Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

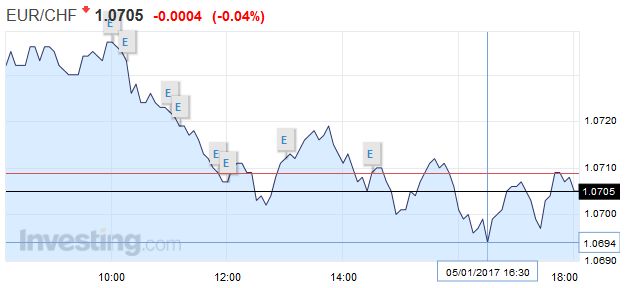

EUR/CHF - Euro Swiss Franc, January 05(see more posts on EUR/CHF, ) - Click to enlarge |

|

The Swiss Franc has limited data releases to note for the upcoming weeks therefore I expect news from the Brexit story and UK economic data to influence exchange rates this month. At present we are awaiting the decision from the Supreme Court in regards to if UK Prime Minister Theresa May needs to seek Government approval before triggering Article50 or if she has the power to invoke the article on her own. The consensus on the market is for a sharp fall if Theresa May manages to get the High Court decision overruled, where as if she loses the case I expect the pound to remain buoyant or potentially make gains against the Swiss Franc. If I had to make a prediction I believe there is a good chance the Supreme Court will rule in favour of the High Court as I wouldn’t be surprised to see the judges stick together. If my predictions come true, the pound could make gains against the Swiss Franc. However the gains should be short lived as Theresa May’s ‘Brexit’ deadline is March. |

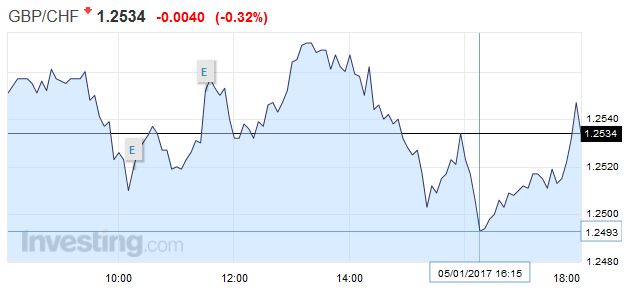

GBP/CHF - British Pound Swiss Franc, January 05(see more posts on GBP/CHF, ) - Click to enlarge |

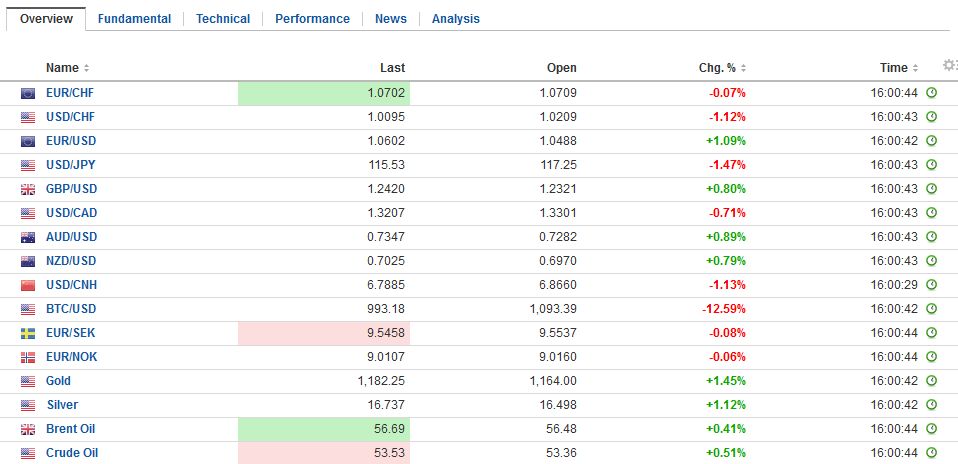

FX RatesThere are two main developments. First, the high degree of uncertainty expressed in the FOMC minutes and the repeated references to the strong dollar spurred a wave of dollar selling. The dollar retreated in Asia, but European participants saw the pullback as a new buying opportunity. The key takeaway from the FOMC minutes is that there is much uncertainty surrounding the size, timing, and composition of the new administration’s fiscal efforts. This told investors that officials are not particularly confident in their forecasts and projections, which Yellen had admitted at the post-FOMC press conference that the steeper rate path reflected very modest adjustments to a few changed forecasts among the participants. |

