar. The Bloomberg Dollar Spot Index edged higher, paring its fifth straight month of declines, as investors prepare for a data-heavy week that will culminate with the release of non-farm payrolls data for July, while Apple, Pfizer, Tesla and Berkshire Hathaway will report earnings. The euro began the week on a soft note as investors waited for second-quarter growth data due Tuesday. The Swiss franc was little changed against the euro, after posting its biggest weekly decline in more than two years; last week’s selloff was triggered by a host of factors, including stop losses and talk of initial public offer-related flows. The ruble slid 1.2% to 60.2550 per dollar, falling for a third day and the most among emerging-market currencies amid heightened geopolitical risks after Russia ordered expulsion of U.S. diplomats. Russian government bonds fell, driving the 10-year yield higher by 9bps.

Also overnight, the BOJ maintained its govt bond purchase plans for August unchanged from July. Below are Bloomberg’s comparisons between planned purchase ranges for August against those for July and the amounts BOJ offered to buy at the last operations:

- 1-to-3 years: 200b-300b yen vs 200b-300b yen for July, 280b yen on July 28

- 3-to-5 years: 250b-350b yen vs 250b-350b yen for July, 330b yen on July 28

- 5-to-10 years: 350b-550b yen vs 350b-550b yen for July, 470b yen July 28

- 10- to-25 years: 150b-250b yen vs 150b-250b yen for July, 200b yen on July 26

- More than 25 years: 50b-150b yen vs 50b-150b yen for July, 100b yen on July 26

- Up to 1 year: 50b-150b yen vs 50b-150b yen for July, 100b yen on July 26

U.S. crude futures climbed 0.3 percent to $49.87 a barrel, after earlier hitting $50.06, their first foray above $50 in two months. Brent crude advanced 0.5 percent to $52.78, adding to Friday’s 2 percent surge. Gold was little changed at $1,268.26 an ounce, after earlier climbing to its highest since June 14.

In rates, the yield on 10-year Treasuries advanced less than one basis point to 2.29%. Germany’s 10-year yield climbed one basis point. Britain’s 10-year yield fell less than one basis point.

Copper climbed 1.1 percent to $2.91 a pound, the highest in more than two years. Zinc gained 1.1 percent, nickel 0.7 percent and tin 1 percent Gold fell 0.2 percent to $1,266.98 an ounce after rising to $1,271.23, the highest since June 14. Gold remains on course for its biggest monthly advance since Feb., with prices trading near highest level in more than six weeks, as speculation that Federal Reserve will go slow on raising interest rates hurts dollar. Bullion for immediate delivery +2.2% this month, most since Feb.’s +3.1%. “U.S. GDP data was weaker than expected and inflation remains subdued, which could damp Fed rate hike expectations,” Guotai Junan Futures says in note. “Gold has scope to rise further in the near term.”

Markets are awaiting speeches by Cleveland Federal Reserve President Loretta Mester and San Francisco Fed President John Williams on Tuesday, for further insight into whether the central bank has turned more dovish in light of recently muted inflation.

“It is easy for uncertainty to increase about the Fed’s ability to raise rates next year if inflation remains low. We could see the dollar head below 110.00 yen under such circumstances,” said Junichi Ishikawa, senior forex strategist at IG Securities in Tokyo.

The slew of corporate earnings continues. Apple Inc., Tesla Inc., Berkshire Hathaway Inc. and Toyota Motor Corp. are all set to unveil results this week. Pending home sales and Dallas Fed manufacturing activity is expected later on Monday, along with earnings reports from Stifel Financial, Loews and others.

Overnight Bulletin Summary from RanSquawk

- European equities trade higher with outperformance in the FSTE (+0.4%) amid gains in HSBC

- USD-index has regained some ground against majors, while EUR inflation data saw the headline meet expectations

