Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Light economic data calendar, but look for downtick in eurozone flash PMI.

Soft Canadian retail sales (volume) and softer CPI (base effect) could take some of the sting from the recent BoC official comments.

MSCI decision on China, Argentina, Saudi Arabia, and South Korea may have the broadest and long-lasting impact of the five key events we highlight.

It is a light week for economic data from the G7, and for the reports that are on tap are unlikely to change the consensus scenario in the aftermath of major central bank meetings in the first half of the month. Canada may be the chief exception to this generalization. In the second half of the week, Canada will report retail sales and CPI.

The reports will show less consumption and price pressures. It may ease concerns, prompted by Bank of Canada officials that the degree of accommodation is worth reconsidering. Consumption jumped in Q1 (2.4 percentage points to 3.7% GDP, the most since the crisis, and appears to eased here in Q2. Retail sales rose 0.7% in March. We know fall in auto sales in April will be partially blunted by the rise in gasoline prices. The risk seems to be on the downside in volume terms.

The Bank of Canada recently suggested that the soft core inflation readings were the result of the lagged effect of excess capacity. This implies that it expected higher inflation readings in light of the strong growth over the past few quarters. However, the pass-through from stronger growth to higher prices may take longer than the market may suspect, which has increased the odds of a July rate hike to from about 5% at the end of May to 45% at the end of last week. The base effect and the electricity rebate (Ontario) warn of downside risks.

The Reserve Bank of New Zealand and the Norway’s Norges Bank hold policy-making meetings. Neither is expected to change. Although Q1 GDP disappointed, more recent data from New Zealand suggest the economy is rebounding. We suspect the next move will be a change in the forward guidance either now or the middle of Q3. The recent regional survey by Norges Bank suggests the economy may be re-accelerating. The central bank seems content with the economic progress and does not appear to be in a hurry to change the monetary setting.

Argentina has seen foreign inflows into its equity market amid speculation MSCI will include Argentina shares again in its Emerging Market equity index. Some of the same firms that appear to be lobbying for it may have also been buying the shares. Saudi Arabia has implemented several reforms to that would make its including into the MSCI Emerging Market equity index more likely, including introducing short sales and T+2 settlement. Foreign investors have less than 5% stake in the Saudi equity market, and there is not a strong lobbying effort to include them. The issue with South Korea is whether MSCI upgrades it to a developed market rather than an emerging market. The increased weight of China in the emerging market index means a smaller weight for South Korea. Being including the development market index would make it accessible to a different category of investors, with a larger pool of capital.

MSCI decision: On June 20, MSCI announces it annual updates. Investors are focusing on four countries: China, Saudi Arabia, Argentina, and South Korea. In the fourth attempt to include China’s A-shares, MSCI ha proposed a scaled-down version of last year’s proposal. It could include 169 Chinese companies’ shares down from 448 previously. The issues are accessible through the stock-connect link between Hong Kong and Shanghai and Shenzhen. Large cap companies only are included. The odds seem to have increased, but it remains a close call. Two issues may not have been adequately addressed. They involve the suspension of shares and market data. Chinese shares (that trade in HK, and in ADRs) account for about 25% of the MSCI emerging market equity index. The proposed A-share inclusion would account for about 0.5% in the index; a modest step. Over time, the China’s shares may eventually account for 40% of the MSCI emerging market equity index.

Italian Banks: A last minute attempt to get large Italian banks to provide over a billion euros for two troubled regional banks failed. A precautionary recapitalization by the government cannot take place. One of the banks (Veneto Banca) debt payment due this coming week was postponed by the EC. The banks appear to be headed for one of the three outcomes of the Bank Recovery and Resolution Directive (BRRD): liquidation, wind-down, resolution. The BRRD offers several tools for the resolution, among which is a bad bank-good bank arrangement. Initial press reports suggest Italian officials, who had been suggesting an optimistic outcome much of last week, seem to refer this latter course as the next best.

JapanIn terms of economic data, two reports stand out that may be market sensitive: Japan’s trade balance and the flash PMI for the eurozone. Over the last 20 years, Japan’s May trade surplus has improved over April one (2009). This week’s report is expected to be true to trend. The median guesstimate from the Bloomberg survey is for a trade surplus of JPY43.3 bln down from JPY481 bln in April. A recovery is likely in June. However, the balance is less important than the performance of exports and imports. The former is expected to accelerate and the latter to slow. Even though slowing of imports is often associated with economic weakness, in Japan’s case, the rise exports are positive for growth, as it underpins industrial output and capex. |

