Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Jonathan Watson

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitter

Swiss Franc |

EUR/CHF - Euro Swiss Franc, January 06(see more posts on EUR/CHF, ) - Click to enlarge |

|

I am reading a lot about the pound in 2017 which is likely to be as volatile as in 2016. But the Franc is a harder beast to predict. Loosely tracking the euro but subject to its own rules and trends GBP/CHF could be an interesting pair to watch in 2017. There are numerous global events which can shape the direction on the Franc and clients looking to exchange pounds into Francs or move Francs back to the UK should be considering the path ahead. As a safe haven currency the Franc is seen by investors as a safe bet and will often perform well in times of global and economic uncertainty. In the past the Swiss National Bank have cut their base interest rate into negative territory to help fight the strength of the currency. I think that 2017 could see them be forced to act further on such moves as global uncertainty piles pressure on the Swiss currency. But despite cutting interest rates the Franc will still strengthen as investors avoid the Euro and the pound. Global uncertainty can include for example wars but also political uncertainty. I foresee increased Russian aggression in Europe which will put pressure on the strained NATO relations. I also foresee increased political uncertainty in the Eurozone as the sentiments that predicated the UK’s Brexit vote are mirrored across the continent. Nationalist uprisings in France, Holland and Germany are all gathering pace and even if 2017 isn’t the year they take power I do feel that this trend towards less international cooperation will help the Franc. Couple all of this with the likelihood sterling is in for a rough ride and I think GBP/CHF will soon be back towards 1.20 or potentially lower, I would estimate by the end of March. If you need to buy the Franc there is potentially going to be a spike once the UK’s Supreme Court decision is finalised this month, assuming the decision goes the way of the previous decision then sterling should rally. However once the dust settles on this decision I expect the pound to come under renewed pressure and GBP/CHF to fall. If you need to buy CHF I would move sooner or on any spikes, if you are selling the Swissie to buy pounds some patience might prove rewarding. |

GBP/CHF - British Pound Swiss Franc, January 06(see more posts on GBP/CHF, ) - Click to enlarge |

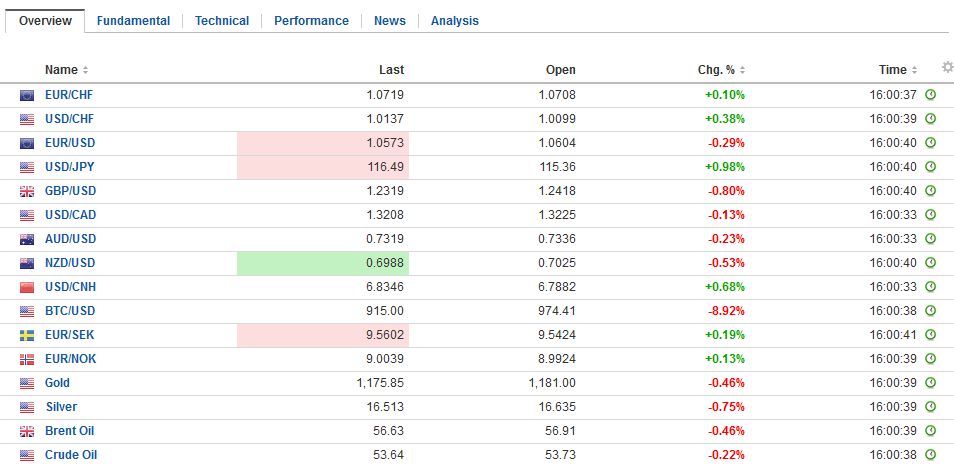

FX RatesThe US dollar is consolidating yesterday’s losses against the major currencies, giving it an apparently firmer tone today ahead of the monthly employment report. Even though the Turkish lira continues to be sold to new record lows, the focus in the emerging markets in recent days has been the Mexican peso and Chinese yuan. |

