Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss Franc |

EUR/CHF - Euro Swiss Franc, October 17 2016(see more posts on EUR/CHF, ) . - Click to enlarge |

FX RatesThe US dollar is consolidating in relatively narrow trading ranges. Participants appear to be waiting for fresh incentives, while the recent rise yields continue and equities have begun the new week on a soft note. Yellen spoke before the weekend, and her explicit willingness to tolerate higher inflation pushed yields higher, while not deterring expectations for a hike in December. Today, Fischer speaks in New York near midday, and investors may look for confirmation. |

FX Performance, October 17 2016 Movers and Shakers . - Click to enlarge |

| Canada reports international securities transactions, but the talking point today is about Belgium possibly blocking the EU free-trade agreement (Comprehensive Economic and Trade Agreement–CETA). It would be the first EU free-trade agreement with a G7 country. One part of Belgium, which is needed for the coalition government, wants to have more safeguards. Some worry that the length of time it has taken to negotiate this agreement (~7 years) and the difficulty does not bode well for the UK.

Lastly, we note that the US and UK are considering new sanctions on Russia for its actions in Syria and particularly the bombing for Aleppo. In Europe, France and Italy have been reluctant, but German says it is considering joining the US and the UK. Syria is becoming an increasingly important global flashpoint. China has sent military advisors and is sympathetic to the Russian and Syrian position. Turkey, which appears to be shunned, even if for good reasons from the EU, is having a rapprochement with Russia. There is an argument in the US press that Russia may be seeking advantage during this part of the US political cycle to put it in a better negotiating position with the next US Administration. While the US Treasury may have softened its criticism of China’s currency policy with its report at the end of last week, US-Russian tensions are rising.

|

FX Daily Rates, October 17 (GMT 15:00) . - Click to enlarge |

| Rightmove’s October house price index rose 0.9% from a 4.2% year-over-year increase. It arrests the decline in the year-over-year pace since the referendum. While sterling remains confined to last Tuesday’s trading range ($1.2090-$1.2375), UK assets remain under pressures. UK debt instruments are selling off. The 10-year yield is up nine bp today and briefly poked above 1.20% for the first time since the referendum. Recall that the yield finished last month near 67 bp.

The FTSE 250 is off 0.8%, with consumer sectors (staples and discretionary) the hardest hit. The precipitous drop in sterling is expected to squeeze real incomes and compress household demand. The FTSE 100 is flirting with its 20-day moving average (~6952) and has not closed below this moving average since mid-September. |

FX Performance, October 17 . - Click to enlarge |

Japan

The news stream is light with three economic reports of note. First, Japan revised lower its initial 1.5% estimate for industrial output in August. It now stands at 1.3%. The year-over-year rate was revised to 4.5% from 4.6%. The Topix rose 0.4%, led by real estate and materials. Telecoms and utilities were the only sectors unable to advance today. The dollar has been confined to about half a yen against the Japanese currency today, trading within the pre-weekend range. The intraday technicals warn the consolidation tone may persist through the North American session, and the dollar could pullback toward the JPY103.60-JPY103.80 area.

EurozoneSecond, the eurozone confirmed September’s CPI print of 0.4% year-over-year, with the core rate increasing by 0.8%. The euro was unaffected by the report. The single currency made a marginal new low a little below $1.0965 to reach an 11-week extreme. It found a bid by the middle of the Asian session that carried it back to $1.10 in the European morning. The trendline found by connecting the January, June and July lows that were violated last week, is found near $1.1040 today and will now likely act as resistance if the $1.10 is convincingly retaken. |

Eurozone Core Consumer Price Index (CPI) YoY, September 2016(see more posts on Eurozone Core Consumer Price Index, ) . Source: Investing.com - Click to enlarge |

| The Dow Jones Stoxx 600 is off 0.7%, paring the pre-weekend gains. Consumer staples and energy are the largest drags, though no sector is gaining today. Of note, Deutsche Bank shares, which have traded higher for three consecutive weeks has also begun the new week with small gains. Italy’s bank index is also slightly higher on the session. However, sovereign bond yields are rising. Ten-year benchmark yields are 2-4 bp higher in Europe, with Italy’s 5.5 bp increase the most in EMU. |

