Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

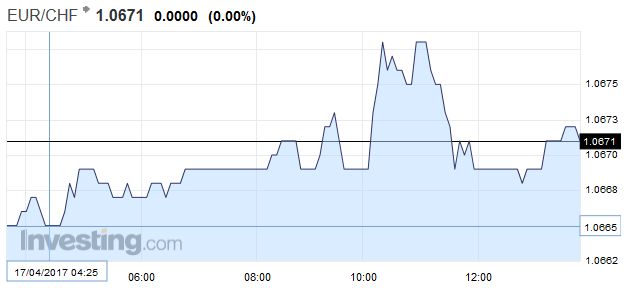

EUR/CHF - Euro Swiss Franc, April 17(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesFinancial centers in Europe are closed for the extended Easter holiday. Australian and New Zealand markets were also closed. The drop in US 10-year Treasury yields in early Asia, with a brief push below 2.20%, appears to have kept the dollar under pressure. As the North American market prepares to open, the dollar is softer against the all major currencies and many emerging market currencies. In fairness, the unexpectedly soft March CPI data and soft retail sales (incorporating the back-month revision) before the weekend, while the Treasury market was closed, would have weighed on yields regardless of the weekend events. That said, the strength in the March core retail sales (0.5%) suggest that after a poor start, household consumption likely began Q2 with reasonable momentum. |

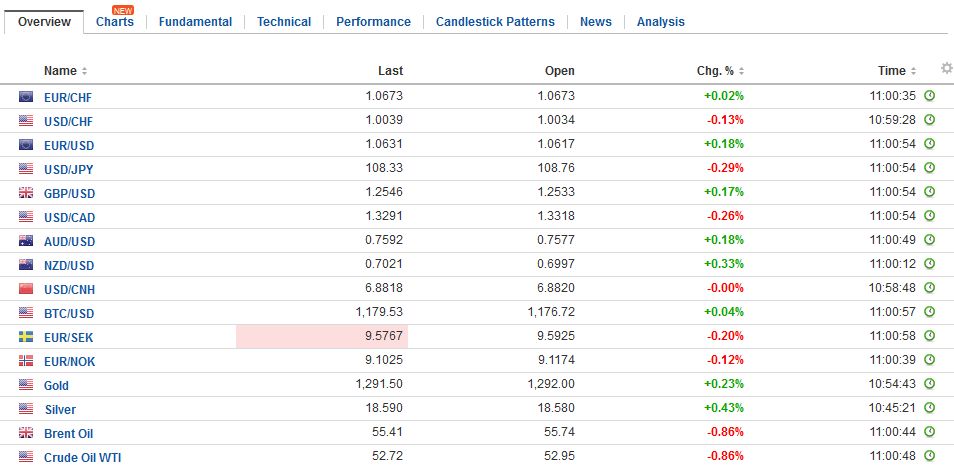

FX Daily Rates, April 17 - Click to enlarge |

| The yen remains the strongest the of the majors. The dollar is trading at new five-month lows, as it approaches the JPY108.00 level. A little below there (~JPY107.85) is the 61.8% retracement of the dollar’s rally since the US election. The 200-day moving average (~JPY108.80) was violated on a closing basis at the end of last week and appears to offer resistance to dollar upticks. Japanese equities, however, did not fall as they often do in the face of yen strength. The Topix gained almost 0.5%, while the Nikkei lagged with a 0.1% gain. Utilities, real estate, and consumer staples did well, while financials, energy, and materials were small drags.

