Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

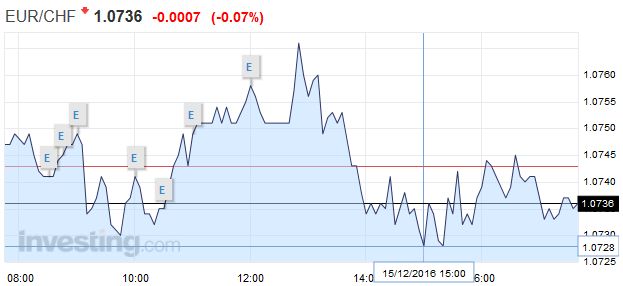

EUR/CHF - Euro Swiss Franc, December 15(see more posts on EUR/CHF, ) - Click to enlarge |

|

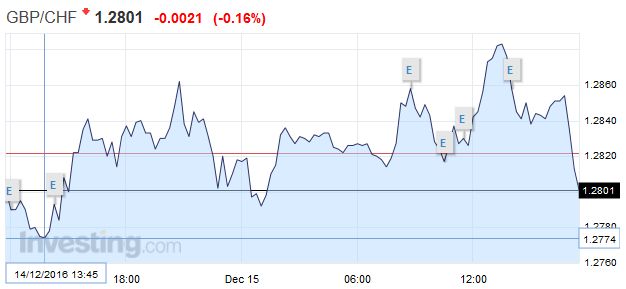

Sterling has made steady gains against the CHF over the past month and although the spike has levelled this week, the Pound has certainly gained a foothold. Yesterday’s decision by the US Federal Reserve to raise their base rate from 0.25% to 0.5% did little to shift the value of GBP/CHF but with investors still digesting the outcome, we may yet find it still has an effect. The FED’s decision to hike rates could be seen as a positive for the global economy, due to the US’s standing as the world’s economic powerhouse and this could bring some risk appetite back to investors. This in turn could lead to money being moved away from the safe haven currencies such as the CHF and in turn we could see further weakness and a move up towards 1.30 is certainly a possibility. However, I still feel that the Pound will find resistance around 1.30 and we may well need to see another shift in market conditions in order to break through this level. We also need to consider the on-going uncertainty surrounding the UK’s Brexit and the negative effect this is having on future growth forecasts. With further reports today that any trade deals post Brexit could take up to 10 years to negotiate, I would not be taking too many risks if I was holding Sterling and look to take advantage of the recent upturn. If you have an upcoming GBP or CHF currency exchange to make and you are concerned by the increased market volatility of late, it may be wise to look at protecting the gains you’ve made, or limiting your losses with one of our forward contracts, rather than gamble on what has become an increasingly volatile and unpredictable market. |

GBP/CHF - British Pound Swiss Franc, December 15(see more posts on GBP/CHF, ) - Click to enlarge |

Federal ReserveThe Federal Reserve delivered the widely expected hike yesterday. A year ago it suggested four hikes in 2016 were likely appropriate. The market never accepted that, and as the year progressed many derided it. Yesterday the Federal Reserve’s projections anticipated three hikes next year instead of the two anticipated in September. The distribution of the forecasts illustrates what happened. In September, seven of the 17 members expected Fed funds would finish 2017 in the 1.25%-1.50% or higher. Yesterday 11did. In September, 10 expected that Fed funds would finish 2017 1.0%-1.25% of lower. Now six do. |

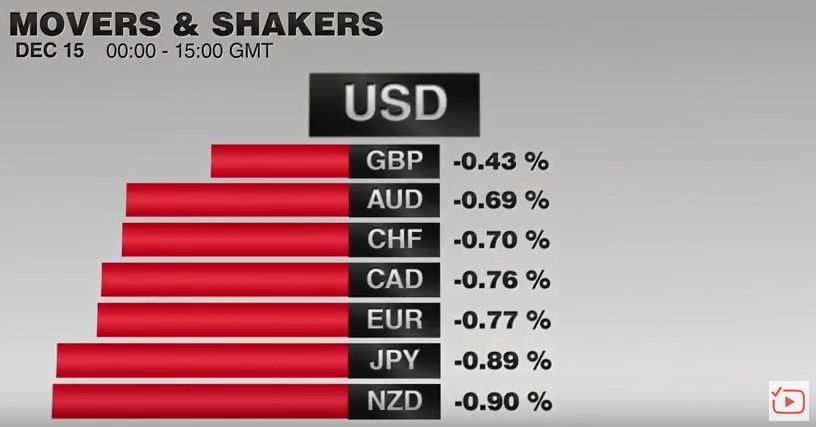

FX Performance, December 15 2016 Movers and Shakers Source: Dukascopy - Click to enlarge |