- Looking ahead, highlights include Chicago PMI and Pending Home Sales

Market Snapshot

- S&P 500 futures up 0.11% to 2,473.00

- STOXX Europe 600 up 0.3% to 379.46

- MXAP up 0.3% to 160.20

- MXAPJ up 0.4% to 529.01

- Nikkei down 0.2% to 19,925.18

- Topix down 0.2% to 1,618.61

- Hang Seng Index up 1.3% to 27,323.99

- Shanghai Composite up 0.6% to 3,273.03

- Sensex up 0.5% to 32,479.54

- Australia S&P/ASX 200 up 0.3% to 5,720.59

- Kospi up 0.07% to 2,402.71

- US 10Y yield +0.35bps to 2.29%

- German 10Y yield unchanged at 0.541%

- Euro down 0.2% to 1.1726 per US$

- Italian 10Y yield rose 2.7 bps to 1.829%

- Spanish 10Y yield fell 3.1 bps to 1.494%

- Brent Futures up 0.2% to $52.61/bbl

- WTI up 0.2% to 49.80/bbl

- Gold spot down 0.3% to $1,266.39

- U.S. Dollar Index up 0.3% to 93.51

Top Overnight News

- Inflation in the euro area remained well below the European Central Bank’s goal as policy makers prepare to discuss unwinding stimulus.

- After the collapse of Obamacare repeal, Republicans may have to choose between pursuing another health bill or pushing through a tax overhaul this year, because there’s almost certainly not enough time to do both.

- So how much did it end up taking after European Central Bank President Mario Draghi memorably said five years ago he’d do “whatever it takes” to save the euro? About 1.2 trillion euros.

- The Saudi-led alliance that severed ties with Qatar reinstated a list of 13 demands that must be met before talks to resolve the eight-week crisis could start, just as as fresh economic data highlighted the impact of the unprecedented boycott on the Gulf nation.

- Trump’s New Chief Has One Key Asset: Ivanka and Kushner’s Nod

- Trump Hints Ending Subsidies to Insurance Cos if No Bill Passed

- SoftBank Is Said to Plan Making Direct Offer for Charter; Charter Says Has No Interest in Acquiring Sprint

- India Needs 2,100 Planes Worth $290b in 20 Years, Boeing Says

- Astra’s Imfinzi Granted FDA Breakthrough Therapy in Lung Cancer

- J&J Granted FDA Orphan Drug Status for Bedaquiline

- Ford Takes Action to Help Address Concerns of First Responders

- Five Banks Reach $111.2m Total Pact Over FX case, Law Firm Says

- Lockheed Lands $3.69B Advance to Build 50 F-35s for Int’l Buyers

- Alaska Air Says Hacker Accessed Virgin America Worker Passwords

- Koch Network Readies Push for Lower Taxes After Border Tax Kill

- Raytheon’s Troubled GPS III Ground Control Network Slips Again

Asia equity markets traded mixed ahead of this week’s key risk events and as participants digested Chinese Manufacturing PMI and further provocation from North Korea. ASX 200 (+0.4%) was underpinned by commodity names amid strength in the metals complex coupled with WTI crude’s brief reclaim of USD 50/bbl to the upside, while Nikkei 225 (-0.2%) was dampened by broad-based JPY strength. Geopolitical concerns pressured the KOSPI (-0.3%) following another North Korean missile test on Friday which it claimed was capable of striking mainland US, while both Hang Seng (+1%) and Shanghai Comp. (+0.6%) were positive despite Official Chinese Manufacturing PMI data missing estimates, as the Construction sub-index rose to its highest since December 2013. Finally, 10yr JGBs were flat and failed to benefit from the cautious risk tone in Japan, with demand subdued following a lacklustre BoJ Rinban announcement valued at just only JPY 325b1n of JGBs. PBoC injected CNY 160 bin 7-day reverse repos and CNY 80bln 14-day reverse repos. Chinese Official Manufacturing PMI (Jul) 51.4 vs. Exp. 51.5 (Prey. 51.7). Chinese Non-Manufacturing PMI (Jul) 54.5 (Prey. 54.90)

Top Asian News

- China Is Said to Ask Waldorf Owner Anbang to Sell Assets Abroad

- BOJ Keeps August Bond Purchase Ranges Unchanged From July

- Biggest Indian Bank Surges as Deposit Rate Cut May Boost Profit

- Sumitomo Mitsui 1Q Net Income Rises 31% to 241.5b Yen

- SMFG Reports 1st Qtr Group Earnings Result

- Panasonic Reports 1st Qtr Group Earnings Result (IFRS)

- Tian Guoli Is Said to Be Named China Construction Bank Chairman

European bourses are higher across the board this morning led through material names, following the Chinese Mfg. PMI data, in which the construction index rose to its highest level since Dec’13. Firm earnings and an announcement to plan a USD 2bln share buyback from Europe’s largest bank, HSBC (+3%), has lifted financial names higher this morning with support for health care names also seen in the wake of earnings from Sanofi (+1.8%) whereby the Co. also raised their guidance. A cautious start was initially seen for German paper this morning ahead of this morning’s Eurozone CPI data with prices relatively unreactive to the release which saw the headline match expectations with core slightly firmer than anticipated. Peripheral debt outperforming its German counterpart with the BTPSs and Bonos tighter by 3bps. Some suggest BTPs are set to benefit from large month-end extensions.

