Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

![]() Introduction by

Introduction by

George Dorgan

My articles

My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

US retail sales and CPI should help bolster confidence that the Fed was right about the transitory nature of Q1 slowdown.

Bank of England meets; Forbes will likely continue with her dissent, but likely failed to convince her other colleagues of the merit of an immediate rate hike.

French politics are center stage, but German state election and South Korea’s national election are also important.

Sometimes there seems to be a single factor of overwhelming influence in the capital market. We have maintained that to the extent one exists, it was divergence as the Federal Reserve is well ahead of the other major central banks in the beginning to normalize policy.

The rise in US interest rates and the related increase in dollar’s exchange value was an integral part how the global recovery was to strengthen. The below PPP exchange rates in Europe and Japan and the continued pursuit of aggressive, unorthodox monetary policy should help pave the way for stronger recoveries.

And indeed that seems to be the case. The eurozone expanded slightly faster than the US last year, and in Q1 17, it grew nearly as much as the US did an annualized pace (0.5% quarter-over-year vs. 0.7% annualized). The Japanese economy is also finding better traction. In addition to valuation considerations, another factor drawing money to European equities this year is that it being behind the US also meant the potential for p/e expansions. Emerging markets also drew investment, after recent drawdowns, as two threats eased. US bond yields had trended lower, and the Chinese economy appeared to stabilize.

Some observers may be exaggerating the importance of a change in the ECB’s forward guidance. The ECB has famously kept an easing bias by suggesting that rates could be cut further. However, while true in theory, after all the zero thresholds has been breached, but no one believes it is within the realm of possibilities barring a paradigm shifting shock.

In effect, the ECB may drop a phrase of little real value to investors in the first place. The most likely scenario is still that the Fed hikes and begins to reduce its balance sheet before the ECB stops expanding its balance sheet or brings the deposit rate back to zero from minus 40 bp. The BOJ’s balance sheet is expanding a bit slower than JPY80 trillion a year, but what is a few trillion yen at this juncture than a rounding error?

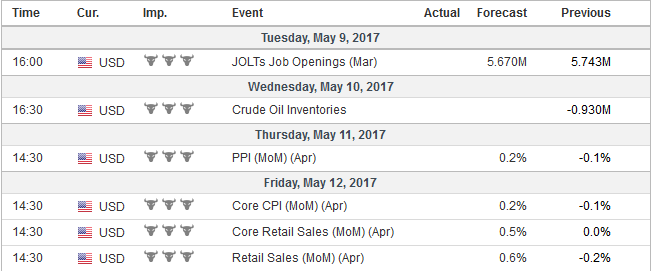

United StatesWhile the Fed funds futures strip implies a strong chance of a Fed hike in June (Bloomberg says almost 99% chance, the CME says 78.5%) to 1.00%-1.25%, the US two-year note is yielding 1.31%. In January and February, when many expected the next hike to be in June, the two-year hovered around 1.20%. The yield rose to 1.40% in response to the Fed’s full course press to prepare investors for a March move. At 2.35%, the US 10-year yield is below where it was the Fed hiked at the end of 2016 and again a couple of months ago. After the poor Q1 GDP, the onus is on the US economy to demonstrate that the headwinds were transitory. That is what we expect to be delivered in the main two economic reports next week: retail sales and CPI. Consumption was particularly weak in Q1. The foundation for better consumption that is income and that means wages/salaries and transfer payments, remain intact. If consumption is going to increase, then the first place to look is retail sales. A 0.5%-0.6% is expected after a 0.2% decline in March. In part, this will reflect the increase in gasoline prices. The components that are used in GDP calculations are expected to be rise by 0.4%. That said, the average core retail sales rose an average of 0.23% in Q16, while they averaged 0.27% in Q1 17. Personal consumption expenditures rose 3.5% an annualized rate in Q4 16 but only a miserly 0.3% in Q1 17. Consumer prices appeared to have increased in April after softening in March. The headline may increase 0.2% after a 0.3% fall in March. The year-over-year rate could edge lower to 2.3% from 2.4%. The core rate is expected to increase 0.2% after easing 0.1%. This would keep the year-over-year rate steady at 2.0%. The markets did not react much to the passage of health care reform by the House of Representatives. It was to free up funds that could ostensibly be used to fund tax reform. The S&P 500 edged to new record highs before the weekend, but this seems to be part of a global move and not a US-specific driver. In fact, the only G7 market to do worse than the S&P 500 0.6% gain was Canada’s where the TSX was off 0.3%, after a 1.2% rally before the weekend. Trade tensions with the US, the decline in oil prices, and diverging interest rate differentials undermined the Canadian dollar. It is the worst performing major currency so far this year, off 1.6% against the US dollar. The two-year US premium jumped from 45 bp on April 20 to 63 bp at the end of last week. This is the widest premium in a decade. However, the positioning and price action in the Canadian dollar is warning the bears to be careful.The gross short Canadian dollar futures at the CME appear to be at a record high as of May 2. The price action before the weekend, whereby the US dollar made new highs and then sold off closing below the previous session’s low is a negative technical sign. Not coincidentally, oil prices snapped back to close 1.5% higher after initially plunging 4% to levels not seen since April 2016. Copper prices stabilized after briefly trading to new lows for the year. Iron ore future prices in China fell more than 5% before the weekend to end the sixth weekly decline in the past seven. Steel futures have also fallen. |

