Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Overall reserve holdings hardly changed in Q3.

China continues to bleed its reserves from unallocated to allocated.

Sterling’s share of new reserves warns it may be losing some allure.

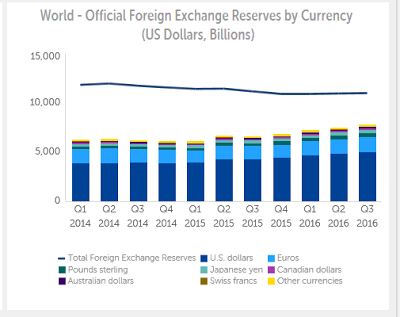

| The IMF is the most authoritative source for reserve holdings of central banks. It reports the data at the end of each quarter with a quarter lag. At the end of last year, the IMF published the Q3 16 reserve figures. As often is the case, the Q3 reserve figures get lost in the holiday shuffle.

Nevertheless, there are a couple of interesting developments. First, though, let review the basics. Overall, the valuation of global reserves rose to a little more than $11 trillion, a $36 bln build on the quarter, but off $182 bln from Q3 15. It is awkward to say, but the $36 bln increase in reserves in Q3 16 is so small that it is practically a rounding error. Currencies did not fluctuate much in the quarter (euro rose almost 1.2%, and the yen rose 1.8%, sterling was off nearly 2.6%), but still could likely account for much of the change. The other important point to recall is that not all central banks report the currency allocation of reserves. Of the $11 trillion of reserves almost $7.8 trillion are allocated, leaving $3.2 trillion unallocated. Of the allocated reserves, the dollar accounts for 63.3%, the euro accounts for 20.3%, the yen and sterling are about 4.5% each, and the Australian and Canadian dollars are 2% each. The Swiss franc and other currencies account for the remainder (~3.3%). Central banks typically move slowly and cautiously when adjusting reserves. However, there is an important development that is taking place. China has agreed to report the allocation of its reserves. However, it is slowly bleeding them in preserve their confidential nature. Allocated reserves rose by $299 bln in Q3. Unallocated reserves fell by a little more than $263 bln. Over the past four quarters, total reserves have fallen by $182 bln. Allocated reserves have increased by $1.19 trillion, while unallocated reserves have fallen by $1.37 trillion. |

Official Foreign Exchange Reserves by Currency - Click to enlarge |

China seems to be the main driver here. Starting with the Q4 16 COFER report, out at the end of March, the IMF will break out the yuan’s allocation. We suspect the yuan’s share of reserves is around 1.5%, despite its inclusion in the SDR.

By a narrow margin of less than two percentage points, the UK voted to leave the EU at the end of Q2 16. There has been a debate about what happens to sterling’s status as a reserve asset going forward. One quarter is hardly sufficient to reach any firm conclusion, especially given the gradual nature of central bank adjustments.

The valuation of sterling reserves rose $1.9 bln in Q3 to $350.8 bln. This is small. Of the increase in allocated reserves, sterling’s share was 0.06%. Sterling’s decline of 2.6% depressed the change but more may be taking place. The volatility of sterling and the decline in Gilt yields (from 1.4% on the eve of the referendum to 50 bp by the middle of August) may have deterred some central banks. There is also the risk that the figures are distorted by China’s selective inclusion of allocated reserves. The situation is worth monitoring in the coming quarters. Over the past four quarters, sterling has accounted for about 3.3% of the allocated reserves, which is a bit lower than the share of overall reserves.

On the other hand, the yen’s share of allocated reserves is rising faster than one might expect. The valuation of yen holdings rose nearly $21 bln in Q3, which is accounts for about 7% of the increase in allocated reserves. Over the four-quarter period, the yen’s share of the increase in allocated reserves was about 8.5%. We suspect that this is largely a function of China. It had been reported a relatively active investor in Japanese debt instruments. The dollar value of yen holdings appears poised to surpass the dollar value of sterling’s holdings (currently GBP=$350.8 bln and JPY=$349.7 bln).

Full story here Are you the author?

Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,newslettersent