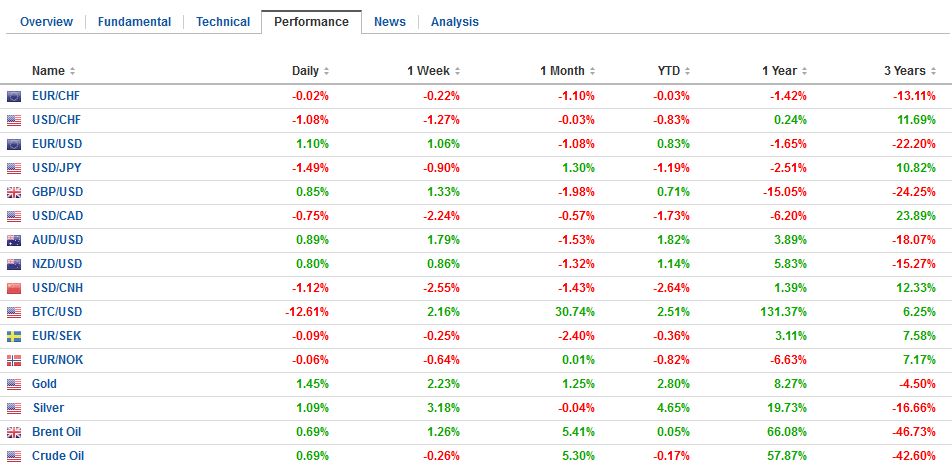

FX Performance, January 05 2017 Movers and Shakers Source: Dukascopy - Click to enlarge |

| The euro reached $1.0575 in Asia, 2.3 cents above Tuesday’s low. However, the upticks were sold into, and the euro was pushed back to $1.05. The key issue for participants today is whether the dollar’s downside correction is over. The lack of full participation and tomorrow’s US jobs report are also factors. On balance, we suspect the euro will find better support in the $1.0450-$1.0470 area. |

FX Daily Rates, January 05 - Click to enlarge |

| The yen is the strongest of the majors, but it too has seen its earlier gains pared considerably. The dollar peaked on Tuesday near JPY118.60. In Asia, it traded briefly through JPY115.60, the lowest since the Fed’s rate decision in the middle of last month. However, the dollar’s resilience is again evident. Europe took the dollar back toward JPY116.70. The JPY117.00-JPY117.50 may be difficult to overcome.

Sterling, which had bottomed near $1.22 on Tuesday reached through $1.2360 today, from where it was sold down to $1.2270 before finding buyers in Europe. The intraday technicals warn that the low may not be in place today. The Australian dollar has unwound its gains that had carried it to $0.7330. Support is seen in near $0.7270 and then $0.7240. The US dollar fell to CAD1.3255 bounced back to CAD1.3310. Gains above CAD1.3350 are needed to lift the tone. |

FX Performance, January 05 - Click to enlarge |

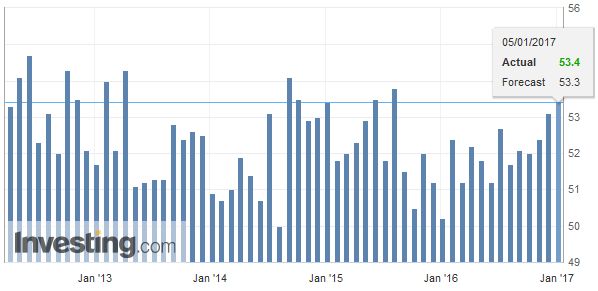

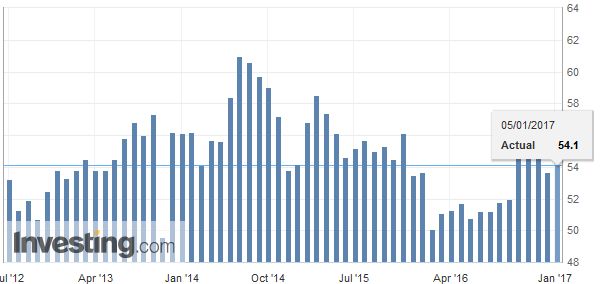

ChinaSecond, Chinese officials have continued to squeeze liquidity in the offshore yuan market (CNH), and some reports suggest that state-owned enterprises were encouraged to sell foreign exchange holdings. In addition to more formal and informal capital controls, Chinese officials triggered a short squeeze that has been painful enough to likely deter aggressive sales in the near-term. In these two days, as the overnight deposit rate for yuan in Hong Kong rose to 80% and the three-month deposit rate jumped 100 bp, the CNH has rallied nearly 1.9% and on the onshore yuan (CNY) has gained 1.1%. Longer-term outlooks will not change due to the short squeeze. More powerful fundamental drivers include the broader trajectory of the dollar and interest rate differentials. Still, capital controls and the willingness of officials to facilitate such a powerful squeeze demonstrates their resolve and ability to manage the challenges. Separately, there was more confirmation of the stabilization of the Chinese economy. The Caixin services PMI rose to 53.4 from 53. |

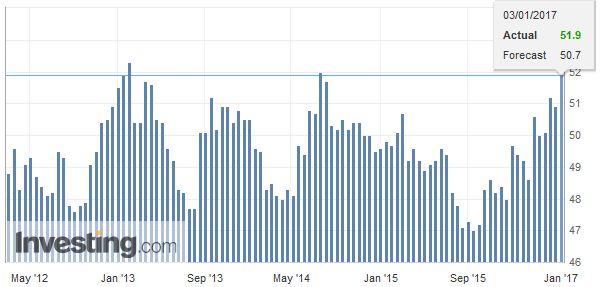

China Caixin Manufacturing PMI, December 2016(see more posts on China Caixin Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

| This combined with the improvement reported earlier in the manufacturing PMI, the composite rose to 53.5 (from 52.9), which is a new record for the two-year-old time series. |