Economic Events: United States, Week May 08 - Click to enlarge |

ChinaChina’s capital controls appear to have effectively slowed capital outflows, while under-performance of the equity market and bearish sentiment toward the yuan has discouraged capital inflows. Reserves rose ($20.45 bln to $3.03 trillion) for a third consecutive month in April as capital controls bit and the dollar’s decline flattered the valuation of other currencies in reserves. Even if capital flows have slowed, trade linkages remain significant. Its supply and demand for industrial metal may not be the only consideration, but it is a major driver most of the time. It is expected to report a moderation of both imports and exports (in dollar terms). Slower growth in imports and exports is not inconsistent with a larger trade surplus. It is expected to rise to around $35 bln from $24 bln. There is also a large seasonal component. China’s trade surplus has widened in April over March for the last seven years and in nine of the past 10. Tame consumer prices will create scope for stimulus if economic slowing becomes too pronounced, and in the meantime, officials can focus on curbing some of the excesses, including lending and leverage. |

Economic Events: China, Week May 08 - Click to enlarge |

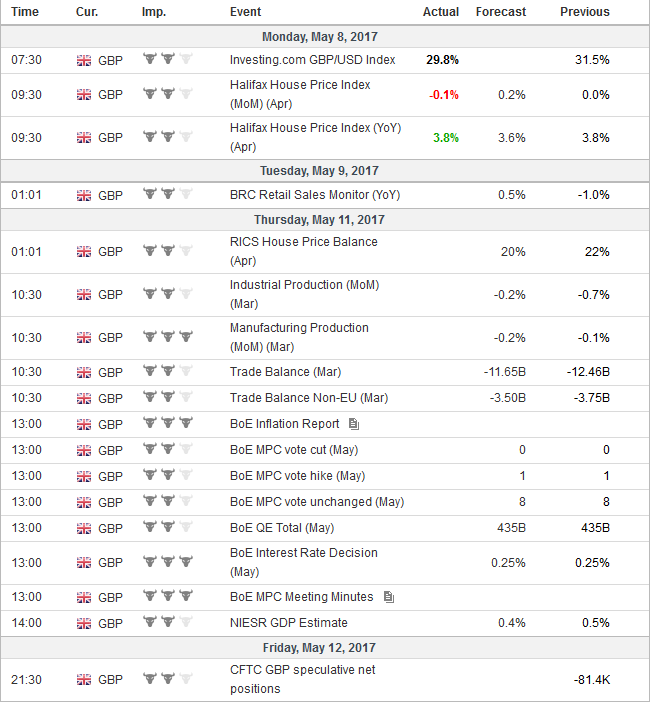

United KingdomThe Bank of England meets and issues its quarterly inflation report. Just like the FOMC looked past the soft Q1 GDP, the MPC seems inclined to look through firm real sector and price data. Each of the three April PMIs released last week were better than expected. Prices pressures do not appear to have peaked. However, it still arguably reasonable to expect the economy to slow and the base effect, points to a peak in CPI, perhaps by the end of Q3. Since the last quarterly inflation report, growth has been a bit slower than expected, and inflation, a bit firmer. Forbes disagrees. She dissented last month for an immediate hike and is likely to dissent again. However, her term ends shortly, and she probably was unable to convince any of her colleagues to join her. That said, if perchance there is more than one dissent, it could catch the market leaning the wrong way. Consider that implied yield of the December short sterling futures contract finished last week at 42 bp. In the middle of last December, before year-end pressures emerged, the yield was near 55 bp. We note that in the future market, speculators have retained a large short gross sterling position (135k contracts, 62.5k GBP per contract), the largest among the currency futures. |

