Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

EUR/CHF - Euro Swiss Franc, January 24(see more posts on EUR/CHF, ) - Click to enlarge |

GBP/CHFThe Supreme Court ruling is finally upon us this morning which will determine whether or not UK Prime Minister Theresa May can invoke Article 50 to commence exit negotiations without as Act of Parliament. With so many political forces at work and a movement to keep Britain with as close ties as possible to the single market this case carries major implications for the pound. There are a large number of MP’s who would like to keep Britain in the single market. GBP/CHF has remained at the lower levels for the last few months with levels trading around 1.25 for this pair. In my view the Supreme Court ruling is likely to create new direction for the pound. If Theresa Mya wins the appeal it will provide clarity but it will also mean that a hard Brexit is very much on the cards which would mean coming out of the single market. The hard Brexit option is likely to see the pound weaken in the short term in my view. Economic data for the UK is light today with UK public sector net borrowing numbers although these are likely to be overshadowed by the court case this morning. Swiss trade balance data is released on Thursday which will give us some more idea as to how well the Swiss economy is performing. The issue of Brexit will largely dominate as far as GBP/CHF is concerned though so the next few months will see considerable movement. Those clients selling Swiss Francs may wish to consider moving sooner rather than later to take advantage of the excellent prices which are currently available. |

GBP/CHF - British Pound Swiss Franc, January 24(see more posts on GBP/CHF, ) - Click to enlarge |

FX RatesAs widely expected, the UK Supreme Court ruled that Parliament approval is needed to trigger Article 50 start the divorce proceedings with the EU. The Court decided by an 8-3 majority that a bill needs to be submitted to both chambers, but that the approval of the regional assemblies (e.g. Scotland, Northern Ireland) is not necessary. A bill is more onerous than a motion in that not only are both chambers involved, but amendments can be added that further condition. This appears to be Labour’s strategy; not to oppose the triggering of Brexit, but ensure a larger role for parliament to ensure it is integral in the process. Two elements that could work in favor of the government is the fact that it was not a unanimous decision and that the regional assemblies have not a role. The former had been anticipated, though some reports suggested a 7-4 decision. The latter had greater potential to disrupt May’s timetable given the recent collapse of the Northern Irish assembly. The issue now becomes parliamentary in nature in the sense that the government will craft a bill to minimize the scope for amendments, and which amendments are discussed and for how long. The Tories have a small majority in the House of Commons, and the challenge will be for an amendment to find sufficient support. Initially, at least, the Supreme Court ruling ought not to push back May’s end of a Q1 target for triggering Article 50 |

FX Daily Rates, January 24 - Click to enlarge |

| Sterling fell from a little above $1.2500 to a little below $1.2440 on the news and recovered quickly.The low met the 38.2% retracement objective of the rally from the pre-weekend low, leaving our constructive outlook intact. Recall yesterday that sterling rallied from around $1.2380 to almost $1.2540. Important chart support is seen in the $1.2400-$1.2415 area, and a break of it would undermine our outlook.

The euro also made a marginal new multi-week high (~$1.0772) before hitting a wall of offers that sent it back to $1.0735. Trading is choppy, and ranges are narrow. Although we still read the technical indicators as suggesting that the euro’s upside correction may be in its last stages, the underlying tone still is firm. A break of the $1.0700 area and, ideally, the $1.0660-$1.0680 area is needed to boost the chances that a high is in place. |

