Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

EUR/CHF - Euro Swiss Franc, January 23(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesThe US dollar had a poor close in the North American session before the weekend as investors appear increasing anxious about the new US Administration’s economic policies and priorities.With no fresh details emerging over the weekend, some stale dollar longs exited. The dollar stabilized in the European morning, but broader risk appetites were not rekindled, and the Dow Jones Stoxx 600, led by financials, was sold to its lowest level this month. Asian shares did better, with the MSCI Asia Pacific Index snapping a two-day decline by rising nearly 0.2%. However, Japanese shares were heavy, and the three-day rally in the Nikkei and Topix ended with 1.2%-1.3% loss, the second biggest this month. All sectors were lower, and although some report suggests exporters were the hardest hit, which may be the telecoms on the Topix and consumer discretionary on the Nikkei, the real estate sector in both indices were down nearly as much. Moreover, other markets that might suffer from the shift represented by Trump’s “America First” rhetoric, including China, Taiwan, South Korea, and Singapore markets rose. |

FX Daily Rates, January 23 - Click to enlarge |

| Bond markets are mostly firmer. The US 10-year yield is increased by over 20 bp last week, though pulled back in late pre-weekend activity to finish a little below 2.47%. Today it fell below 2.43% before steadying in Europe. European bond yields are mostly lower. Italy and Portugal are lagging. British, German and Swedish 10-year yields are off two basis points.

Sterling has been bid through its recent highs. At its best level today (~$1.2470) it was the strongest in a month (December 19). The move above the $1.2425 area is constructive from a technical vantage point. There is a possible head and shoulder bottom pattern whose neckline has been taken out (~$1.2430) that would project toward $1.2830, which is above the December 6 peak near $1.2775, though approximates the 6.18% retracement of the sharp decline since the early September peak near $1.3450. The Australian dollar has been the strongest currency this month, advancing almost 5% this year. However, it is a laggard today, being almost flat against the greenback. Some bulls may have been deterred by the continued retreat in iron ore prices. The 2.6% decline in China today brings the four-day slide to nearly 5.5%. Reports suggest its new high-grade supply (and Brazil’s) may be spurring the unwinding of the early rally. Other industrial metals (copper and aluminum) are higher today, and gold is at its highest level since late November. Gold has been down only two sessions since January 3 and has risen four consecutive weeks. The $1230 area corresponds with a 50% retracement of the post-US election losses. |

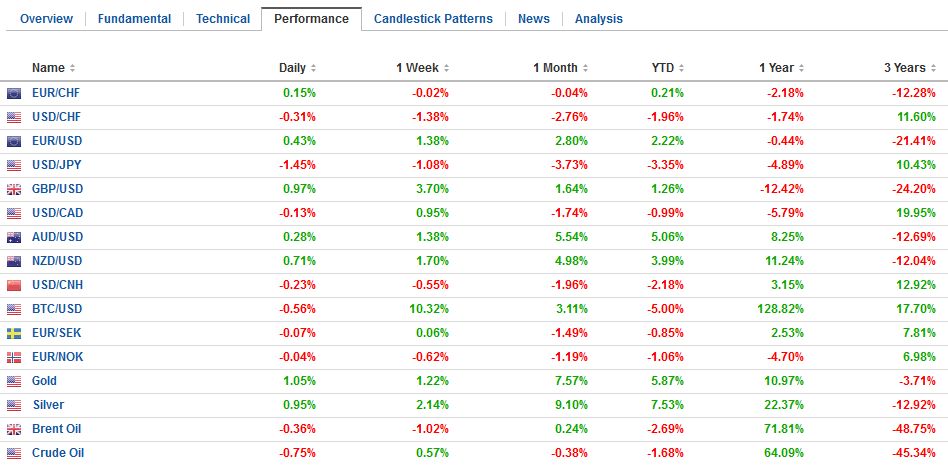

FX Performance, January 23 - Click to enlarge |

EurozoneFrance is trailing Germany. Yesterday’s Socialist Party primary set the stage for a run-off between former Prime Minister Valls and the former Education Minister Hamon next Sunday. The French presidential election may be heating up. Le Pen has a solid base and is widely touted to make it into the second round. The center-right Republican Fillon has been the favorite to lead the mainstream to stop the National Front in the second round. However, Macron may get a bump if the Socialist go left, giving him the middle ground. Elsewhere we note that S&P affirmed its rating and outlook for Greece before the weekend, and this is helping lift Greek bonds today. The 10-year benchmark is off 5-8 bp. The new week has begun off with a little fresh news. It does not get better in the US today. There are no economic reports, and the Fed’s ‘cone of silence” descends ahead of next week FOMC meeting. While some may see a new era in reports that Foxconn, the manufacturer, is considering teaming up with Apple to build a $7 bln display factory in the US, news of the first drone strike (in Yemen) under President Trump suggests some elements of continuity. The euro’s recent gains were extended to $1.0755 in Asia. This is the highest level for the euro since December 8. The $1.0710 area stalled the euro at the beginning of last week, which corresponds to a 38.2% retracement objective of the euro’s losses since the US election. The 50% retracement is near $1.0820. The high from the ECB’s December meeting, which saw the asset purchases extended for nine months rather than six but at a reduced pace, was near $1.0875. On the downside, a break of the $1.06 50-$1.0670 is needed to suggest a top may be in place. |

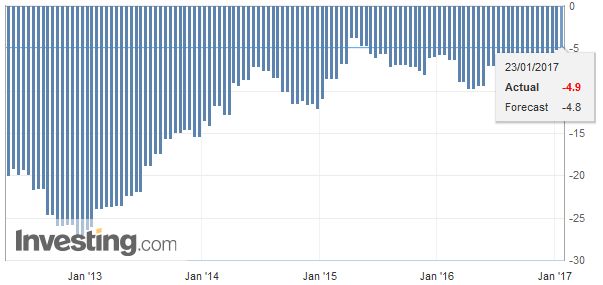

Eurozone Consumer Confidence, December 2016(see more posts on Eurozone Consumer Confidence, ) Source: Investing.com - Click to enlarge |

The Japanese yen is the strongest currency today, gaining nearly 1% against the dollar. Thus far, the dollar held above the seven-week low set last week around JPY112.60. Today’s low was set in Asia near JPY113.20. The intra-day technical indicators look soft, and at this juncture, only a move above JPY113.75 would lift the tone.

The NAFTA currencies–Canadian dollar and Mexican peso– are higher today. Re-opening NAFTA was signaled as a priority of the Trump Administration. It is not clear when the announcement will be made, but it could be this week. The US dollar bounced from nearly CAD1.30 at the start of last week to almost CAD1.34 before the weekend, edging through a 61.8% retracement of a leg down that began in late December. Initial support now is seen near CAD1.3240. The US dollar appears to have put in a double top against the Mexican peso near MXN22.00. The neckline is around MXN21.50; giving a minimum measuring objective of MXN21.00. The MXN21.10 area also is where the 50% retracement of the dollar’s rally since around the mid-December FOMC meeting.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,Eurozone Consumer Confidence,MXN,newslettersent