China Caixin Services PMI, December 2016(see more posts on China Caixin Services PMI, ) Source: Investing.com - Click to enlarge |

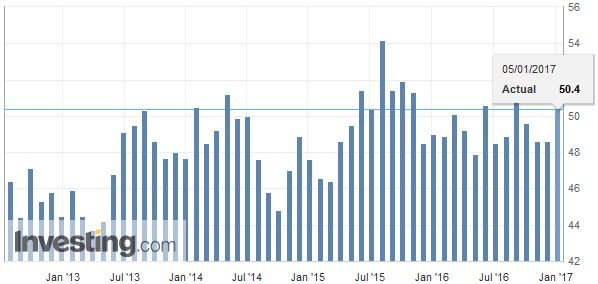

EurozoneWe also note that the German construction PMI reached a nine-month high in December, while the eurozone retail PMI bounced to 50.4 from 48.6. The eurozone growth appears to be broadly stable, and prices are firming. Even the core rate ticked up to 0.9%, while most economists had expected it to remain at 0.8%. Many expect price pressures to remain low in Europe due to the still large output gaps. A caution, however, comes from what appears to be a loosening link between factor usage, such as near full employment (in Germany, UK, Japan, and the US) and yet lower inflation than expected. |

Eurozone Retail PMI, December 2016(see more posts on Eurozone Retail PMI, ) Source: Investing.com - Click to enlarge |

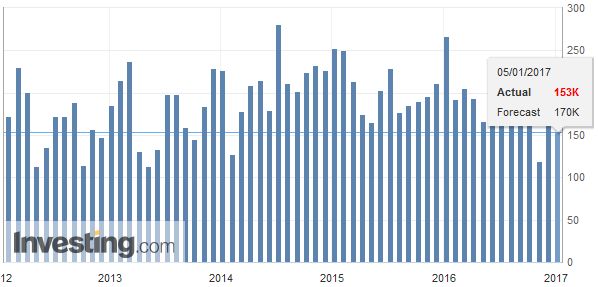

United StatesToday’s data highlight from the US will be the ADP private sector employment estimate. The Bloomberg median is for 175k after 216k in November. It will overshadow the weekly jobless claims, especially with the monthly jobs report tomorrow. Markit and ISM report December non-manufacturing PMIs. There may be some headline risk, but the focus is on the labor market. The employment sub-index will likely draw the attention. |

U.S. ADP Nonfarm Employment Change, December 2016(see more posts on U.S. ADP Nonfarm Employment Change, ) Source: Investing.com - Click to enlarge |

| The US 10-year yields that reached almost 2.52% on Tuesday (2.57% on December 28) fell to 2.43% yesterday and follow through buying pushed the yield briefly below 2.40% for the first time in nearly a month. The two-year yield approached 1.295 last week and fell to 1.19% at the end of last week. It has held that level today. |

U.S. Markit Composite PMI, December 2016(see more posts on U.S. Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

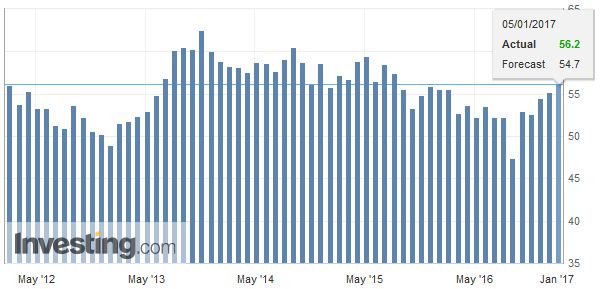

United KingdomThe rally in the US bond market carried over into Asia, but Europe is resisting. Peripheral yields are 2-3 bp higher while core yields are little changed. UK Gilts are under performing after a strong service PMI. It rose to 56.2 from 55.2. Many economists had expected a decline. With the three PMI readings in tow, the composite rose to 56.7, the highest level since mid-2015. The average in Q4 16 was 55.6 compared with 51.6 in Q3 and 52.5 in Q2. |

U.K. Services PMI, December 2016(see more posts on U.K. Services PMI, ) Source: Investing.com - Click to enlarge |

Switzerland |

Switzerland Consumer Price Index (CPI) YoY, December 2016(see more posts on Switzerland Consumer Price Index, ) Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,China Caixin Manufacturing PMI,China Caixin Services PMI,EUR/CHF,Eurozone Retail PMI,FX Daily,gbp-chf,newslettersent,Switzerland Consumer Price Index,U.K. Services PMI,U.S. ADP Employment Change,U.S. ADP Nonfarm Employment Change,U.S. Markit Composite PMI