Economic Events: United Kingdom, Week May 08 - Click to enlarge |

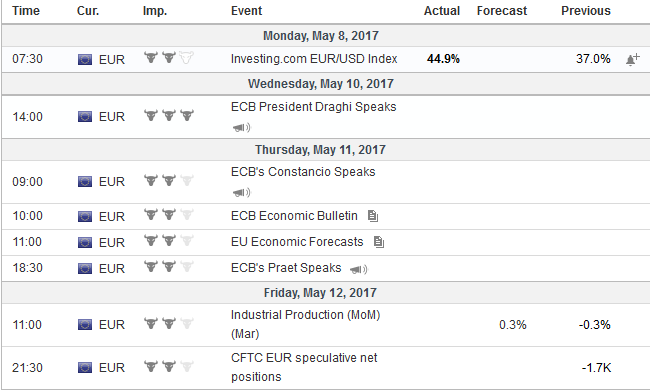

EurozoneIndustrial production figures are featured from Europe, but the data does not matter. Investors focus is not on Q1 data as we approach the midpoint of Q2. Also, the challenge for the ECB is not current growth, but prices. The combination of euro’s gains (three of four months this year) and weaker commodity prices are not usually associated with an acceleration of inflation. It seems a foregone conclusion that Macron is going to be the next president of France. Th euro may rally on the announcement, but the significance cannot be known with any degree of confidence until next month’s parliamentary election. Macron comes from the pro-business wing of the French Socialist Party. The Socialist Party is, in essence, a social democrat party, with the propensity to create factions and new parties. Macron’s departure to launch his own party removed a key obstacle to the fundos-wing take control of the Socialist brand that had been driven into disrepute by the unpopular Hollande. French national interests do not change from election to election. It is a debtor nation often expresses the interests of debt countries. It is a check on Germany and the interest of the creditors. Macron, like Merkel, Renzi (and Gentiloni), and Rajoy that are pro-Europe but attach somewhat different meaning to Europe. France will follow Finland, Austria, and the Netherlands in turning back a populist-nationalist challenge. In recent council elections in the UK, the populist-nationalist UKIP was nearly wiped out. Its single issue agenda has been co-opted by the Tories. It is still not clear how Trump will govern. He plays to the populist-nationalists, even when he does not have to, such as endorsing Le Pen, yet, in many ways, he is governing like what the FT’s Martin Wolf dubbed a post-Reagan Republican Overshadowed by the French election, the small German state of Schleswig-Holstein goes to the polls. It is led by as SPD coalition. The CDU may get the most votes, but a combination of SPD, Greens and the FDP could form a coalition if the small Danish-speaking party fails to secure representation in the state parliament might not be counted on to sustain the current coalition. The new SPD leader Schulz had a brief honeymoon that bolster the party’s standing in the polls, but it has faded and next week, his home state, North Rhine Westphalia the most populous German state holds local election. It is currently led by a minority SPD-Green coalition. |

Economic Events: Eurozone, Week May 08 - Click to enlarge |

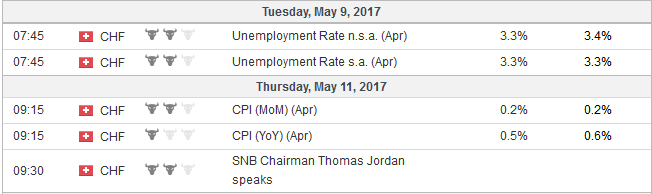

Switzerland |

Economic Events: Switzerland, Week May 08 - Click to enlarge |

The Reserve Bank of New Zealand meets next week and policy is on hold. There is no urgency. Australia’s fiscal policy eclipses monetary policy. Infrastructure spending (rails, roads, and a new airport). Over the past month, the Australian dollar has been the weakest of the majors losing about 2% against the US dollar. It staged a sharp recovery before the weekend, not as technically robust as the Canadian dollar, but promising.

There has been a perverse counter-intuitive reaction to Brexit and Trump’s unexpected electoral success in the US. In Europe, pro-EU sentiment has grown since the slim majority voted for the UK to leave in nearly every country, except Italy. In the US, traditional media has found new subscribers and Democrats are talking about the benefits of trade agreements.

The populist-nationalist rhetoric in Washington is spurring populism-nationalism in Mexico. Trump’s bellicose rhetoric and his reference to Korea once being part of China may have helped bolster the candidacy of Moon Jae-in as the next president of South Korea. More than the other candidate, he is more likely to delay the establishment of the US anti-missile capacity, which has antagonized China and would be a possible basis for a rapprochement with North Korea.

Full story here Are you the author?

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,newslettersent,SPY