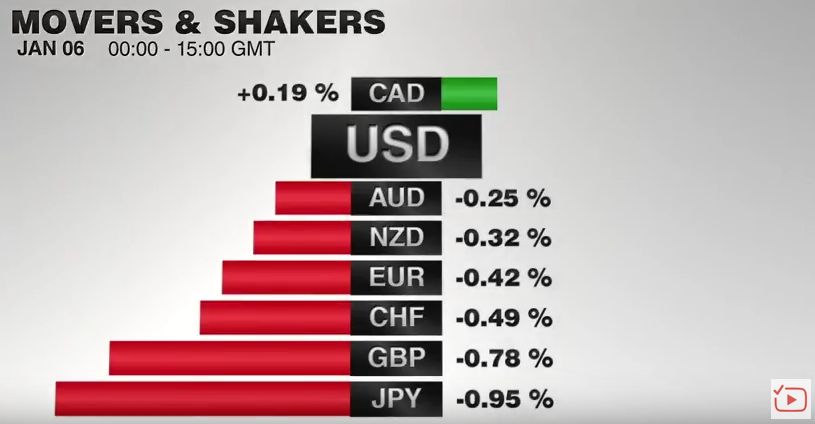

FX Performance, January 06 2017 Movers and Shakers Source: Dukascopy - Click to enlarge |

| The FTSE 100 is at risk of snapping eight-day advance. Real estate, information technology, and financials are leading the advance, while utilities, consumer discretionary and energy are among the largest drags. Whether it manages to extend the winning streak or not may prove to be a function now of the market’s reaction to the US jobs data. |

FX Daily Rates, January 06 - Click to enlarge |

| The US Treasury market is also stabilizing after yesterday’s rally that saw the 10-year yield fall nine basis points, the most since late June, following the UK’s referendum and a little below the level that prevailed before the FOMC decision last month to hike its Fed funds target range. JGBs were unchanged, while European bond yields are mostly firmer. We note that DBRS is the only rating agency recognized by the ECB that accepts that Portugal is an investment grade credit. It has suggested that rising yields are credit negative and the 4% yield threshold is seen as important. The 10-year Portuguese benchmark pushed above there yesterday, it is slightly below there now, while the generic yield is still a couple of basis point north of it. |

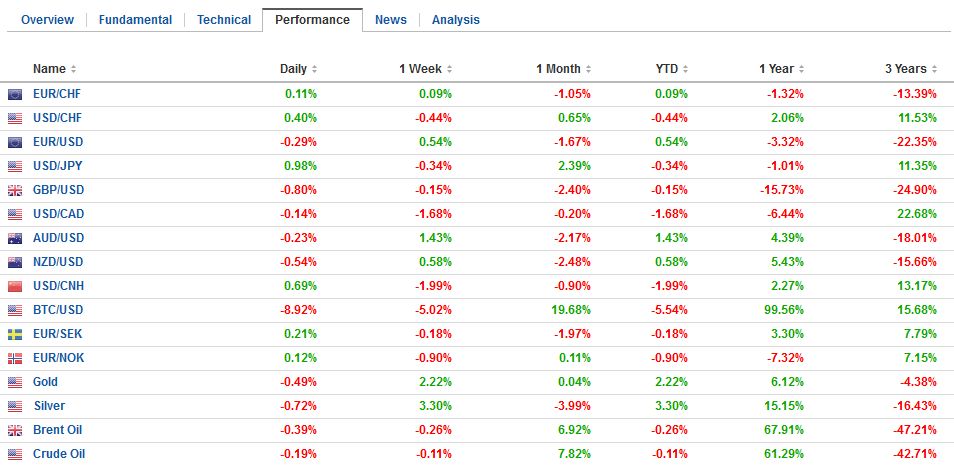

FX Performance, January 06 - Click to enlarge |

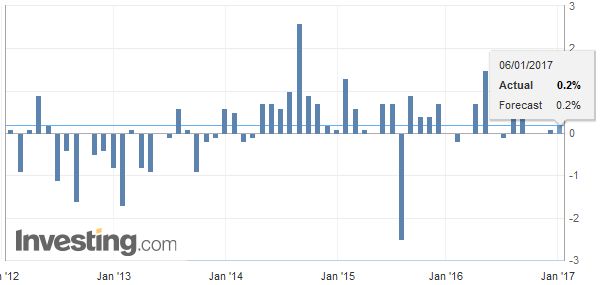

JapanThere are a few economic reports released today to note. The first was Japan’s real cash earnings. In November, they were 0.2% lower on a year-over-year basis. This is a poor reading. It is is the first negative reading for 2016. The central bank is pushing for inflation, but without employers raising wages to compensate this is the result. It could impact consumption and/or see a draw down in savings. |

