Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Fed, BOJ, and BOE meet next week, each may adjust economic assessments in more favorable direction.

Key challenge for many investors is the new US Administration.

US employment, EMU inflation, Q4 GDP, and China’s PMI are among the data highlights.

Three major central banks meet in the week ahead, and there are several important reports due out that will give investors more insight into how the economies have begun the new year.However, the uncertainty surrounding these events and data pale in comparison to known and unknown impulses from the new US Administration.

On one hand, there is little thus far that should be surprising. The executive orders, like freezing new regulations, are what other presidents have done, including Obama, or ideas that Trump supported during the campaign, like withdrawing from TPP, supporting pipelines, the wall on the Mexican border, not funding international activity the support abortions, and limiting immigration by Muslims.

On the other hand, it is not so straight forward. There are no indications that the rhetoric about prosecuting Clinton over her emails is going forward, and in fact, press reports suggest that officials in the new Administration may also be continuing to use private networks and unsecured communication. China has not been cited as a currency manipulator, as Trump had pledged as a Day 1 priority. The freezing of immigrants from several Muslim countries is what Trump supported, but that Saudi Arabia was not on the list, (nor Egypt, Turkey, and Azerbaijan). Despite the role of Saudi nationals in the 9/11 attack, raises questions even from those who support the initiative.

That the freeze includes people with green cards and those in transit, struck many as particularly severe, and a judge sought to limit the impact on some new arrivals. Many airports were scenes of large spontaneous protests. The situation was still playing out Sunday morning. A study by the libertarian Cato Institute found that between 1975 and 2015, immigrants from the seven countries from where immigrants are frozen, have not committed fatal terrorist attacks on US soil. Also, Muslim Americans with family backgrounds in those seven countries have killed no Americans in the past 15 years.

When Trump signed the order to officially end the TPP negotiations, he noted that Clinton also opposed the deal, though during the campaign he accused her of being duplicitous and really supporting the final agreement. Trump also express interest going forward in bilateral agreements rather than multilateral arrangements. Couldn’t TPP form the basis of a bilateral US-Japan free-trade agreement?

Investors are also continuing to wrestle with the conflicting views represented by different Administration officials.The President seemed to endorse actions that are defined as torture, but then said he would defer to Defense Secretary General Mattis, who is opposed. What does it mean to say that NATO is obsolete but important? Some members of the cabinet are more pro-trade than others, and it is not clear who will be the “deciders.”

The rubber meets the road in the middle of March. The debt ceiling is expected to be reached. This is the authorization to pay for what has already largely been spent. It is the bill that comes after the meal. The debt ceiling has been lifted nearly 75 times since the early 1960s. It is part of the US political ritual where Congress uses the debt ceiling as leverage to try to get concessions from the President.

The point man for the White House is the Office of Management and Budget (OMB) Director, Mulaney, who is a deficit hawk. He has gone beyond Trump did in the campaign and suggested that cutting Social Security and Medicare may be necessary. Other campaign promises and other cabinet members are committed to various fiscal actions, including tax cuts and infrastructure, that will likely boost the US deficit (and therefore debt), even if reasonable people differ on the magnitude and duration of the impact.

The Mexican peso was the strongest currency in the world last week, despite the escalation of tensions. The Mexican peso bottomed on January 11 and retested the low on January 19. It rose 3.3% last week and closed well. Since it trended higher consistently last week, it is difficult to know if the news that the two Presidents talked after a scheduled meeting was canceled when Mexico refused to pay for the wall that Trump insists upon the building.

Some suggest that the peso’s recovery was the realization that things could not get worse, though given when the peso bottomed, things have gotten worse, with a suggestion that among things the US could do to get Mexico to pay for the wall was a 20% tariff on Mexico’s exports to the US. While this seems far-fetched, as we have noted, the US President can impose a 15% temporary tariff under conditions of a balance payments emergency.

Given the complicated continental trade where a part could cross the border several times, the law of unintended consequences risks significant economic dislocations in the US. Other suggest it is the Negotiator in Chief posturing. Consider this: before last week’s peso’s gain, since the beginning of 2016, the peso had depreciated by more than a fifth, partly driven seemingly by Trump’s comments, which if sustained would seem to offset some of the sting of a tariff.

This is Trump’s first tangle and one that he prioritized. It is important that he wins it from a political point of view. The wall is of great symbolic value. It is a campaign promise that many of his supporters appear to have taken literally.

The Federal Reserve, the Bank of England and the Bank of Japan hold policy meetings in the week ahead. None of the central banks are likely to take fresh action. Each may be somewhat more upbeat than previous statements.

