Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Odds of a March Fed hike edged up last week, and Q4 GDP figures were revised higher.

Many continue to expect the new US Administration to pursue pro-growth tax reform, deregulation and infrastructure spending.

Although many other high income countries are growing, near trend divergence of monetary policy continues.

United StatesThe major US equity indices reached record highs before the weekend even if the Dow 20000 level was just out of reach.Following news of a stronger than expected rise in hourly earnings, US yields rose, and after an initial stumble, the dollar recovered on closed on its highs. The underlying narrative that explains and justifies these broad trends stands on four legs. First, that the US economy is expanding at a sufficient clip to spur some price pressures, including, as we saw in the employment report, hourly earnings. (2.9% year-over-year, a new cyclical high, though below past recoveries and expansion levels). Second, that the economic policies of the new Administration will be pro-growth in the form of de-regulation, tax changes, and nationalist economic policies. Third, that other high income countries are expanding at least near-trend, and price pressures appear to have bottomed. Fourth, populist-nationalist forces will be featured on the European political stage, posing the last expression of the existential threat. The headwinds on the US economy abated in the middle of last year. The economy expanded at a 3.5% annualized rate in Q3 16 and, while it likely slowed, with less of a contribution from consumption, and a drag from net exports, recent data prompted upward revisions to the Atlanta Fed GDP tracker to 2.9% for Q4. The Bloomberg consensus is 2.3%, while the NY Fed’s tracker has it at 1.9%. Some economists are suggesting there is better than a one in three chance of a Fed hike in March, while the CME estimates that the Fed funds futures currently discounts about a one in four chance. The December retail sales data that will be reported on January 13 will give no reason to doubt basic scenario. The headline may be flattered by the better than expected vehicle sales and the increase in gasoline prices. The GDP should rise around 0.3%, consistent with consumption rising at a slightly than the 3.0% pace in Q3. |

Economic Events: United States, Week January 09 - Click to enlarge |

EurozoneIn Europe, the main feature is November industrial output reports. Industrial output in the UK and eurozone is expected to have risen by 0.5%-0.6%. The main difference is in year-over-year pace. The eurozone’s pace may more than double from the 0.6% clip seen in October. The UK’s industrial output my turn positive (~0.5%) after contracting (-1.1%) in October. |

Economic Events: Eurozone, Week January 09 - Click to enlarge |

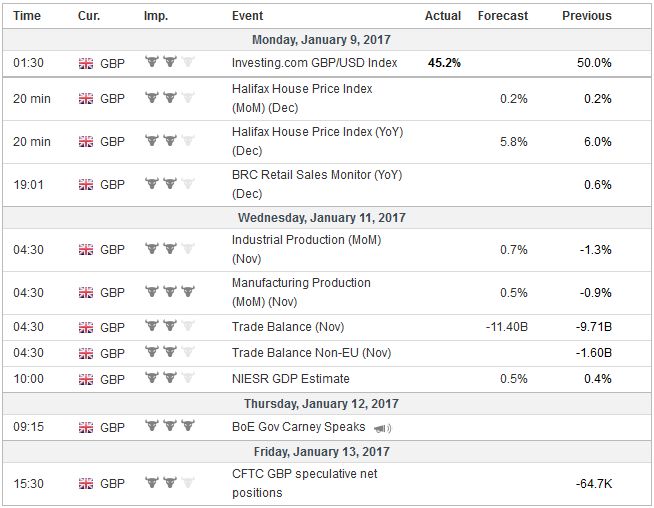

United KingdomSeparately the UK reports the November trade figures. The UK deficit is expected to widen out toward GBP3.5 bln from just below GBP2 bln in October. The average monthly shortfall this year has been GBP3.44 bln vs. GBP2.66 bln in 2015. Also, Sweden and Norway report CPI. Sweden, where the central bank is still pursuing very aggressive unorthodox monetary policy is likely to see a further rise in inflation. It is expected to rise 0.4%-0.5% on the month for a 1.6% year-over-year pace, the fastest in four years. Even with a 0.1% decline in the Norway’s monthly consumer prices, the year-over-year rate may still rise to 3.8% from 3.5%. |

Economic Events: United Kingdom, Week January 09 - Click to enlarge |

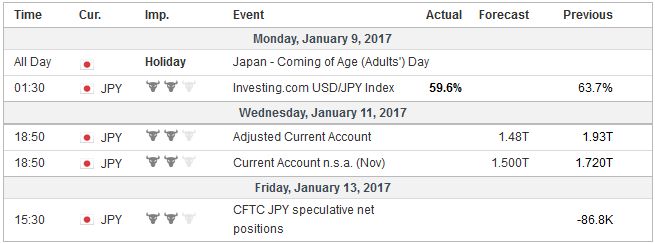

JapanJapan reports its November balance of payments. It typically deteriorates in November compared with October. This has been the case without exception since 2006. Before then, it had often improved. Many observers focus the yen’s impact through the trade channel, but given Japan’s large holdings of foreign assets, the pullback in the yen will boost the investment income balance, arguably more directly than the trade balance. |