Japan Average Cash Earnings YoY, December 2016(see more posts on Japan Average Cash Earnings, ) Source: Investing.com - Click to enlarge |

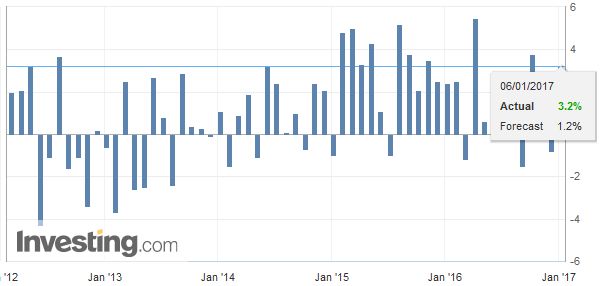

GermanyGermany reported disappointing November retail sales and factory orders. The 1.8% decline in November retail sales was twice the decline the Bloomberg median forecast. It gives back more of the 2.5% rise in October than expected. Still, the 3.2% year-over-year pace is respectable. |

Germany Retail Sales YoY, December 2016(see more posts on Germany Retail Sales, ) Source: Investing.com - Click to enlarge |

| Factory orders fell 2.5% in November, which is a little more than expected and follows a 5% rise in October. Germany reports industrial output figures next week, today’s data suggests small risks to the downside. |

Germany Factory Orders YoY, December 2016(see more posts on Germany Factory Orders, ) Source: zerohedge.com - Click to enlarge |

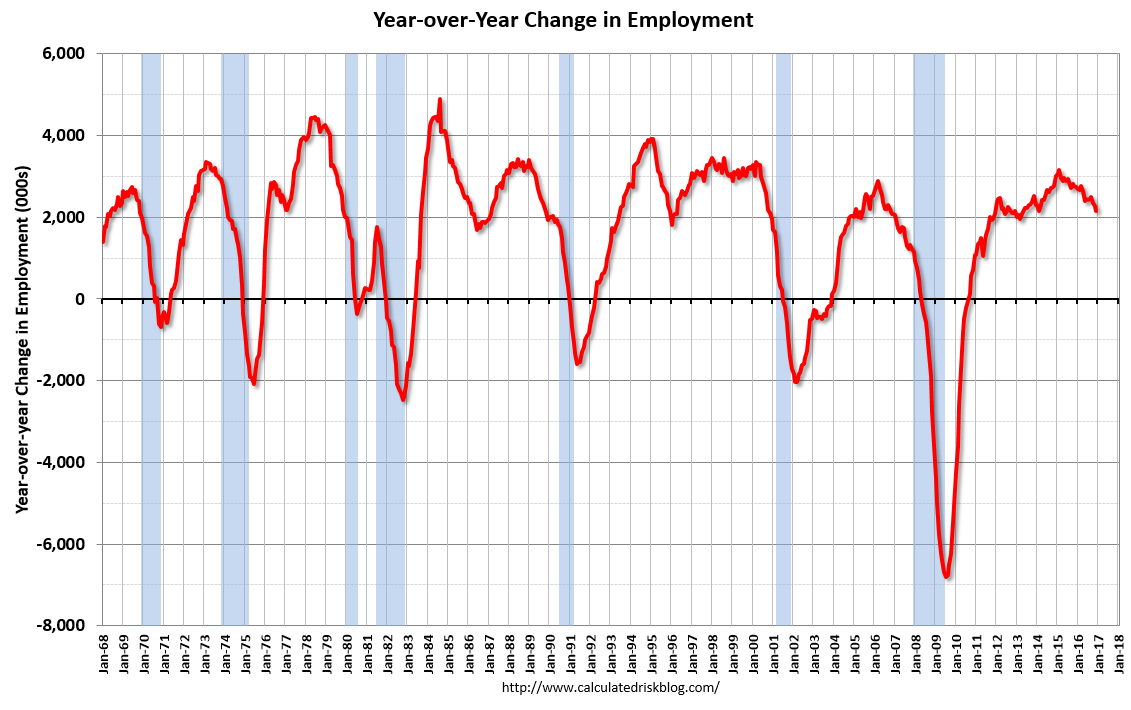

United StatesThe US and Canada report December jobs data and November trade figures. The main focus is on the US employment. |