| Yellen made two important points that ought not to be lost. First, she noted that the change in the median forecast was small and was the result of a few members changing their forecasts. Second, and arguably more important, some but not all the participants incorporated changes in fiscal policy. This gives meaning to the old saw about a camel being a horse made in committee. We did not anticipate a change in forecasts based on fiscal policy that is impossible to make any judgments. It is not just about size, but they simply contribute the disparity of income and wealth or do they lift the growth potential.

What changed in the market’s reaction function is that the rise in US rates was an adjustment in the real rate. That is to say that it appears that inflation expectations did not change. Here we measure inflation expectations by the 10-year breakeven rate (inflation-linked bond yield and the conventional bond yield). For example, the 10-year US yield is up 14 bp on the week. The 10-year break-even is down three basis points this week. |

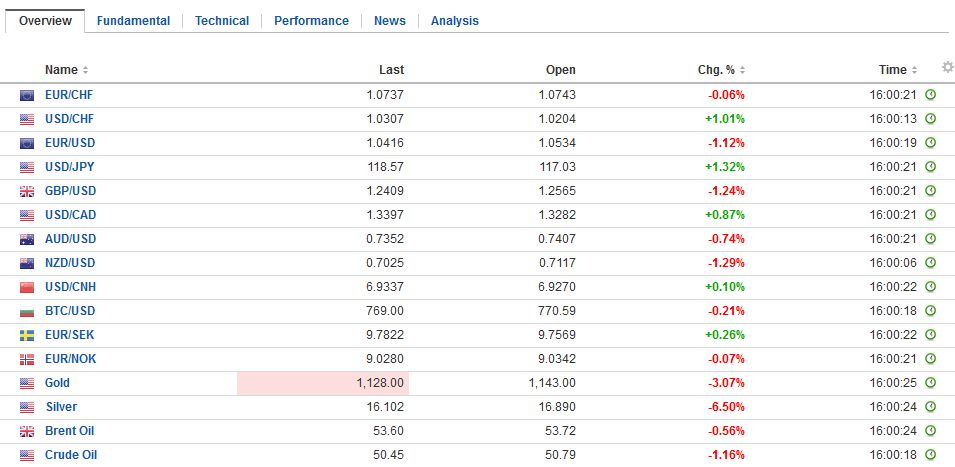

FX Daily Rates, December 15 - Click to enlarge |

| There are several other developments today, though the dollar’s rally and bond sell-off appear driven by the Fed. Equity markets are more mixed, with Asia following the US lower, and Europe is mostly moving higher.

First are the central banks. The Swiss National Bank kept policy steady and repeated its usual threat to intervene. It appears that it will accept some modest franc appreciation. Norway’s Norges Bank surprised many by leaving its rate path unchanged. Many had expected that although there would be no change in policy, the central bank would lower the rate path due to the krone’s strength. However, officials seemed more concerned about financial excesses and real estate prices. The knone is the only major currency not to have fallen against the dollar today. The Bank of England is ahead. No change is expected in the neutral bias. Of note sterling and interest rates are higher than when the MPC last met. |

FX Performance, December 15 - Click to enlarge |

AustraliaSecond are the economic reports. There are three to note. Australian reported stronger than expected labor data, even though the unemployment rate rose to 5.75 from 5.6%. |

Australia Unemployment Rate, November 2016(see more posts on Australia Unemployment Rate, ) Source: Investing.com - Click to enlarge |

| The participation rate rose more (64.6% from 64.4%(. The 39.1k net new jobs created were all full-time positions, and the October series was revised higher. The Australian dollar is faring second best among the majors today, off 0.2% as it dips below $0.7400. Initial support is pegged near $0.7370. |

Australia Participation Rate, November 2016(see more posts on Australia Participation Rate, ) Source: Investing.com - Click to enlarge |

