Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Many observers misunderstood US President Trump’s “American First” rhetoric. Trump’s earlier writings show that this is not a reference to the 1940s effort to keep the US out of WWII, with its isolationist tint.

Rather, Trump’s use goes back to the original use by President Harding in the 1920s. It was a rejection of the Wilsonian multilateralism (e.g. League of Nations) and a robust defense of unilateralism. That unilateralism was clearly on display in the missile strike on Syria.

Yet the fear of US disengagement was so acute, that many US allies welcomed the unilateralism. It may be less undesirable than isolationism, but unilateralism risks weakening the international rule of law, and sets dangerous precedents, as Putin demonstrates.

Many investors and foreign policymakers are trying to tease out underlying principles of the Trump Administration. What is the underlying narrative? If there is one, it appears to be a crude realist view that the international arena is where states compete in the pursuit of national self-interest, at the heart of which is a short-run commercial success.

It is not so much that Trump was duplicitous in refusing to cite China as a currency manipulator or in the missile strike on Syria, for which, after pushing the birth certificate claims, was among his most repeated criticism of Obama. Instead, US national interests are contingent, and as his perceptions of them change, Trump’s positions change. NATO was obsolete a few weeks ago. Now it isn’t. Russia’s support for Syria has not changed. Trump’s perceptions of it did. China’s behavior in the foreign exchange markets has not changed in the past 12-18 months, but Trump’s view of it changed as North Korea become more intransigent. Trump explicitly linked the possibility of China’s efforts on North Korea with the decision not to cite it as a currency manipulator, which unnecessarily further politcizes the integrity of the exercise.

Neither the missile strike on Syria nor the dropping of the largest non-nuclear bomb on Afghanistan appears to have changed the essential conditions on the ground. Nor are they perceived to be the start of an escalated military campaign. Geopolitical tensions may ease in the coming days if this assessment is borne out. If one believes that both conflicts will require a political solution, the US attacks may be more important for their signaling rather than the punishment delivered.

The anniversary of the birthday of the founder of North Korea passed without much incident, though early Sunday, a ballistic missile launch apparently failed after a few seconds. China reportedly is putting more pressure on its ally to give up its nuclear capability. A preemptive strike by the US does not seem particularly likely, but if North Korea were to conduct another nuclear test, some military response by Trump cannot be ruled out.

In the geopolitical dance of early 21st century between the US, Russia, and China, each wants to have a partner. Under the last few years of Obama, Russia and China seemed to be the couple, and the US the odd-man out. Trump seemed to want to cut in and dance with Russia. As we noted, Syria changed this, and some suspect the investigations of the Trump campaign to Russia, may have encouraged the quick abandonment of the initial strategy.

The US and China seemed to be better paired, though Tinder may not think so. Under the US leadership, NATO rolled east since the end of the Cold War. China’s One Belt One Road initiative integrates the soft underbelly of the former Soviet Union into its sphere. From a strictly commercial standpoint, China is significantly more important than Russia. A dance with Russia steps on Europe’s toes, where Russian forces continue to harass nations on its borders.

A relaxation of tensions, which may be nothing more than not repeating or escalating recent developments could help the capital markets stabilize. However, another source of political risk may intensify in the days ahead. The first round of the French presidential election is April 23. Anxiety has been running high as the recent polls suggest that any two of the top four candidates could move into the second round, given the margin of error.

The recent movement was the rise of Melenchon, a candidate from the left-wing of the Socialist Party. Given the two-round nature of the French elections, voters can express their principles in the first round and become more pragmatic in the second. Polls suggest Melenchon would beat Le Pen in the second round, but would also be destabilizing. Even after the presidential election, political risk is unlikely to be alleviated. Parliament elections will be held in June. Only Fillon has a bloc in parliament. Macron and Melenchon would likely reach out to the Socialist, from where they come. Le Pen’s National Front also does not have parliamentary representation.

Outside of politics capital flows may be changing. In the week that ended April 7, Japanese investors sold nearly JPY2.18 trillion of foreign bonds. This is the most in a year. In that one week, Japanese investors sold almost as much as they sold in the first three months of the year (~JPY2.65 trillion). Consider that in the first 14 weeks of 2017, Japanese investors sold an average of JPY344 bln of foreign bonds a week. In the 14 weeks before the US election, they bought an average of JPY327 bln a week. The end of the fiscal year may be behind latest repatriation. We will be watching the weekly MOF data to see if the strong yen (though low international yields, including Treasuries, induce new buying).

The US 10-year premium fell to 220 bp last week, the lowest in four months. It was near 175 bp a year ago and fell below 160 bp last August and September before rallying to 254 bp a couple of days before the Fed hiked rates last month. We suspect the US premium has bottomed or nearly so, which may help underpin the dollar against the yen.

Chinese capital flows have also changed. Capital controls, perhaps the decline in US rates, which has eased some pressure on the yuan may be stemming the capital outflows. Reserves edged higher in February and March. It seems more a case of stabilization than a return of funds to China. China’s economy appears to have stabilized too, and Q1 17 GDP is expected to be little changed from the 6.8% pace reported in Q4 16 and the average pace since the middle of 2015.

