Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

EUR/CHF - Euro Swiss Franc, December 07(see more posts on EUR/CHF, ) Source: Investing.com - Click to enlarge |

|

The pound has seen a very marked turnaround against the Swiss Franc with almost 8 cents gained in the last few weeks. GBP/CHF appears to have 1.30 in its sights and at this pace it should be there in record time. This week sees a number of political events which are playing out into the currency markets. The Italian referendum whereby Matteo Renzi has agreed to resign is a trigger for volatility in the Eurozone and has already seen the Euro weaken. With growing political unhappiness in the EU we are likely to see added pressure on the Euro. This anti-establishment is actually proving good for sterling exchange rates as these growing problems mean that Britain would appear to be less isolated than it was 4 months ago. As such this in my view is one of the main drivers for sterling exchange rates across the board as it means that the outlook for Britain post Brexit is looking less gloomy, in my view anyway. The UK Supreme Court hearing on Parliament Brexit appeal continues to be heard this week and there are likely to be market reactions considering the case is being shown live. Although a verdict is not expected until January we could still see an outcome in December. Should Theresa May win the case and I believe there is a growing chance that she will then the pound could slide lower as a hard Brexit will become the order of the day once again. Clients who are holding sterling are seeing a very volatile period at the moment which is unlikely to change any time soon although sterling still appears to be on the up. |

GBP/CHF - British Pound Swiss Franc, December 07(see more posts on GBP/CHF, ) Source: Investing.com - Click to enlarge |

FX RatesThe US dollar is little changed against most of the major currencies. Sterling is the notable exception, losing about 0.75% to trade at three-day lows. It was on the defensive in early European turnover but got the run pulled from beneath by the unexpectedly poor data. |

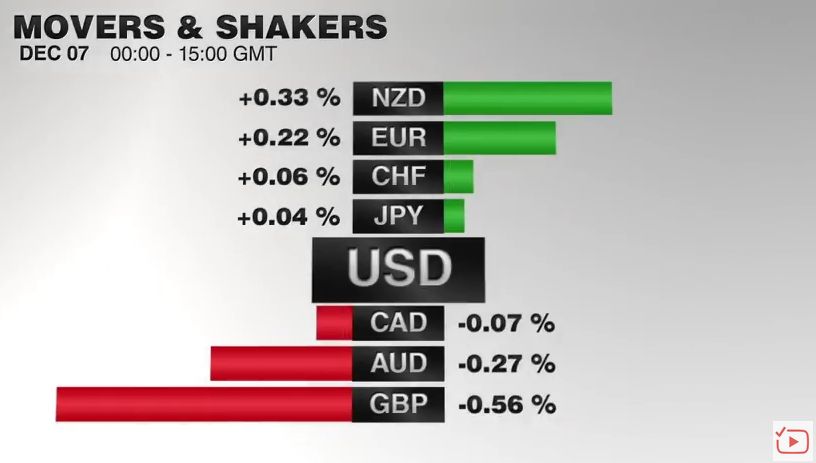

FX Performance, December 07 2016 Movers and Shakers Source: Dukascopy.com - Click to enlarge |

| Sterling was near two-months highs yesterday, reaching $1.2775. It was sold off to almost $1.2580 today. It appears to found a bid, but it may be difficult to resurface above $1.2650. The euro had begun the week at nearly four-month lows against sterling just ahead of GBP0.8300. It traded a little above GBP0.8520 today but is running into offers as the 20-day moving average is approached (~GBP0.8530). The euro has not traded above this moving average since the US election. |

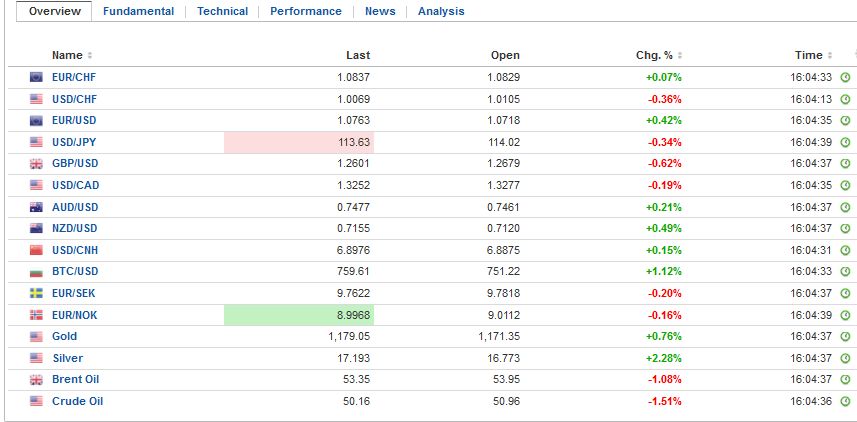

FX Daily Rates, December 07 - Click to enlarge |

| The euro has been trapped in about a quarter of a cent range through most of the European morning. Since stalling near $1.08 at the start of the week, the euro approached $1.07 yesterday. The ECB meets tomorrow and is expected to extend its asset purchase program, adjust some self-imposed rules to minimize the scarcity challenge, and ease the securities lending facility to alleviate some pressure in the repo market. |