Top European News

- U.K. Consumer Borrowing Cools After Bank of England Warning

- HSBC Rises as Second Quarter of Growth Backs Turnaround Story

- Putin Says Hopes Retaliation Ends Once 755 U.S. Staff Ousted

- Rolls- Royce Shares Fall; Is Said to Caution on Cash Flow to FT

- Greece’s Road to Bailout Exit: 140 Reforms Down, More to Go

- U.K. Takes Two Steps Forward, One Step Back on Brexit Plan

- Italian Unemployment Declines; Jobs Growth Led by Temporary Work

In currencies, the USD-index begins the week slightly firmer, rising 0.1% overnight to pull off 15-months lows reached last week amid a raft of soft US data. USDCAD has been the notable mover with bargain hunting the likely catalyst, given Friday’s 1% decline. Major support lies around 1.2400 with the pair testing stalling at 1.2410¬20 multiple times last week. The antipodeans (AUD,NZD) will be in focus this week, both currencies slightly tailing off their 2Y highs. Last week, AUD reached the highest level since May’15 at 0.8066, however the currency has pulled off somewhat with the Aussie back below 0.80. Focus will be on the RBA statement, in which the central bank may sharpen their language on the AUD to temper its recent surge. NZD hovers above 0.75 with participants likely to keep an eye for latest GDT auction and jobs data which will guide price action. Cable: Another central bank to announce their latest decision will be the BoE who will announce their latest economic projections. It is likely the central bank will keep rates unchanged with inflation cooling to 2.6% in June and growth remaining tepid, this has subsequently reduced speculation over a near term rate rise. Since the last meeting, GBP has risen over 3% with the currency now above 1.31. Resistance ahead at 1.3150-60 with additional offers situated at 1.32 (option barrier level).

In commodities, Brent and WTI futures up a nudge this morning, the latter met resistance at USD 50. Over the weekend, Shell’s Pernis oil refinery had been forced to close after reports of a fire at the 404k bpd refinery. Also, source reports indicate the US could announce oil related sanctions on Venezuela as soon as today in a response to Sunday’s election. Industrial metals supported overnight from the Chinese PMI data, which saw Dalian iron ore futures hitting limit up in Asia, while steel rebar soared to a 3Y high. US could announce oil related sanctions on Venezuela as soon as today in a response to Sunday’s election, according to sources. Sources added that US is considering banning sales of US oil and refined products to Venezuela, but are not expected to include a ban on Venezuelan oil shipments to the US.

Looking at today’s session, we will get the Chicago PMI number (60 expected; 65.7 previous), the Dallas Fed manufacturing activity reading (13 expected; 15 previous) for July and June pending home sales (1% expected).

US Event Calendar

- 9:45am: Chicago Purchasing Manager, est. 60, prior 65.7

- 10am: Pending Home Sales MoM, est. 1.0%, prior -0.8%; NSA YoY, prior 0.5%

- 10:30am: Dallas Fed Manf. Activity, est. 13, prior 15

DB’s Jim Reid concludes the overnight wrap

Welcome to the last day of July and the end of one life and start of a new one split between work and childcare, with nothing much in between. It’s likely that August will see a barbell of excitement with decent activity at either end but with a notable slowdown in the middle. This week we see the monthly PMIs/ISMs over the next couple of days which are a crucial barometer on realtime growth momentum, the BoE on Thursday (probably a lower key event after recent inflation numbers) and then payrolls on Friday which is always fun! Then a likely lull for 2-3 weeks before the Jackson Hole Symposium on August 24-26th with guest star Mr Draghi present for the first time since he attended and strongly hinted at QE three years ago. Will he tee-up further autumnal tapering and create some bond volatility?