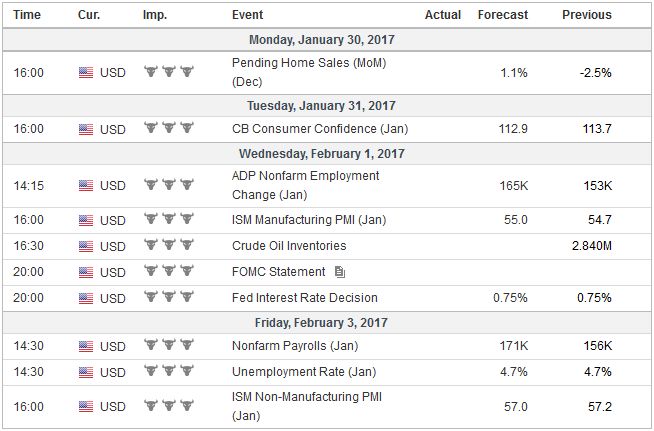

The US economy moderated more than expected in Q4 16 after a 3.5% annualized clip in Q3 16. However, the best measure for underlying economic signal excludes inventories and net exports. This measure of final domestic sales accelerated to 2.5% from 2.1%. The Fed’s statement will also likely recognize that increased inflation expectations. The five-year breakeven is above 2% for the first time in a couple of years, and the three-year breakeven looks set to cross that threshold in the days ahead. The uncertainty surrounding the fiscal initiatives of the new US Administration has not been lifted. It seems unreasonable to expect anything about the balance sheet to be including in the statement. This may be addressed at the mid-March meeting (around the time of the debt ceiling), if not directly than at the press conference.

After rallying into the last FOMC meeting, the dollar has pulled back in recent weeks. The euro’s five-week and roughly 4.4% was snapped last week with a 0.05% loss. Since the last FOMC meeting, the only one of the major trading partners that the dollar has appreciated against is the peso (2.65%). It has fallen against the euro (2.8%), Canadian dollar (1.4%), and Chinese yuan (1.0%). The Federal Reserve is unlikely to feel compelled to discuss the dollar.

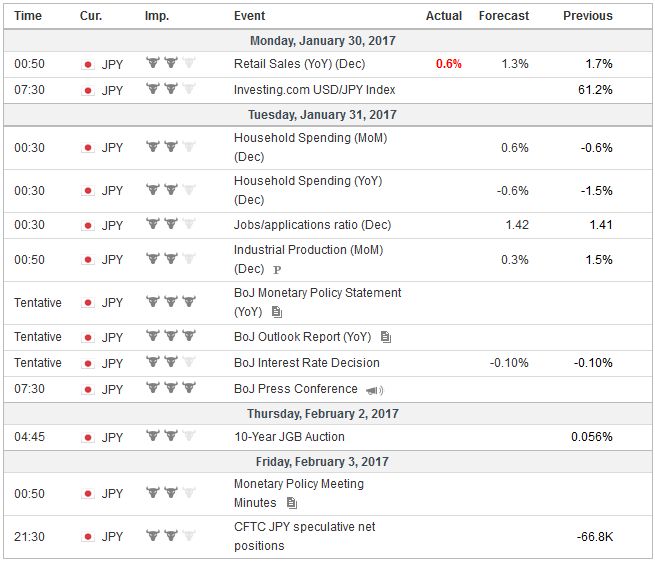

JapanThe Bank of Japan meets. The rise in global interest rates is pulling up Japanese rates, requiring the central bank to defend its +/- 10 bp target range. The BOJ may upgrade its economic assessment after stronger than expected exports and industrial output. It may be too early to expect the BOJ to upgrade its inflation outlook, but even many private sector economists suspect the worst of deflation is passed. |

Economic Events: Japan, Week January 30 - Click to enlarge |

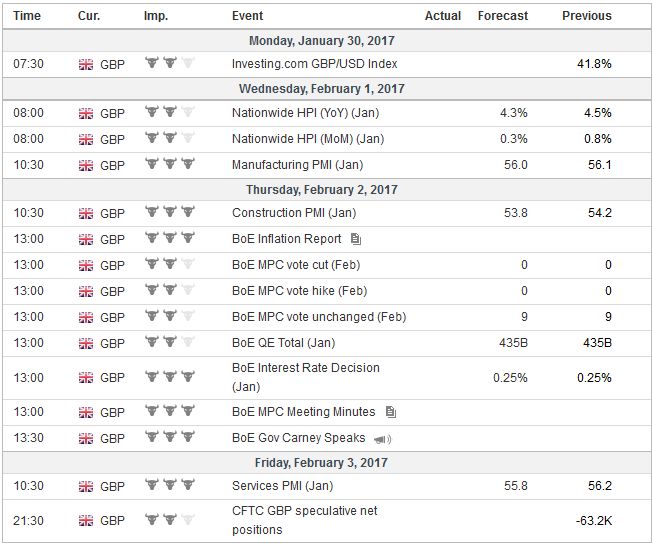

United KingdomThe Bank of England meets. Although some talk about the central bank’s neutral stance, it is still engaged in buying Gilts and corporate bonds. It has been fairly successful in purchasing corporate bonds and may achieve its objective earlier than had been anticipated. There could be some update of operational issues. It is true that the risk of a rate cut has slackened considerably since last summer, and that the next move is likely to be an increase. The decision to keep rates on hold will likely have unanimous support. The risk is that the BOE turns more upbeat at exactly the wrong time. The official forecasts for this year and next are above the median forecast (1.4% vs. 1.2% and 1.5% vs. 1.3% for official vs. median for 2017 and 2018 respectively). |