Economic Events: Japan, Week June 19 - Click to enlarge |

EurozoneThe eurozone’s solid and steady growth spurred talk that the ECB is too easy. Ironically, US growth was slightly lower than the eurozone’s last year, but US unemployment (speaks to the output gap) is considerably lower and inflation considerably higher, and yet many observers, including former Treasury Secretary Summers, have been critical of the Fed for being too hawkish. We have been concerned that all the good news from Europe has now been discounted. Unhedged European stocks, alongside emerging markets, were among the favored strategies in the first half. Macron’s victory over Le Pen and the likely victory for Merkel in September is widely recognized. The fear of a populist-nationalist wave sweeping across Europe seemed to rise a bit after Brexit but accelerated with Trump’s victory in the US. It was a distraction from the underlying structural issues in Europe. These have not been addressed. ECB President Draghi continues to plea for countries to implement structural reforms. The European Union itself has structural issues and institutional challenges, with or without the Britain. We suspect Europe is near a peak. The Dutch don’t have a government. The Finnish government nearly collapsed last week. Catalonia is planning a referendum in early Q4 which puts it at loggerheads with Madrid. In France, Macron is not the first French president to be elected on a reformist agenda and promise labor reforms. Sarkozy and Hollande promised reforms. A Merkel victory in Germany means that, whether in partnership with the FDP or the SPD, the basic thrust of German policy will not change. The chances of an early Italian election have faded, and the Five-Star Movement has done poorly in the local elections. However, it is not clear how closely a national election will track the local results. There were some idiosyncratic problems. There is still no agreement on the electoral law. The economy too cannot do much better. Some confidence has shown the assessment of current conditions remains elevated, but expectations have begun slipping. The flash eurozone PMI is expected to slip. It is expected to be small for both manufacturing (from Germany) and services (France), which will result in a lower composite reading. The magnitude is not significant; the direction could be a forewarning of a new economic phase. |

Economic Events: Eurozone, Week June 19 - Click to enlarge |

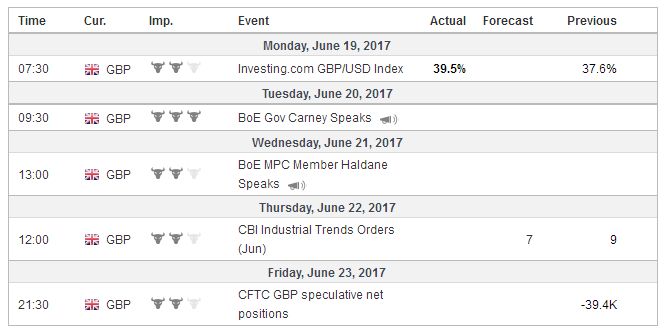

United KingdomBrexit negotiations The negotiations begin on Monday and come at an awkward time for UK politics. It is not clear that a majority favor leaving the EU anymore. In last June’s non-binding referendum, the decision to leave was carried by the smallest of majorities (52%-48%). Polls (Survation and YouGov) suggest that a growing majority do not want to leave the customs union, and an increasing number want to priorities unrestricted trade over immigration controls. Nevertheless, the Chancellor of the Exchequer Hammond, rumored to be ousted if Prime Minister May won a resounding victory, as the early pre-election polls pointed to, reaffirmed over the weekend that the UK would indeed leave the single market and customs union. This dashes the hopes that the election would spur a reconsideration of the government’s strategy instead of a doubling down. Queen’s Speech June Mansion House Speech: The Queen’s Speech is delivered by the UK Prime Minister on June 21, and outlines the legislative agenda for the parliamentary session. In an unusual move, it was pre-announced that there will not be a Queen’s Speech in 2018. Instead, the parliamentary session will run two years. The announcement was seen as another indications that May does not intend to change the main approach to Brexit. Of note, after a couple of days of negotiations with the Democrat Unionist Party (DUP), no formal agreement has been reached. May decision to push ahead with the Queen’s Speech without the agreement illustrates her commitment to lead the UK even with a minority government. Carney and Hammond will deliver their delayed (due to the Grenfell fire) Mansion House speeches a day earlier. Recall that last week, the BOE’s decision to stand was decided by a 5-3 vote. Carney can be expected to present the case of looking through the increase in price pressures as primarily a transitory phenomenon related to the past decline in sterling. It will be gradually passing in the second half of the year. Meanwhile, the slowing of the labor market, weaker earnings growth, and less consumption pose greater near-term risks. |

Economic Events: United Kingdom, Week June 19 - Click to enlarge |

United StatesSpecial election in Georgia’s 6th Congressional District: On June 20, there is a special election in Georgia to fill the seat of Price who after winning the election in November was appointed to the Secretary of Health and Human Services. That seat was previously held by Newt Gingrich. Price won the election easily with a 23 percentage point margin. Trump carried the congressional district by less than two percentage points. This election is being watched closely as a bellwether. If the Democrats (Ossoff) can take the seat, it will be seen as a sign of a backlash against Trump, whose support in most opinion polls is below what it was in November. It will embolden the Democrats for next year’s mid-term elections and be obstructionist in the meantime. If the Republicans ( Handle) hold on to the seat, it will be seen as a sign that the Democrats are overreaching. It will encourage Republican Representatives not to abandon the President and his agenda. That, in turn, may slow the unwind of what has been dubbed the Trump trade. |

Economic Events: United States, Week June 19 - Click to enlarge |

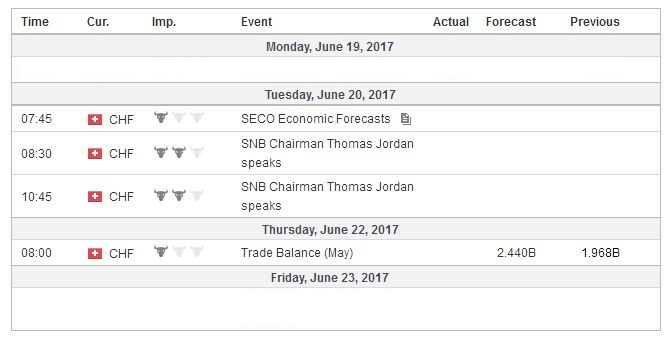

Switzerland |

Economic Events: Switzerland, Week June 19 - Click to enlarge |

Full story here Are you the author?

Tags: #GBP,#USD,$CAD,$EUR,$JPY,newslettersent,Norwegian Krone,NZD