Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Spain’s Banco Popular is scrambling ahead of its meeting with the ECB tomorrow; shares are around 50% in three sessions.

Italy has two banks that may see the same deal Monte Paschi negotiated with the EU.

Portugal banks are still putting loan loss reserves and provisions aside.

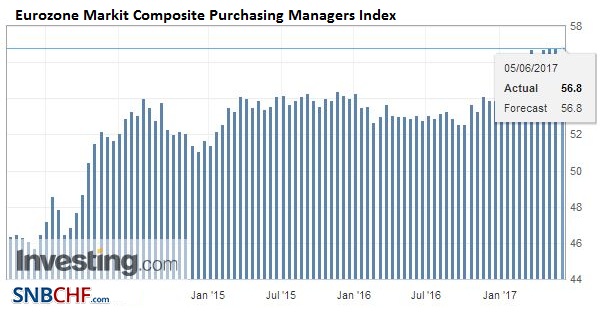

EurozoneThe eurozone appears to be in rare form. The political threat that seemed so palpable at the start of the year has faded. Not only have the populist-nationalists been turned back at every opportunity, but polls suggest the new French President can secure a parliamentary majority in upcoming elections. The regional economy continues to expand at a stable clip around 0.4% a quarter, which may be a little above trend. The composite PMI reported earlier today unchanged at 56.8 in May is above the 55.6 average of Q1 17, the 53.9 average in Q4 16 and the 53.3 average for all of last year. The ECB meets later this week. It is widely expected to take a small step toward the eventual end of its extraordinary monetary policy shepherded by Draghi, who was once referred to as the Prussian Roman. Most likely, the step will involve some moderation of its forward guidance. In September, it is expected to announce its intentions to scale back its purchases from the current pace of 60 bln a month and extended them into the first part of next year. |

Eurozone Markit Composite Purchasing Managers Index (PMI), May 2017(see more posts on Eurozone Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

| The ECB is challenged, as are many major central banks, with softer than desired inflation. The drop in the price of oil, the strengthening of the euro, and unwind of the effect of Easter and poor weather are conspiring to push headline and core inflation lower after a recent spike. This alone keeps the majority of the ECB reluctant change policy. Recall in 2008 and 2011 the ECB tightened monetary policy prematurely. The ECB cannot afford to make the same mistake in 2017.

The eurozone faces two imminent challenges. First, Greece’s debt situation is unresolved insofar as the European proposal to extend some maturities does not satisfy the IMF, which has argued for greater debt relief. Without a significant move, European officials risk delaying when Greece can fund itself in the capital markets. In turn, this is raising the prospect that Greece will need another aid package when the current one expires in the middle of next year. It seems impolitic to discuss this ahead of the German election in September. European finance ministers meet next week. Greece will most likely be granted a tranche payment so that it can service the debt largely held by the official creditors. The second imminent problem, like Greece, is also the return of an old issue that has not been addressed: namely European banks. Spain’s Banco Popular is in the cross-hairs. Share prices fell by around a third in the second half of last week and were off another 16% today. Its debt is also selling off. This seems to be contributing to the rally in the sovereign CDS. It was trading near 63 bp a month ago. It is now near 78 bp. |

Eurozone Services Purchasing Managers Index (PMI), May 2017(see more posts on Eurozone Services PMI, ) Source: Investing.com - Click to enlarge |

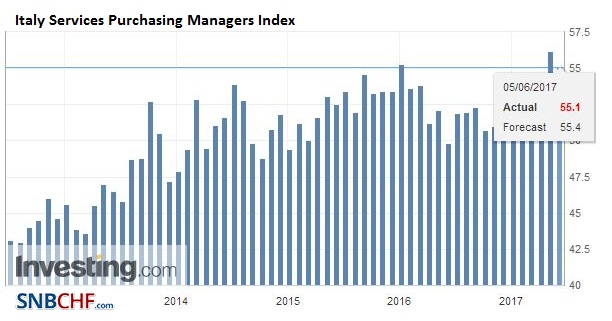

ItalyAn index of Italian bank shares eased by around 6.3% in January and February before rebounded 18% in March and April. It was off 1.1% last month when it finished with a five-day slide. It was up 0.65% last Thursday and Friday and is off 1.6% today. March and April were also good months for the bank index within the Dow Jones Stoxx 600 when it rose 15%. It fell 2.2% last month. Like Italy, the European bank index is giving back today everything it made in the second half of last week plus some. |

Italy Services Purchasing Managers Index (PMI), May 2017(see more posts on Italy Services PMI, ) Source: Investing.com - Click to enlarge |

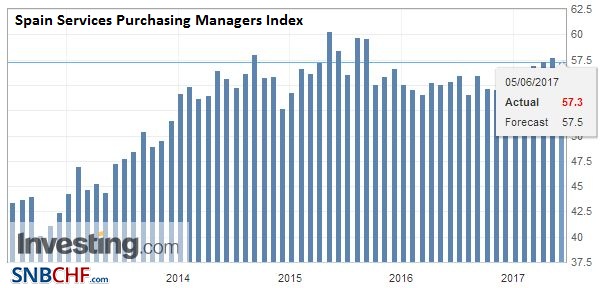

SpainIn addition to Spanish and Italian banks, there is also concern about Portuguese banks. The largest banks are still putting funds aside to cover bank loans. Portugal’s largest publicly traded bank put a record 1.6 bln euros aside last year for impairments. Caixa Geral, which is already owned by the state, put three bln euros aside for impairments and provisions in 2016. |

Spain Services Purchasing Managers Index (PMI), May 2017(see more posts on Spain Services PMI, ) Source: Investing.com - Click to enlarge |

Bad real estate loans are the main culprit. It is trying to sell assets. Reports suggest it has raised a little more than 200 mln euros in recent weeks by selling stakes in Targobank (jointly held with a French bank) and a real estate company. It has sold treasury shares and Tier 1 notes issued by itself and other lenders. It is also reportedly in talks to sell its US unit TotalBank.

Bank officials are to meet ECB officials tomorrow. Its choices are getting to be stark. Unload more assets quickly, find a buyer for the bank, or move into resolution.

Meanwhile, Italian banks are also in the spotlight. Monte Dei Paschi recently reached an agreement with the EU that involves a precautionary recapitalization. It is unclear whether this can serve as a model for two other Italian banks (Banca Popolare di Vicenza and Veneto Banca. A key issue is the extent to which the banks’ shareholders and junior bondholders share in the burden of adjustment (i.e., haircut).

On a purely directional basis, the euro’s correlation with the Dow Jones Stoxx 600 bank index reached a three-year high near 0.90 in the middle of last month on a 60-day rolling basis. The correlation has eased a bit, but at 0.66 it is still fairly strong about the last several years. Still, the decoupling is evident, as the bank share index peaked on May 5 and the euro made new highs for the year before the weekend.

The banking challenges in these three periphery countries do not pose the systemic risk that they may have a couple of years ago. The euro is benefiting from the lifting of political uncertainty in Europe and increasing questions about US politics. At the same time, more skepticism about the health of the US economy and the ability of President Trump to enact his economic agenda also help underpin the euro through the interest rate and portfolio flow channels.

Full story here Are you the author?Tags: #USD,$EUR,Eurozone Markit Composite PMI,Greece,Italy,Italy Services PMI,newslettersent,Portugal,Spain,Spain Services PMI