U.S. Employment Change, December 2016(see more posts on U.S. Employment Change, ) Source: macro.economicblogs.org - Click to enlarge |

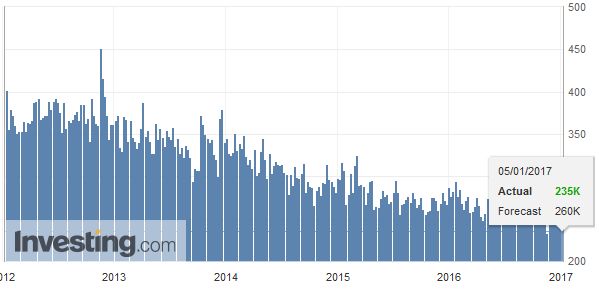

| The decline in jobless claims reported yesterday were likely skewed by the holiday and are well past the survey week for the non-farm payroll. |

U.S. Initial Jobless Claims, December 2016(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

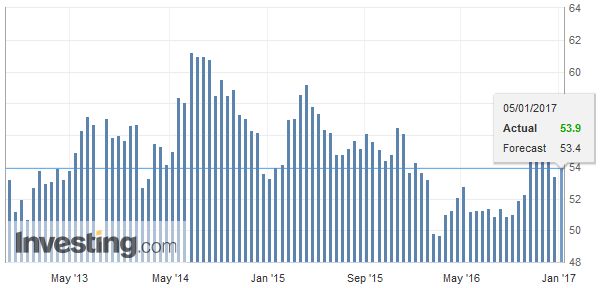

| We see downside risks, especially following the ADP, service ISM, Challenger figures and the trend in jobless claims. |

U.S. Services PMI, December 2016(see more posts on U.S. Services PMI, ) Source: Investing.com - Click to enlarge |

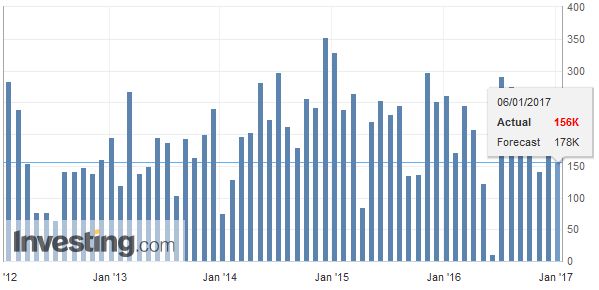

| A disappointing headline non-farm payroll figure and a tick up in the unemployment rate that many expect could be blunted by a stronger than expected rise in hourly earnings. |

U.S. Nonfarm Payrolls, December 2016(see more posts on U.S. Nonfarm Payrolls, ) Source: Investing.com - Click to enlarge |

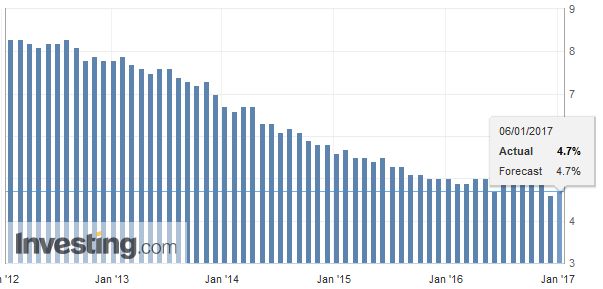

| Although it may be choppy, we see the technical evidence aligned for additional corrective pressure on the dollar. |

U.S. Unemployment Rate, December 2016(see more posts on U.S. Unemployment Rate, ) Source: Investing.com - Click to enlarge |