We saw a little bit of bond vol on Friday after stronger German CPI (HICP 1.5% yoy vs 1.4% expected) saw 10 year Bunds climb from 0.53% to 0.58% in the morning session where they stayed until a slightly weaker than expected US Q2 GDP print (2.6% vs 2.7% annualised QoQ expected) helped see them reverse course again to close at 0.54%.

The US GDP print still represented a significant pick up from Q1 growth but that was revised down from 1.4% to 1.2%. The growth rebound was bolstered by strong Q2 consumer spending data that was in line with expectations at +2.8% SAAR (vs. +1.9% previous). Later in the day we got the final University of Michigan consumer sentiment reading for July which was revised marginally higher from 93.2 to 93.4.

This morning, China’s July manufacturing PMIs were a tad softer than expectations at 51.4 (vs. 51.5 expected; 51.7 previous), partly due to adverse weather conditions such as high temperatures in parts of China and floods in others as well as routine maintenance in some enterprises. There was also a small fall in the non-manufacturing PMI to 54.5 (54.9 previous). Focus will turn to the extent of economic growth in 2H, as China’s policy makers had previously indicated a preference for slower credit growth. Elsewhere, Japan’s industrial production for June beat expectations at 1.6% mom (vs. 1.5% expected; -3.6% previous). This morning in Asia, Chinese related bourses have all strengthened, with the Hang Seng (+0.7%) and the three Chinese markets up ~+0.6%. The Nikkei (-0.1%) and the Kospi (-0.3%) are both marginally weaker.

Global equity markets were on the softer side on Friday as US equities (S&P -0.1%; NASDAQ -0.1%) mostly dipped on the slightly lower than expected Q2 growth. However the Dow bucked the global trend to climb 0.16% (supported by solid results from Chevron) and to another new record close – the third day in a row. Earlier European equities (STOXX -1.0%) struggled as the Euro strengthened on the day and auto makers continue to weaken. Tobacco stocks fell heavily on both sides of the Atlantic as news filtered through that the US Food & Drug Administration plans to look at regulating nicotine levels in cigarettes. Across the region, other markets also softened, with the DAX (-0.4%), FTSE 100 (-1%), CAC (-1%) and FTSE MIB (-0.9%).

Over in government bonds, change in yields were modest for both US Treasuries (2Y: unch; 10Y: unch) and German Bunds (2Y: -1bp; 10Y: +1bp). Other sovereigns also had modest changes, although yields at 10Y slightly increased, while 2Y yields were marginally lower, with Gilts (2Y: -1bps; 10Y: +1bps), OATs (2Y: -1bps; 10Y: +1bps) and BTPs (2Y: +1bps; 10Y: +3bps).

Turning to currency, the US dollar index fell 0.6% on the back of softer Q2 GDP data, but has recovered a little this morning. The Euro/USD strengthened 0.6% to a new 30-month high of 1.175 and Sterling/USD was also up 0.5% to a fresh 10 month high. Commodity markets saw another day of strong performance, with the energy segment broadly higher on the day as oil rose again (WTI +1.4%) to end the week up over 8%. Precious metals were broadly higher (Gold +0.8%; Silver +1.0%), while industrial metals were slightly lower (copper: -0.3%; Aluminium -0.4%). Agricultural commodities were broadly higher on the day as well.

Away from the markets, voting efforts to repeal Obamacare have ended for now. Despite being health stricken, Senator McCain flew in last week to allow the senate to start the debate on healthcare legislation. In the end, it was McCain and two other senators that blocked the skinny repeal of Obamacare on a vote of 49-51 last Friday. Senate majority leader McConnell said “he’ll move on to other legislative business”, but Trump is not giving up, tweeting “…if a new HealthCare Bill is not approved quickly, BAILOUTS for Insurance Companies….will end very soon!” Trump is referring to ending subsidy payments to health insurance companies which help make insurance accessible to poorer Americans. The next payment is due 21 Aug and the Health and Humans Service Secretary Price has said on Sunday that “no decision (on the subsidy) has been made” either way.

The North Korean situation will also be giving Mr Trump some headaches after the state fired off more intercontinental missiles over the weekend. China has condemned the latest tests, but fell short of more aggressive actions as desired by Mr Trump. Conversely, the US has sent bombers to joint military exercises with South Korea on Saturday and the US ambassador to the UN has said “the time for talk is over…China must decide whether it is finally willing to take this vital step (to resolve this situation)..” The Krw/USD was up 0.8% last Friday and is little changed this morning.