Although political tensions remain high in the region, after North Korea’s failed missile test yesterday, and reports that China is having difficulty reining it in, the Korean won edged higher, for the third session in the past four, and the Kospi gained 0.5%. Foreign investors continue to sell Korean shares, albeit at a slower pace. According to the Korean Exchange, foreign investors sold $15.3 mln worth of Korean stocks earlier today, which is about a third of the average pace seen last week. |

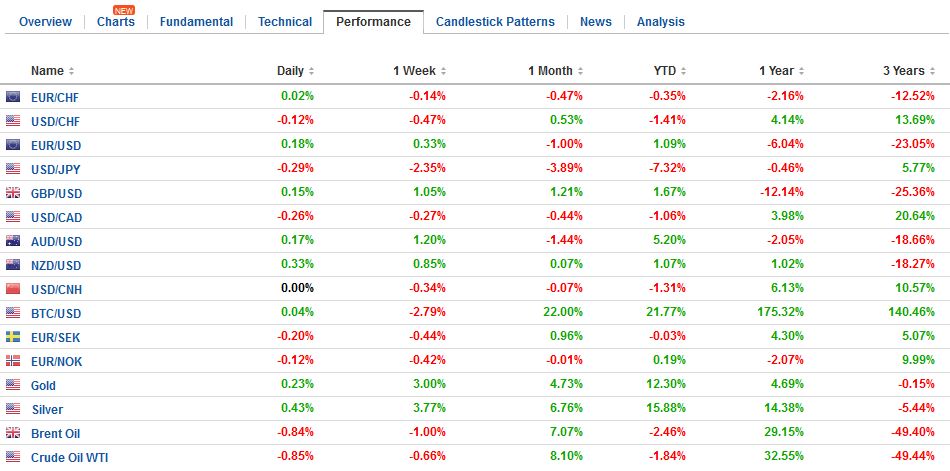

FX Performance, April 17 - Click to enlarge |

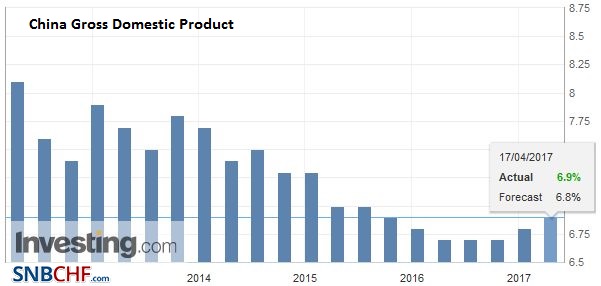

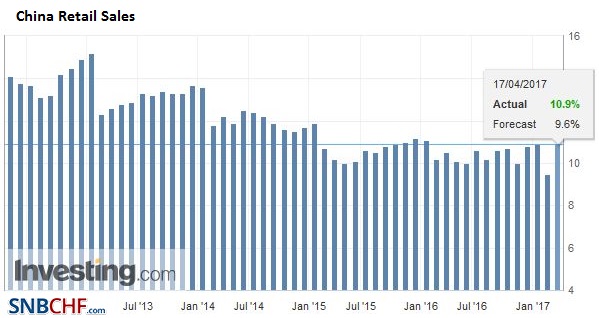

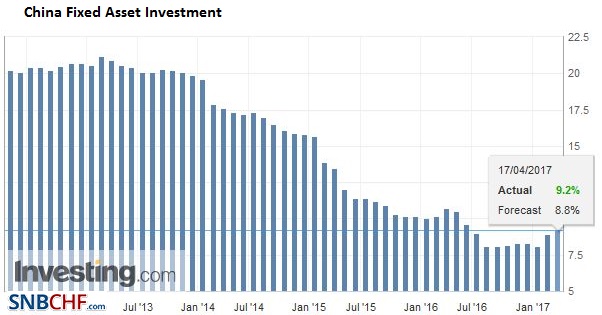

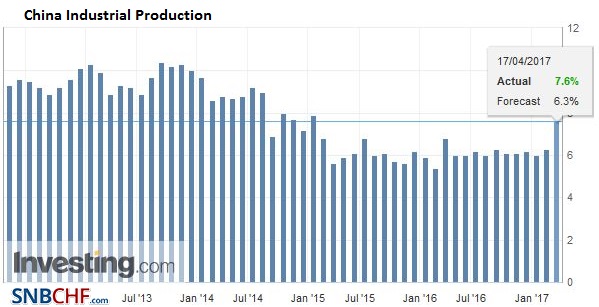

ChinaChina reported a slew of data, culminating in Q1 GDP, which ticked up[ to 6.9% from 6.8%. It is the first back-to-back acceleration in growth in seven years. |