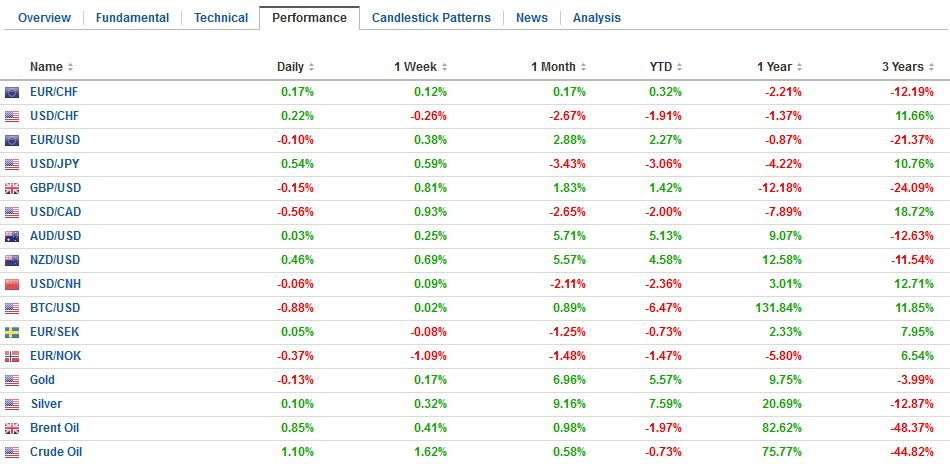

FX Performance, January 24 - Click to enlarge |

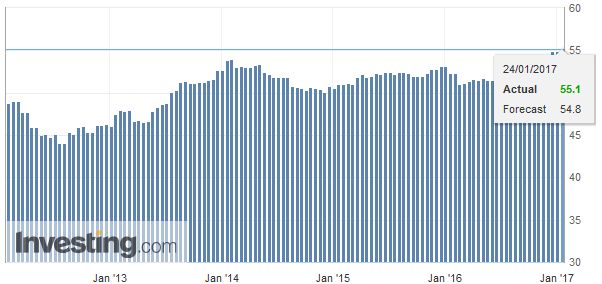

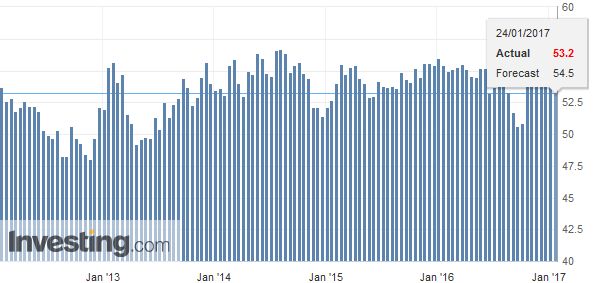

EurozoneTurning to the eurozone, the flash January PMI was reported. Two details, in particular, were notable. Employment is at its best level in nine years, and forward-looking new orders also rose. Also, there were some signs of pricing power from suppliers, which likely reflects the rise in commodity prices. Import prices may also have been lifted by the euro’s depreciation. |

Eurozone Manufacturing Purchasing Managers Index (PMI), December 2016(see more posts on Eurozone Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

| The composite reading of 54.3, down ever so slightly from the 54.4 December reading is consistent with continued steady growth. |

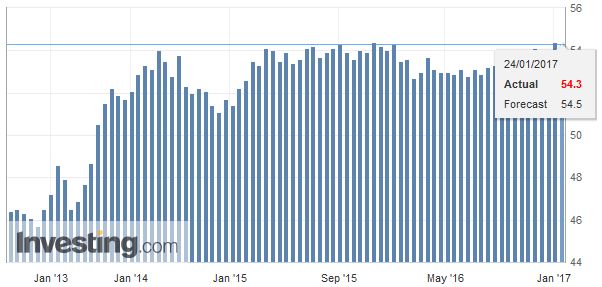

Eurozone Markit Composite Purchasing Managers Index (PMI), December 2016(see more posts on Eurozone Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

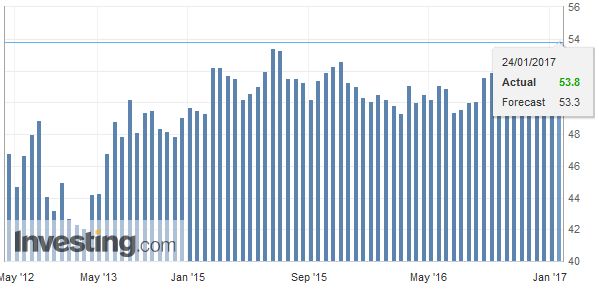

FranceAlthough it will do little to change the dialogue ahead of the April election, France’s composite reading of 53.8 is the highest in this short time series (three-years-old). Consider that last January the composite was at 50.2, and in June it was at 49.6. |

French Markit Composite Purchasing Managers Index (PMI), December 2016 Source: Investing.com - Click to enlarge |

| The gains came from services not manufacturing. |

France Services Purchasing Managers Index (PMI), December 2016(see more posts on France Services PMI, ) Source: Investing.com - Click to enlarge |