Economic Events: United Kingdom, Week January 30 - Click to enlarge |

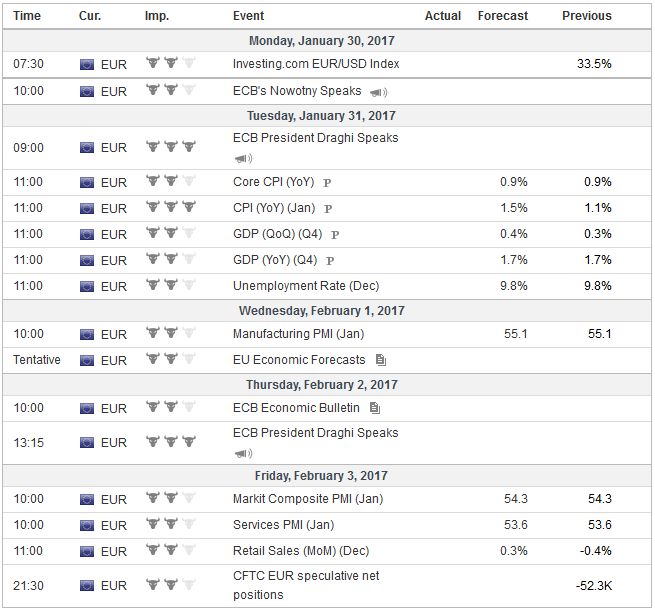

EurozoneHeadline eurozone inflation is rising. It rose 1.1% year-over-year in December after a 0.6% pace in November. The first estimate for January is expected to be 1.4%-15%. The ECB target is near but below 2%, but Draghi has been emphasizing the core rate which is expected to remain unchanged at a subdued 0.9% pace. It bottomed at 0.6%. He is opposed to reconsidering the decision made last month to extend the asset purchases through the end of this year but at a 60 bln euro a month pace rather than the current 80 bln that run through March based on the recovery in oil prices. We have made the point before, and it is worth making again: In lieu of offsetting stimulus policies by Germany, or the structural reforms that Draghi repeatedly demands, Germany inflation running a bit above the periphery is helpful in boosting the competitiveness of the periphery. That said, ideas that an Italian election could be held in June, now that the Court ruling leaves both chambers with a proportional representation system, suggests Italian bonds will continue to underperform. We suspect that the economies and prices will evolve to allow the ECB to consider tapering further in late-Q3 or early Q4. The eurozone also reports its first estimate of Q4 GDP. The data suggests growth of 0.4%-0.5% growth, which would keep the four quarter pace steady in the 1.8%-1.9% range that has been sustained since the middle of 2015. Growth is not spectacular, but it is solid and above what economists estimate to be the trend pace. The PMIs suggest the momentum has been sustained into early 2017. Unemployment is stubbornly easing in Greece, Italy, and Spain, but in the aggregate the unemployment area in EMU is expected to have remained at 9.8% in December for the third consecutive month. |

Economic Events: Eurozone, Week January 30 - Click to enlarge |

ChinaAlthough the Lunar New Year holiday runs through the week, China will report the manufacturing and the non-manufacturing PMI, and Caixin will report its manufacturing PMI. The manufacturing surveys are expected to soften slightly (0.1-0.2 points) with little significance. Both are expanding between 51-52. The non-manufacturing PMI rose 54.5 in December, which was the second best reading (after November 54.7) in a couple of years. Officials in Beijing are likely watching the new US Administration closely, perhaps through the prism of the Chinese saying about killing a chicken to scare the monkeys. The onshore yuan has appreciated by almost 1.0% this month, and the onshore yuan has risen by 1.5%. Since the squeeze that appears to have been engineered by the PBOC at the start of January, the offshore yuan is trading at a premium to the onshore yuan, suggesting speculative pull has been neutralized, at least for the time being. The evolution of the relationship in a stronger US dollar environment may be an important test. |

Economic Events: China, Week January 30 - Click to enlarge |

United States

|

Economic Events: United States, Week January 30 - Click to enlarge |

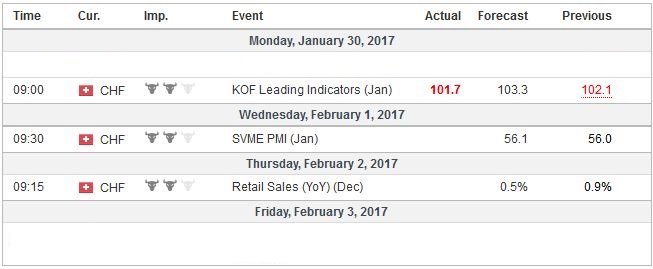

Switzerland |

Economic Events: Switzerland, Week January 30 - Click to enlarge |

Full story here Are you the author?

Tags: #USD,Bank of England,Bank of Japan,Federal Reserve,jobs,MXN,newslettersent