In terms of US politics, there are two things to watch. First, there is much speculator that special presidential strategist Bannon may leave the Trump Administration amid a mini-shuffle seen likely around the 100-day in office threshold, which is late this month. It would be seen as part of the shift in the Administration away from Russia, and part of the ascendancy of the other more liberal globalist wing, represented by people like Cohen and Mnuchin.

Second, there is an election for Price’s seat in Georgia, who is the new Secretary of Housing and Human Services. Although Price won his seat handily, Trump barely beat Clinton in the congressional district. It is an open primary pitting several Republicans against each other and the Democrat Ossoff. If no one gets 50% of the vote, like in France, there will be a run-off (June 20). It is seen as an early referendum on Trump’s presidency.

The Treasury Department’s semiannual report on the foreign exchange market was released on Good Friday. Trump had already stolen the thunder by revealing in the WSJ interview that China would not be cited. The report reads like the previous report under Treasury Secretary Lew, and the six countries that posed a challenge then were cited again: China, Japan, South Korea, Taiwan, Germany, and Switzerland.

Note that Japan and China have both agreed to conduct trade talks with the US, which would have been one of the consequences of being cited as a manipulator. Japan’s Prime Minister Abe will meet US Commerce Secretary Ross on April 18. Ross is reportedly working on a comprehensive review of US trade, with attention to currency misalignments (different thrust than manipulation, though perhaps still susceptible to pressure for remedial action).

At the time of this writing the outcome of the referendum in Turkey is not known. The referendum seeks to concentrate more power in Erdogan. Polls suggest it may be a close vote. If the referendum is successful, Erdogan would have few constitutional checks on his authority. The impact will be largely localized, but it will further strain its relationship with the rest of Europe.

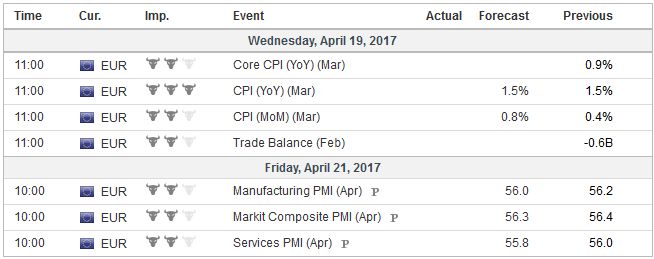

EurozoneEconomic data over the course of the week ahead is not particularly significant and are unlikely to alter base case views of the different economies. Survey data has been running ahead of actual performance in the US and Europe. That means that some softening in the April Empire State and Philly Fed surveys are likely to have little impact. That same generalization may also apply to the flash eurozone PMI at the end of the week. No one expects the Fed to hike rates in May, and this makes the Beige Book somewhat less interesting. |

Economic Events: Eurozone, Week April 17 - Click to enlarge |

United StatesUS utility and extractive sector (oil) may have helped lift industrial output, but the manufacturing component looks set to soften, with some negative impulses possibly coming from the auto sector.One of the factors discouraging new capital expenditures and weighing productivity is that US industry is only using a little more than three-quarters of its capacity. Our technical work warns that the rally in gold, oil, yen and US Treasuries are getting stretched. We want to be particularly attentive to price action reversals that would turn the technical indicators lower. Major equity markets look vulnerable. The S&P 500 ended last week with a three-day slide and the lowest close in two months. The Nikkei closed last week at four-month lows. The Dow Jones Stoxx 600 recorded its best level last week since December 2015. European funds have reportedly seen strong inflows, and this leaves new longs in weak hands, in there is a deeper pullback, as the technical indicators seem to suggest. |

Economic Events: United States, Week April 17 - Click to enlarge |

United KingdomThe UK reports March retail sales at the end of the week. After the outsized rise in February (1.3% excluding petrol), a pullback is expected. The BRC already reported some dismal figures. Slower wage growth and higher inflation sap the purchasing power of UK households. |

Economic Events: United Kingdom, Week April 17 - Click to enlarge |

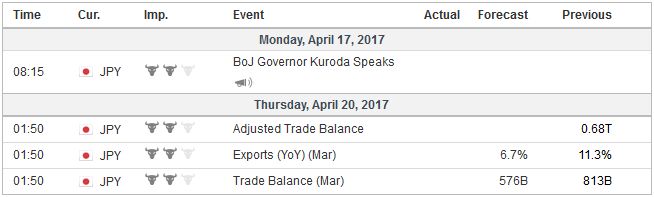

JapanThere are strong seasonal influences on Japan’s trade flows. The March trade balance often but not always improves over February, which always improves from January. The consensus expects some deterioration this time. Exports are expected to slow, while imports rise. The trade deficit in January-February was about a third smaller than the similar year ago period. |

Economic Events: Japan, Week April 17 - Click to enlarge |

Australia

Australia reports the minutes from the recent central bank meeting. A few days before the meeting, regulators tightened rules on mortgage lending. The housing market had been a concern of RBA officials. The central bank seems content to bide its time and update its forecasts next month. With the Bank of Canada on hold, the March CPI report is unlikely to have a lasting impact. The headline pace may is expected to slow, but the new common core is expected to be steady at 1.3%.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CNY,$EUR,$JPY,$TLT,newslettersent,SPY