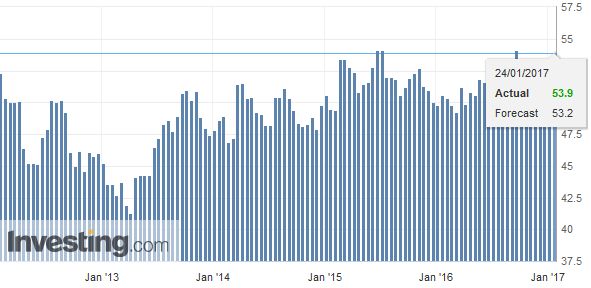

GermanyBy contrast, the German composite slipped to 54.7 from 55.2. We would not want to make a big deal of the decline in German composite reading. The average from Q4 16 was 55.1 and Q3 53.8. The 12-month average is 54.3. |

Germany Composite Purchasing Managers Index (PMI), December 2016(see more posts on Germany Composite PMI, ) Source: Investing.com - Click to enlarge |

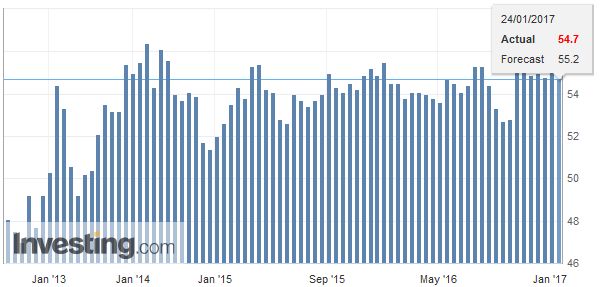

| Services were a drag, falling to 53.2 from 54.3. |

Germany Services Purchasing Managers Index (PMI), December 2016(see more posts on Germany Services PMI, ) Source: Investing.com - Click to enlarge |

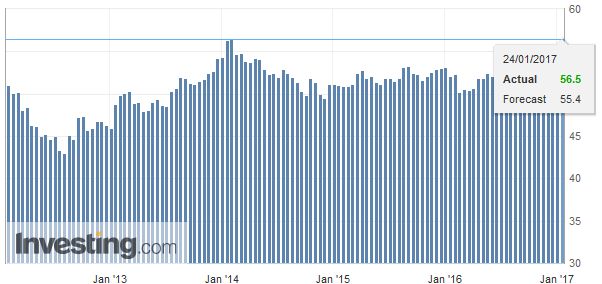

| Manufacturing, on the other hand, rose to 56.5 from 55.6, matching its record high set in January 2014 |

Germany Manufacturing Purchasing Managers Index (PMI), December 2016(see more posts on Germany Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

JapanJapan’s preliminary manufacturing PMI was also reported. It rose to a three-year high of 52.8 (from 52.4). It bottomed last May near 47.7. The average from Q4 16 was 51.7 and Q3 49.7. This is consistent with our anticipation that the Japanese economy has some positive momentum to start the year. The dollar’s recent losses were extended marginally against the yen in Asia before it recovered. Yesterday’s low was about JPY112.70 and last week’s low was JPY112.60. In Asia, the dollar was sold to nearly JPY112.50. Near-term potential extends to JPY113.50, while a move above JPY113.70-JPY114.00 may be an early indication that a low may be in place. |

Japan Manufacturing Purchasing Managers Index (PMI), December 2016(see more posts on Japan Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

United States

Helping the dollar today is the recovery in US yields. Recall that last week; the 10-year yield fell to 2.30% before poking through 2.50% before the weekend. It fell to 2.40% yesterday and now is up a few basis points today. Investors are still waiting for more details about the infrastructure spending, deregulation, and tax cuts. Yesterday’s executive orders, including the federal hiring freeze and the prohibition of US funds being used by foreign organizations that facilitate abortions, are traditional Republican positions.

The freeze on what was called run-away federal hiring may be less than meets the eye. While there was a small increase in federal hiring over the past few years, in the larger picture that is not where the government has grown. Indeed, the federal government directly hires about 2.7 mln employees. This is roughly the same as 50 years ago.The real growth of the government’s workforce is on the state and local level. In 1966, there were about 7.8 mln Americans working for state and local governments. Now there are roughly 19.5 mln.

The formal withdrawal from TPP was well-telegraphed. The effort to renegotiate NAFTA was not a surprise. Note that Obama wanted to renegotiate NAFTA and thought that by including Mexico and Canada into the TPP, it would accomplish the objective of modernizing the agreement.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,$EUR,$JPY,Brexit,EUR/CHF,Eurozone Manufacturing PMI,Eurozone Markit Composite PMI,France Manufacturing PMI,France Services PMI,gbp-chf,Germany Composite PMI,Germany Manufacturing PMI,Germany Services PMI,Japan Manufacturing PMI,Japan Manufacturing Purchasing Managers Index,newslettersent