Eurozone Consumer Price Index (CPI) YoY, September 2016(see more posts on Eurozone Consumer Price Index, ) . Source: Investing.com - Click to enlarge |

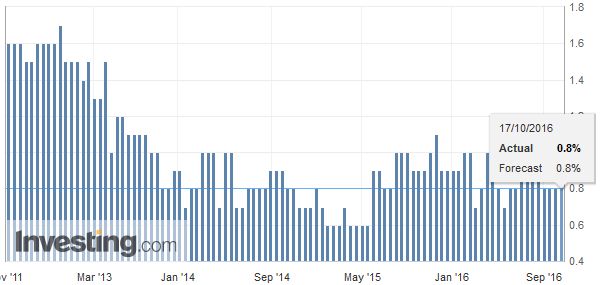

United StatesThe US reports the October Empire Manufacturing and the September industrial output figures. The inventory cycle has weighed on US manufacturing, and its recovery is slower than expected. Nevertheless, it does appear to be taking place, and it should be evident in the today’s report. |

U.S. NY Empire State Manufacturing Index, September 2016(see more posts on U.S. NY Empire State Manufacturing Index, ) . Source: Investing.com - Click to enlarge |

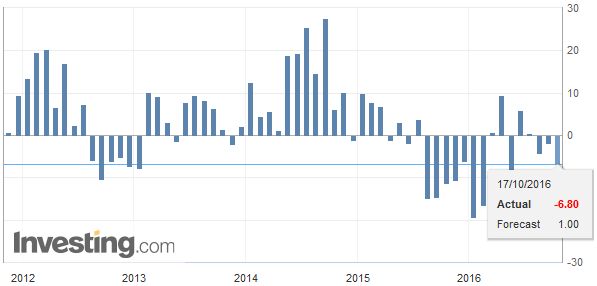

| Industrial output is expected to have increased 0.2% after a 0.4% fall in August. |

U.S. Industrial Production, September 2016(see more posts on U.S. Industrial Production (ZH), ) . Source: Calculatedriskblog.com - Click to enlarge |