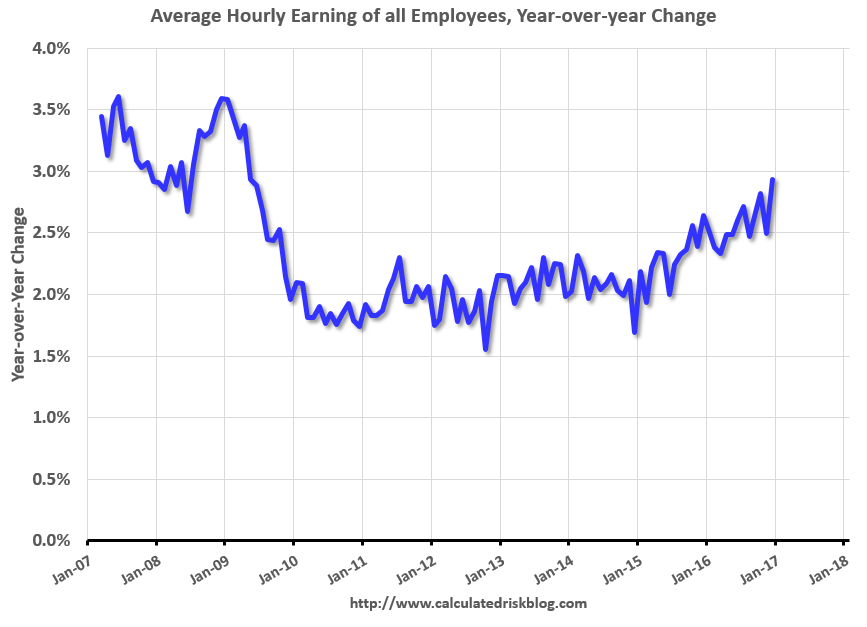

| Job growth has averaged 180,000 per month this year. In December, the year-over-year change was 2.16 million jobs. A key positive was the increase in hourly earnings. This is a noisy series, and the trend is clearly up. |

U.S. Average Hourly Earnings, December 2016(see more posts on U.S. Average Earnings, ) Source: macro.economicblogs.org - Click to enlarge |

Mexico

Mexico’s central bank is believed to have intervened in the Asian session for the first time. This is helping the peso stabilize now. Still, its 0.4% gain against the dollar (~MXN21.33), only manages to pare this week’s loss to 2.9%. The major trigger this week has been tweeted by the US President-elect objecting to investment in Mexico by the auto industry. Since NAFTA and the loss Canada’s preferential treatment, as well as Mexico’s trade agreement with the EU, auto production is organized on a continental basis and Mexico now accounts for roughly 40% of the auto jobs in North America.

Last February, when Mexico last intervened, the central bank also raised interest rates 50 bp between meetings. Energy tax increases went into effect at the start of the year. This coupled with the drop in the peso will likely boost price pressures. The risk of a rate hike before the February 9 meeting rises if the intervention.

Next week Mexico reports December CPI. The year-over-year rate is expected to rise to 3.4% (from 3.3%). It would be the highest since late-2014. However, raising rates to defend a currency is a limited strategy especially when the domestic economy is already struggling. Next week, Mexico also reports December industrial production. It was off.14% in year-over-year in November. Another course open to it is to change the intervention tactics and take a page from Brazil’s playbook and use swaps, which do not have a direct claim on reserves.

China

China does not have the same limitation in this regard as Mexico. It is not that its reserves are a multiple of Mexico’s. Instead, it is that Chinese can squeeze offshore yuan deposit rates sharply higher, to instill in speculators that the yuan is not a one-way market while having little impact on the onshore interest rates. In any event, after the biggest two-day rally on record, the offshore yuan (CNH) fell 0.7% today, and the onshore yuan (CNY) slipped 0.6%. On the week, CNH is up 2%, while CNY is up a little less than 0.4%. Yesterday’s gap created by the sharply lower dollar opening has been filled.

Chinese shares are eased to pare this week’s gains; the Shanghai Composite gained almost 1.9%. Most Asian equity markets, save China, Japan and India posted small gains, but the MSCI Asia Pacific Index lost 0.2% after a two-day 3% rally. European shares are also seeing this week’s gains pared. The Dow Jones Stoxx 600 is off 0.25% near midday in London. Some markets are closed or thinly traded due to the holiday. Most sectors are seeing profit-taking, though the real estate sector is bucking the trend.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,EUR/CHF,gbp-chf,Germany Factory Orders,Germany Retail Sales,Japan Average Cash Earnings,MXN,newslettersent,U.S. Average Earnings,U.S. Employment Change,U.S. Initial Jobless Claims,U.S. Nonfarm Payrolls,U.S. Services PMI,U.S. Unemployment Rate