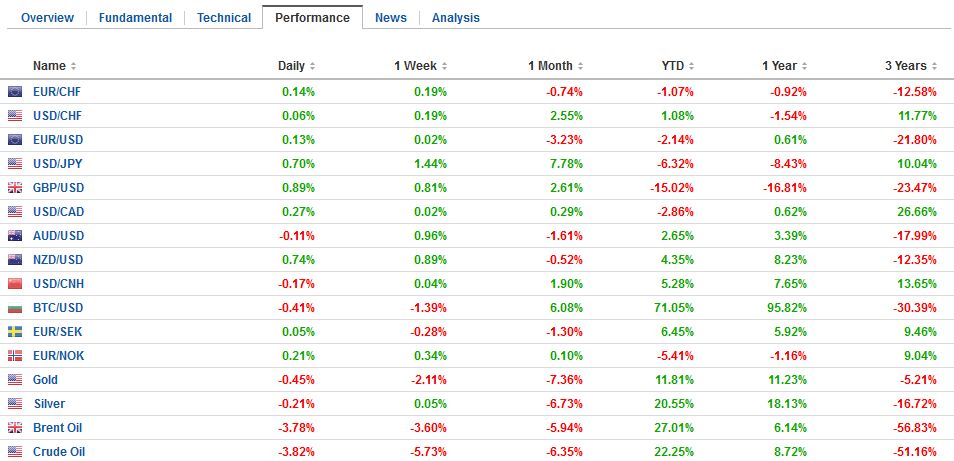

Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss Franc |

EUR/CHF - Euro Swiss Franc, November 29(see more posts on EUR/CHF, ) . - Click to enlarge |

FX RatesThe US dollar correctly lowered yesterday, but most of the selling was over by the end of the Asian session, and the greenback steadied in Europe and North America. The dollar is firm against the euro and yen but within yesterday’s broad trading ranges. The Australian and Canadian dollar’s gains from yesterday are being pared. What had looked like a possible deeper dollar correction is turning into a consolidative phase that may be sufficient to alleviate the over-extended technical condition. Equities are lower. Of note, the Topix 12-day advance was snapped with a minor loss of less than 0.1%. The MSCI Asia-Pacific Index is off 0.25% to snap a three-day advance. The Dow Jones Stoxx 600 is off fractionally to extend yesterday’s decline. The MSCI Emerging Market equity index is lower by 0.25%, after initially building on yesterday’s advance to reach a two-week high. The South African rand is the weakest of majors, while the Chinese yuan, which was fixed higher by the PBOC for the second session, is the strongest of the emerging market currencies, gaining almost 0.3%. European bonds firmer, led by a 6 bp decline in Italy’s 10-year yield. French bonds are also outperforming German bunds, narrowing the premium from a two-year peak. The US 10-year yield is firm near 2.33%. |

FX Performance, November 29 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

|

Sterling is an exception. It is firmer, following news that mortgage approvals rose more than expected in October to stand at the highest since March, while household credit increased GBP1.6 bln. The Bank of England noted that the effective interest rate on new mortgages fell 11 bp in October to 2.16%, the lowest since at least 2004. However, even with the upticks sterling has been confined to yesterday’s ranges.

The other development drawing attention today is in South Korea, where the beleaguered President Park Geun-hye has offered to resign apparently in an effort to derail impeachment efforts. Part of the constitutional challenge of the succession is that Park dismissed her prime minister and finance ministers earlier this month to stem the influence-peddling scandal. The prospect of a resolution helped steady the Korean won and local stocks. The Kospi posted the smallest of gains, while MSCI Asia-Pacific Index snapped a three-day advance. |

FX Daily Rates, November 29 (GMT 16:00) . - Click to enlarge |

| On the other hand, news that South African President Zuma managed to fend off critics within the executive committee of his own party who seek his resignation, coupled with some profit-taking in the metals has seen the rand give back yesterday’s gains in full. The rand is the weakest of the emerging market currencies, off a little more than 1.5%.

However, the markets’ focus is elsewhere. Investors are finding it difficult to get a read on OPEC. Although a deal may be elusive, as Russia now says it won’t attend the Wednesday meeting in Vienna, Iran and Saudi Arabia do not look that far apart. The latest reports suggest Saudi’s wanted it to freeze output at a little more than 3.7 mln barrels a day, and the Iranians wanted 3.975 mln. A compromise has been suggested at 3.795 mln barrels. Iran and Iraq are also disputing the methodology to determine how the cuts should be distributed. The front-month Brent contract is off 1.5% near $47.50, while the front-month light sweet contract is off a little more at $46.25.