China Gross Domestic Product (GDP) YoY, Q1 2017(see more posts on China Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

| Retail sales, investment, and industrial output rose more than expected. Consumption accounted for a little more than 77% of growth, according to the government’s report. However, there are two worrisome elements. |

China Retail Sales YoY, March 2017(see more posts on China Retail Sales, ) Source: Investing.com - Click to enlarge |

| First, the growth seems to be still debt-driven. Second, several sectors that suffer from excess capacity, like steel and aluminum showed increased output. Higher prices may have encouraged this, but it critical challenge remains. Indeed, iron ore and steel rebar prices have fallen, suggesting that growth is not sustainable. |

China Fixed Asset Investment YoY, March 2017(see more posts on China Fixed Asset Investment, ) Source: Investing.com - Click to enlarge |

| Chinese stocks drew little comfort from the robust data. The Shanghai Composite fell 0.75%. After gapping lower, it successfully tested the 3200 area which has marked the low end of the two-month range. Some cautiousness was linked to regulators attempt to address stock manipulation. We note that with the decline in US yield and the increase in Chinese yields, the 10-year differential is the widest in six months (~120 bp). |

China Industrial Production YoY, March 2017(see more posts on China Industrial Production, ) Source: Investing.com - Click to enlarge |

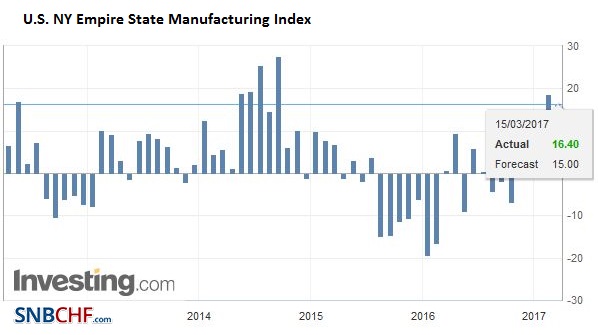

United StatesThe North American session features among the first looks at the start of Q2 with the Empire Manufacturing survey. It is expected to moderate for the second consecutive month. It peaked in February at 18.7 and fell to 16.4 in March. It is expected to have slipped to 15.0 in April. In Q1 16 it averaged -10.9. In Q1 17 it averaged 13.9. As the markets close, the US Treasury will report the TIC data for February. It is of interest to investors, even if it typically does not move the market. Also, after the markets close, the Fed’s Fischer speaks at Columbia University. Separately, reports suggest that Randall Quarles, a Treasury official in the Bush Administration will be shortly nominated as a Vice Chair of the Federal Reserve for bank supervision. This is required under Dodd-Frank, and there had been some speculation that President Trump would not fill the post as part of the push back against the omnibus regulation. |

U.S. NY Empire State Manufacturing Index, April 2017(see more posts on U.S. NY Empire State Manufacturing Index, ) Source: Investing.com - Click to enlarge |

European markets are mostly closed. The initial reaction to Turkey’s referendum, which allows Erdogan to further consolidate his power, was to take the lira higher. It is the strongest currency in the world, up 1.1% against the dollar today. It had initially rallied 2.5%. Some suggest that this lifted the uncertainty that had been weighing on sentiment. The immediate focus shifts to the central banking meeting next week (April 26). Inflation is double the target, and the rate hikes have seen some foreign capital return. According to the central bank, foreign investors bought almost $500 mln of lira-denominated bonds last week. It was the fifth week that foreign investors were net buyers, though their share is near a five-year low.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,$TLT,China Fixed Asset Investment,China Gross Domestic Product,China Industrial Production,China Retail Sales,EUR/CHF,newslettersent,South Korea,Turkey,U.S. NY Empire State Manufacturing Index