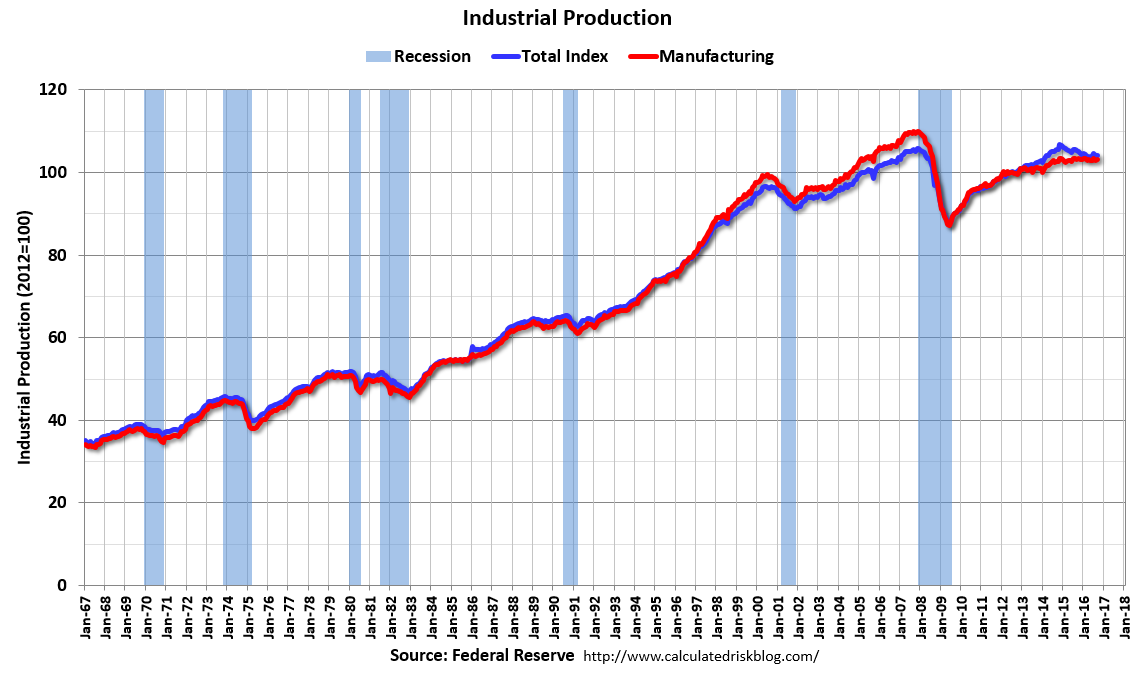

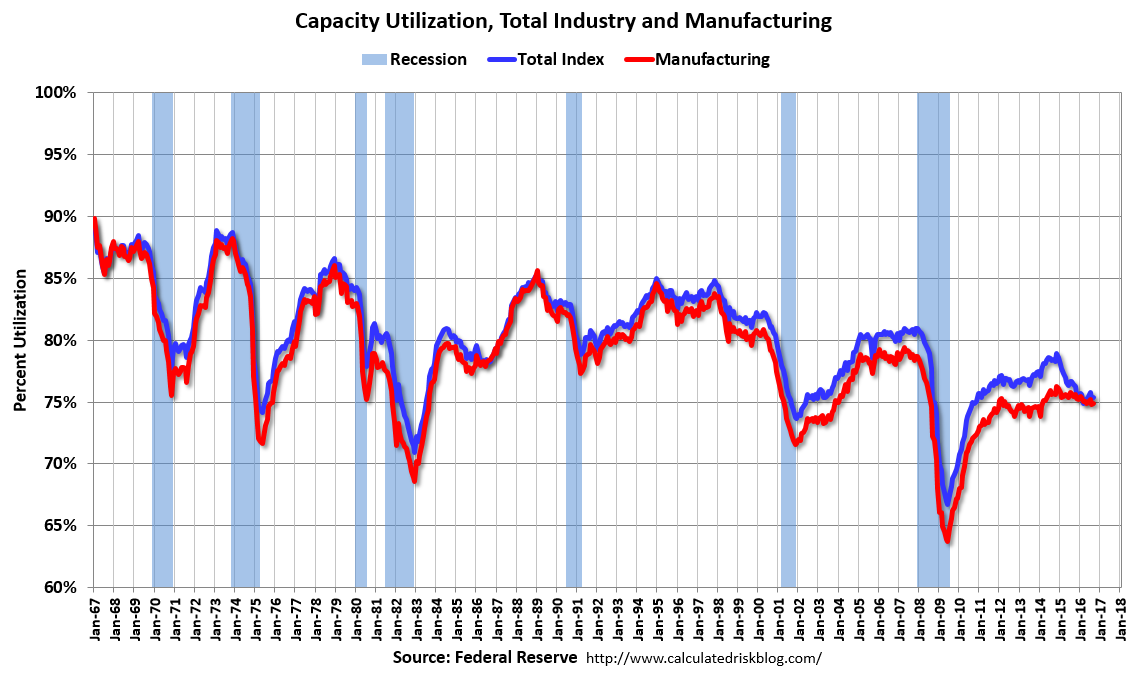

| Manufacturing itself may have risen 0.,1% after also recording a 0.4% decline in August. For the past three-quarters, and four of the past five, manufacturing output has averaged no growth. |

U.S. Capacity Utilization, Total Industry and Manufacturing, September 2016(see more posts on U.S. Capacity Utilization, ) . Source: Calculatedriskblog.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$EUR,$JPY,EUR/CHF,Eurozone Consumer Price Index,Eurozone Core Consumer Price Index,FX Daily,newslettersent,U.S. Capacity Utilization,U.S. Consumer Price Index,U.S. Core Consumer Price Index,U.S. Industrial Production (ZH),U.S. NY Empire State Manufacturing Index