|

FX Performance, November 29 . - Click to enlarge |

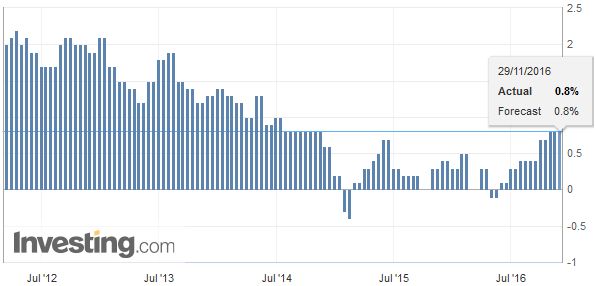

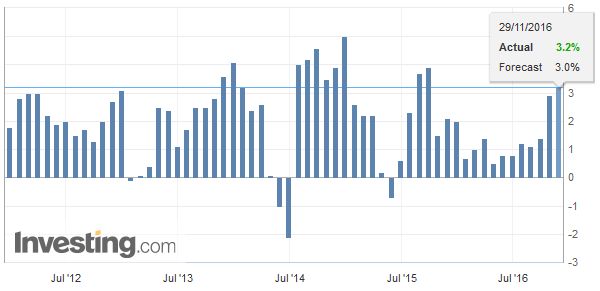

GermanyGerman states have reported preliminary November CPI figures, and national estimate will be reported shortly. The EU-harmonized measure is expected to rise 0.1% to lift the year-over-year rate to 0.8%. It would match the strongest pace since June 2014. It finished last year at 0.2%. France reported Q3 GDP rose 0.2%, in line with Q2. However, Q4 began on a firmer note, with October consumer spending jumping 0.9%, threefold more than the Bloomberg median, tainted a little by the downward revision to the September series to -0.4% from -0.2%. |

Germany Consumer Price Index (CPI) YoY, October 2016(see more posts on Germany Consumer Price Index, ) . Source: Investing.com - Click to enlarge |

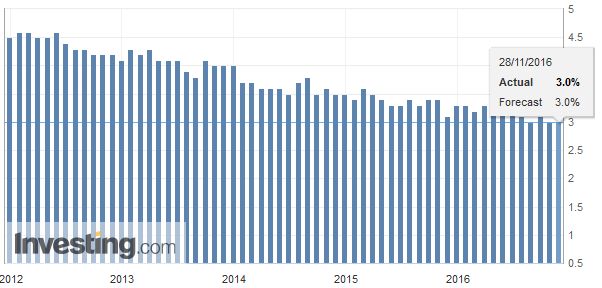

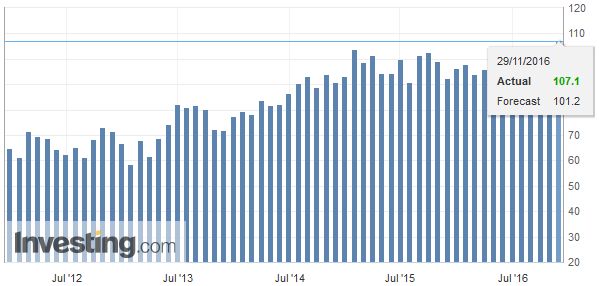

JapanJapan reported strong employment and consumption figures, suggest Q4 is also off to a firm start. Although the unemployment rate remained unchanged at 3.0%, the details were encouraging. The job-to-applicant ratio ticked up 1.40, which is a new high since 1991. The number of unemployed slipped below two million for the first time since February 1995. |

Japan Unemployment Rate, October 2016(see more posts on Japan Unemployment Rate, ) . Source: Investing.com - Click to enlarge |

| Separately, Japan reported that retail sales jumped 2.5% in October, which lifted the year-over-year rate from -1.9% in September to -0.1%. Overall household spending improved from -2.1% in September from a year ago to -0.4% in October. This matches the smallest contraction since April. |

Japan Retail Sales YoY, October 2016(see more posts on Japan Retail Sales, ) . Source: Investing.com - Click to enlarge |

Eurozone

|

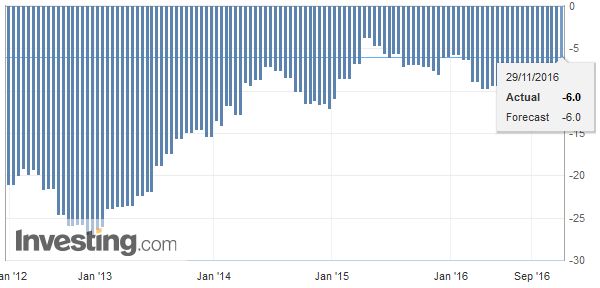

Eurozone Consumer Confidence, November 29 2016(see more posts on Eurozone Consumer Confidence, ) . Source: Investing.com - Click to enlarge |

United States

|

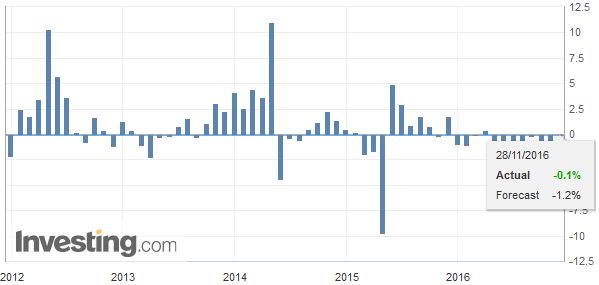

U.S. Gross Domestic Product (GDP) QoQ, October 2016(see more posts on U.S. Gross Domestic Product QoQ, ) . Source: Investing.com - Click to enlarge |

| S&P CoreLogic will report house prices, and the Conference Board’s measure of November consumer confidence is expected to jump from 98.6 in October back above 100. NY Fed President Dudley talks about the Puerto Rico economy early in the North American session, while Governor Powell speaks early afternoon. The ADP report, October consumption and income figures, and Chicago PMI will be released tomorrow, and the Beige Book will be released ahead of the mid-December FOMC meeting. |

U.S. CB Consumer Confidence, October 2016(see more posts on U.S. Consumer Confidence, ) . Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,EUR/CHF,Eurozone Consumer Confidence,Germany Consumer Price Index,Japan Retail Sales,Japan Unemployment Rate,newslettersent,South Korea,U.S. Consumer Confidence,U.S. Gross Domestic Product QoQ