Economic Events: Japan, Week January 09 - Click to enlarge |

ChinaIn 2015 and early 2016, Chinese developments rattled the investors; now considerably less so.However, the powerful short squeeze engineered by PBOC officials does not appear aimed at reversing the yuan’s decline as much creating a powerful disincentive for speculators to think it is a one-way bet. In the larger picture, the same fundamental considerations that we think will underpin the dollar against the major and emerging market currencies are at work with the yuan as well. That means that we expect the yuan to move lower on a trend basis. Nevertheless, the near-term outlook is a bit of cat-and-mouse with Chinese officials and how persistent it wants to be. As painful as it was for some players last week, the second that officials appeared to back off, they jumped right back into the fray. China reported that reserves fell by a little more than $41 bln in December to $3.01 trillion. It is the smallest in decline in three months, and in line with market expectations. Interestingly, the debate about China’s reserves has transformed from it having too much to wondering if it has a sufficient level of reserves. Also, because the opaqueness of China’s intervention, in the derivatives market or forward market, forward market, for example, more reserves may be encumbered (committed). China is expected to report inflation figures and the December trade surplus. China’s CPI has gradually firmed. The 24-month average in November was 1.7%, while the 12-month average 2.0% and the three-month average may tick up to 2.2% in December. It is the PPI that is surging. Recall it was negative (deflationary) for five years through late Q3 16. After turning positive in September (0.1%) it jumped to 1.2% in October and 3.3% in November. It is expected to rise toward 4.6% in December. Often when producer prices rise faster than consumer prices, investors get concerned about profit margins. Some economists also talk about pipeline inflation, but this seems to be more an exception than the rule. China’s trade surplus is expected to edge toward $47.5 bln from $44.6 bln in November. Exports likely deteriorated after edging 0.1% higher year-over-year in November. The improvement likely stems from a slowing in imports. China’s monthly trade surplus is fairly stable. The three, 12, and 24-month averages converge between $44.3 and $46.5 bln. Separately China may also report that credit expansion slow, but remains elevated. Consider that this year’s monthly average of aggregate social financing is CNY1.46 trillion compared with CNY1.27 in 2015. |

Economic Events: China, Week January 09 - Click to enlarge |

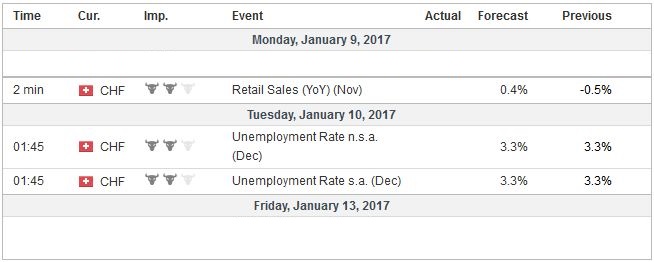

Switzerland |

Economic Events: Switzerland, Week January 09 - Click to enlarge |

Brazil

Brazil’s central bank began its easing cycle last October and had a follow-up rate cut in November.The consensus calls for a 50 bp cut in the 13.75% Selic rate. The US dollar has been trending lower against the real since early December and by the end of last week had returned to near where it was trading before the US election. We suspect the move is exhausted or nearly so. Just as a year ago, the market may have exaggerated the negatives, it seems that the positives may be exaggerated now. The dollar finished last week near BRL3.2225. We see risk in the coming week or two toward BRL3.30.

Lastly, we note three political issues that may become talking points in the days ahead. First, the tensions between Greece and the EU has eased since the middle of December, and a new tranche of aid is expected shortly. Greece’s 10-year bond yield fell 25 bp last week to bring the decline to about 45 bp since Christmas Eve. Note that investors will likely learn in the days ahead that Greece is still experiencing deflation. Greece will also report November industrial output (6.8% year-over-year in October) and October unemployment (23.1% in September). Meanwhile, Greece’s privatization efforts appear to be progressing with the sale of a 51% stake in the Piraeus ports to a Chinese company while has been managing a couple of piers.

Second, a decision by the UK Supreme Court on the royal prerogative regarding triggering Article 50 to begin the formal negotiations for leaving the EU is expected over the next couple of weeks. Prime Minister May confirmed two things many investors have suspects: that there were not plans for Brexit before the referendum and that the UK will leave the single market. This may weigh on sterling, which lost more than 1% before the weekend to fall for the fourth week in the past five. Separately, we note that a 24-hour London Underground strike will make for difficult commutes on Monday.

Third, the US Senate is set to begin taking up the President-elect’s nominations. Although it is widely recognized Presidents’ prerogative to pick their own advisers and cabinet, many of the nominees are particularly contentious for Democrats, and some Republicans may challenge a couple of the nominees as well. The process begins in earnest with a Senator Sessions (Republican from Alabama) nomination for Attorney General. Sessions’ views on civil rights, including voting rights, same-sex marriage, and immigration, as well as Trump’s proposal to establishing a registry of Muslims and imposing a ban on their immigration, will make for a particularly heated hearing.

Full story here Are you the author?

Tags: #GBP,#USD,$CNY,$EUR,Brazil,China,Greece,newslettersent,US