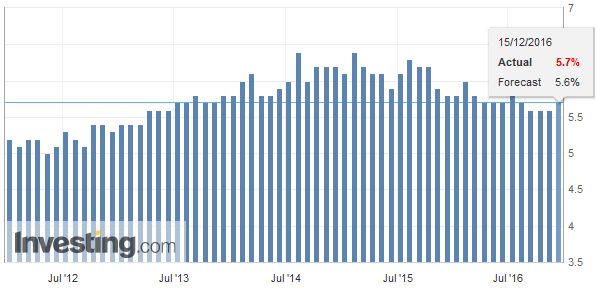

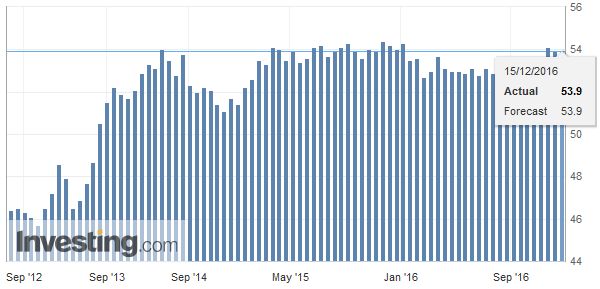

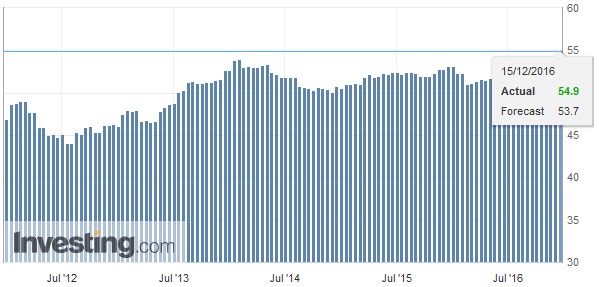

EurozoneThe flash eurozone PMI composite was, as expected, unchanged at 53.9. The three-month average is 53.7, which is the highest since Q4 15. It suggests Q4 growth is firm around 0.4%.

|

Eurozone Markit Composite PMI, November 2016(see more posts on Eurozone Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

| The details are interesting. Manufacturing jumped to 54.9 from 53.7, but services unexpectedly fell to 53.1 from 53.8. This is clearly a function of something in Germany. France’s manufacturing and service reading were both above expectations, finishing a difficult year on a firm note. |

Eurozone Manufacturing PMI, November 2016(see more posts on Eurozone Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

Elsewhere, we note that the details of the TLTRO will be released. The average take-down of the first two was about 32.5 bln euros. The amount is seen as generally disappointing. The Greek government claim to use its overshoot on the primary budget surplus target to make an extra pension payment and ease the sales tax in the islands hit by the refugee crisis brought a strong rebuke from the ESM. This pressured Greek assets. Today’s reports suggested that France was breaking from the ESM to side with Greece.

The euro has fallen two cents from yesterday’s high. Last year’s low was set in late-March just below $1.0460, the lowest since 2003. There is little on the charts until closer to $1.0075 and then the psychologically important $1.00. A move now back above $1.0550 would likely signal a consolidative phase. The US two-year premium over German has jumped to 2.05%. Many will only see the Fed’s hand in this, but look closer, and you’ll see that the German two-year yield fell to new record lows near minus 80 bp. The adjustments to the securities lending program by the ECB and Bundesbank have not been sufficient to ease the pressure in the repo market. Year-end considerations exacerbate this pressure.

Rising US yields are lifting the greenback against the yen. It has approached JPY118.50, the highest since last February. It dipped briefly below JPY114.80 yesterday. There is little chart resistance until the JPY120 area. Europe has extended Asia’s advance. In the two weeks through last Friday, foreign investors bought about JPY680 bln of Japanese equities and JPY1.39 trillion of Japanese bonds. Much of the equities are likely on a currency-hedged basis. The bonds may be financed in the cross-currency swap market rather than in the spot market.

Full story here Are you the author?

Tags: #GBP,#USD,$AUD,$EUR,Australia Participation Rate,Australia Unemployment Rate,EUR/CHF,Eurozone Manufacturing PMI,Eurozone Markit Composite PMI,Federal Reserve,gbp-chf,newslettersent,Norwegian Krone