FX Performance, December 07 - Click to enlarge |

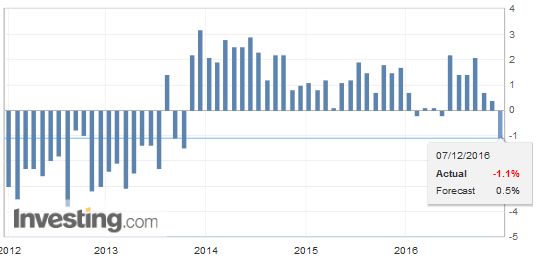

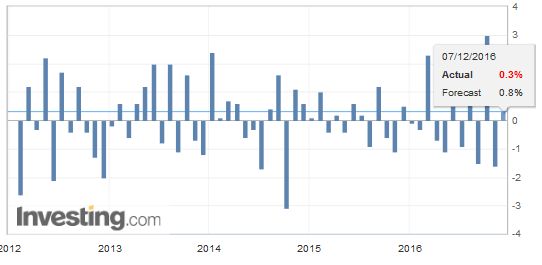

United KingdomUK industrial output fell by 1.3% in October. The median forecast was for a small increase. |

U.K. Industrial Production YoY, October 2016(see more posts on U.K. Industrial Production, ) Source: Investing.com - Click to enlarge |

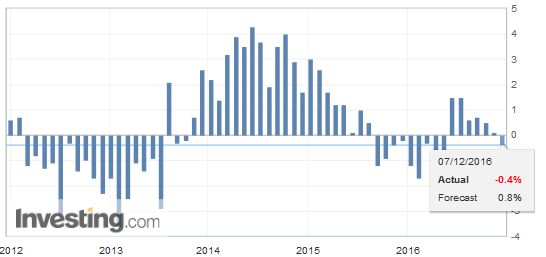

| While oil and gas took a toll, as one of the large North Sea fields was closed for maintenance, manufacturing output slumped by 0.9%. A small gain was expected. The decline was sufficient to push the year-over-year rate into contraction (-0.4%) for the first time since March. Last week’s PMI warned of further slowing in manufacturing in November. |

U.K Manufacturing Production YoY, November 2016(see more posts on U.K. Manufacturing Production, ) Source: Investing.com - Click to enlarge |

GermanyGerman industrial output also disappointed today. The 0.3% increase in October was a little more than a third of what was expected. The September series was revised to show a 1.6% decline rather than a 1.8% fall. The Bundesbank expects growth to accelerate here in Q4, and the PMI supports the optimistic assessment. |

Germany Industrial Production MoM, October 2016(see more posts on Germany Industrial Production, ) Source: Investing.com - Click to enlarge |

Australia

Australia disappointed the market today too. The economy contracted by 0.5% in Q3. The median called for a 0.1% contraction. It is the first contraction since 2011 and the largest since 2008. The Australian dollar had been turned back from $0.7500 at the start of the week. That area capped the Australian dollar last week as well. It fell a little below $0.7420 today on the news. It held above Monday’s low by a couple of ticks and recovered to almost $0.7460 in the European morning.

Italy

Looking at Italian markets, one would hardly know the extent of the political and economic challenges. Italian bank share is up 2.7% on top of yesterday’s nearly 9% advance. Local papers claiming the government is considering drawing on an ESM facility has been denied. Meanwhile, there are other reports suggesting the government could buy as much as two bln euros of subordinated debt owned by retail investors in Monte Paschi, and then swap those bonds for equity.

On the political front, the idea of a February election seems like a stretch. Here is the problem in a nutshell. The old electoral law was ruled unconstitutional. The new law that applies only to the lower chamber is under judicial review, and a hearing is not planned until next month. With the broad defeat of the referendum, there is a new electoral law for the upper chamber. It is possible that Renzi does not just stay on for the passage of the 2017 budget, but until the electoral reform can be implemented to prepare for elections.

There is the usual fear-mongering. The defeat of the referendum, some argue, means that the Five Star Movement is likely to head up the next government and quickly seek a referendum on EMU membership. However, there is still good reason to suspect while this is possible, there are more likely scenarios. Consider that 40% voted in favor of the referendum. That was not enough to win the referendum, but it is enough to win a general election in Italy given the fragmentation of the electorate.

The referendum got all of the government’s critics, some within the PD itself, on the same side of the issue. An election is different. Moreover, the electoral reform that the court is reviewing gives the largest voting-getting party bonus seats. This seems to be the only way the 5-Star Movement could secure a majority, as it is weak in finding coalition partners. This component may be struck down and instead, proportional representation re-introduced.

China

The dollar value of China’s reserves fell by a little more than $69 bln in November. It was the fifth consecutive monthly fall. China’s reserves finished last year near $3.33 bln. As of the end of last month, they stood at $3.051 bln. Part of the decline in reserves, of course, reflects valuation swings. The reserves are kept primarily in fixed income, and November saw a sharp sell-off in global bonds. Also, the dollar appreciated sharply, which reduces the dollar value of the component of reserves invested in euro (-3.6% in November) and yen (-8.4% in November).

To be sure, there were genuine capital outflows as well. On the one hand, China appears to be introducing new capital controls to limit outflows. Foreign companies repatriating profits and proceeds of asset sales are being stymied, according to the front-page story in today’s Financial Times. On the other hand, many expect renewed capital outflows near a year when the $50k cap on individual capital exports is renewed.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?

Tags: #GBP,#USD,$AUD,$CNY,$EUR,EUR/CHF,gbp-chf,Germany Industrial Production,Italy,newslettersent,U.K. Industrial Production,U.K. Manufacturing Production