Elsewhere, one thing appearing to head in a better direction for Mr Trump is tax reform. The Republicans are now more confident of overhauling the US tax code, with an outcome likely by the end of the year. This follows House speaker Ryan making a concession and ditching his controversial border adjusted tax last week, which was expected to raise $1trn of tax revenue over a decade. Obviously there is still a long way to go though.

Taking a look now at some of the other data out on Friday, in Europe we got advanced reading of France Q2 GDP which increased marginally more than expected to +1.8% YoY (vs. +1.6% expected; 1.1% previous). We also got the preliminary July CPI readings for France which came in line with expectations at +0.8% YoY (-0.4% mom), while German inflation was higher than expected at 1.5% YoY (as discussed above) which was the main story of interest. We also saw a group of Eurozone confidence indicators for July where economic confidence (111.2 vs. 110.8 expected), services confidence (14.1 vs. 13.4 expected) and industrial confidence (4.5 vs. 4.4 expected) beat estimates although the business climate did disappoint (1.05 vs. 1.14 expected). The final reading for the July consumer confidence indicator also saw no revisions from the initial reading of -1.7 (as expected).

Taking a look now at this week’s economic calendar. Today, we have German retail sales (+0.2% mom expected; +0.5% previous) and UK consumer credit data for June due, followed by the Eurozone unemployment rate (9.2% expected) for June and CPI estimate (+1.3% YoY expected) for July. In the US we will get the Chicago PMI number (60 expected; 65.7 previous), the Dallas Fed manufacturing activity reading (13 expected; 15 previous) for July and June pending home sales (1% expected). We kick off tomorrow in Asia where we will get the Caixin China manufacturing PMI reading and the final Nikkei Japan manufacturing PMI reading for July. In Europe we will get July data for the UK Nationwide House Price index, followed by a first look at the remaining manufacturing PMIs out of Europe and the final July manufacturing PMIs for France, Germany and the Eurozone as a whole. We will also get the advance estimate for Q2 Eurozone GDP. In the US we will get personal income and spending numbers for June and the ISM manufacturing PMI for July. Wednesday is a quiet day in both the Europe and the US with no real data of note outside of ADP and the Eurozone PPI. Thursday’s calendar will round out July PMI data for the week. In Asia we will get the July composite and services PMI numbers for China (Caixin) and Japan (Nikkei). In Europe we get the July PMIs with the final services and composite PMIs for France, Germany and the Eurozone due as well as a first look at some of the same data for the rest of Europe. Thereafter all focus should shift to the BoE policy meeting. Over in the US we should also get jobless claims data followed by the ISM non- manufacturing composite for July. Thereafter we will get factory orders data as well as the final readings for durable and capital goods orders for June. Friday is relatively quiet day for data in both Asia and Europe with only German factory orders data for June due. The US should be in greater focus as the July payrolls number is due along with other labour market data. Alongside that we will also get the trade balance reading for June.

Onto other events, on Tuesday, trade ministers from the BRICS countries will meet in Shanghai. Then Wednesday, the Fed’s Mester will speak at a Community banking conference and the Fed’s Williams will speak in Las Vega’s on monetary

Full story here Are you the author?Tags: Apple,Asia Pacific,Australia,Bank of England,Bank of Japan,Bond,BRICs,Business,caixin,Canadian Dollar,China,Consumer Confidence,Consumer Credit,Consumer Sentiment,Copper,CPI,Crude,Currency,Dow 30,economy,Economy of the European Union,Equity Markets,Euro,European central bank,Eurozone,federal government,Federal Reserve,Finance,France,Germany,Gilts,Global Economy,headlines,Hong Kong,Insurance Companies,Japan,Japanese yen,Jim Reid,Michigan,NASDAQ,newslettersent,Nikkei,Nikkei 225,North Korea,Obamacare,Personal Income,Precious Metals,Price Action,recovery,renminbi,Reserve Bank of Australia,S&P 500,Sovereigns,Swiss Franc,tax revenue,Trade Balance,Trump Administration,Twitter,U.S. Dollar Index,Unemployment,University Of Michigan,US Dollar Index,US Federal Reserve,Volatility,Yen