Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

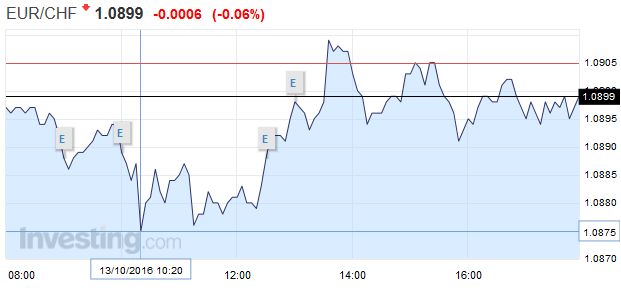

Swiss FrancThe EUR/CHF remains in the range of 1.0815 to 1.0980. The SNB usually intervenes below 1.0850. I am expecting that speculators are reducing their CHF short positions. More tomorrow. |

EUR/CHF - Euro Swiss Franc, October 13 2016(see more posts on EUR/CHF, ) . - Click to enlarge |

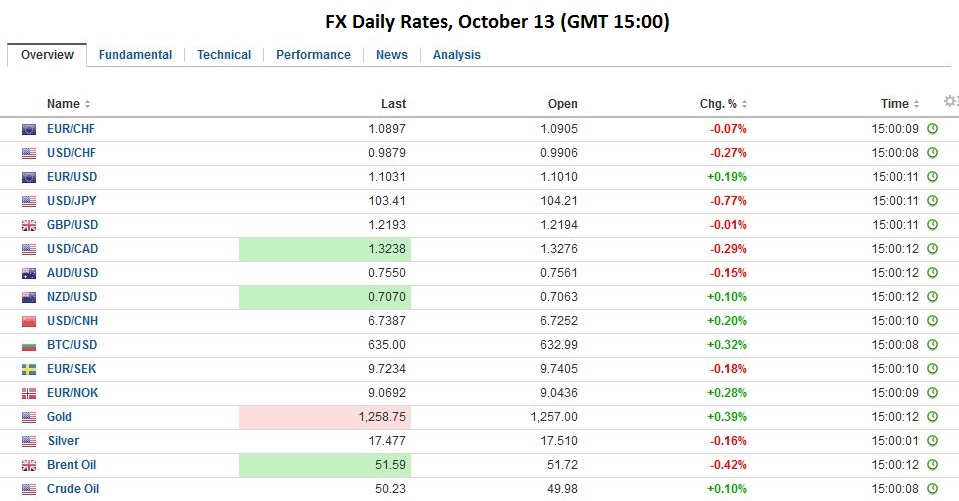

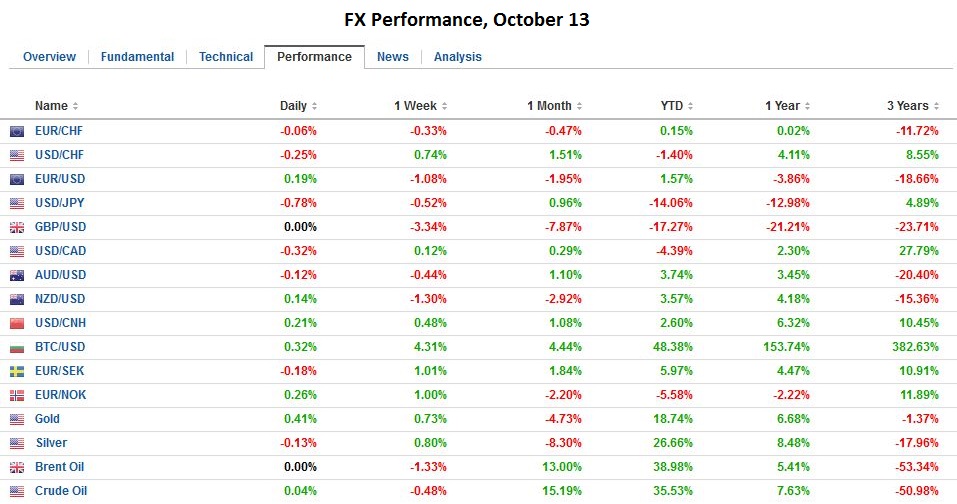

FX RatesThe US dollar is firm, and the euro has slipped below $1.10 for the first time since late-July. Although the dollar’s gains against nearly all the major and emerging market currencies are being attributed to the FOMC minutes, which underscored ideas that another hike was drawing near, US interest rates are a lower today. Both the two and 10-year yields yesterday rose to their highest levels in four months (87 bp and 1.80% respectively). Both are now 2-3 bp lower. The FOMC minutes suggested that understandings of the labor market were a critical issue that divided members. Yesterday’s JOLTS data in this context was not particularly helpful, though it is reported with an additional month lag behind the non-farm payrolls. The August JOLTS report showed the biggest drop in job openings year. The takeaway was healthy but slower. The decision to include a risk assessment for the first time since January in the FOMC statement coupled with the minutes underline that debate at the Fed is over the timing of the move, not direction. |

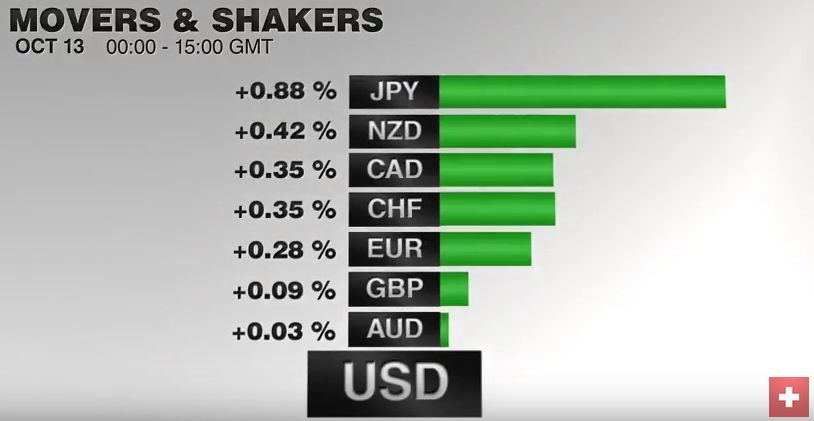

FX Performance, October 13 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| The euro held above $1.10 in Asia after it was approached in North America yesterday. European participants took it to $1.0985 before the single currency found a bid. The $1.1040-$1.1060 offer the initial cap. The dollar initially traded at its best level against the yen since late-July near JPY104.65. However, it was sold down a big figure to JPY103.55 in Asia. It has straddled the JPY104 level in the European morning. The yen’s 0.25% gain makes its the strongest of the major today.

Sterling is consolidating its losses but remains fragile. The $1.2090 low from Tuesday continues to hold. The wide ranges seen since the “flash crash” at the end of last week may be gradually easing. So far today, sterling has been confined to about 0.8 cents. Yesterday’s range was a little more than two cents. Sterling is struggling to sustain upticks above $1.2200. Above there, sellers may re-emerge near $1.2250. |

. - Click to enlarge |

| The Australian dollar is the weakest of the majors today, with a 0.25% loss through the European morning. The Chinese trade figures, news that October inflation expectations ticked up to 3.7% from 3.3%, matching the high for the year, and Fitch’s warning that a housing slump is the biggest risk saw the Australian dollar near $0.7500. Buyer emerged in late-Asian activity, and Europe took it back through $0.7540. The Aussie has pulled away from the $0.7700 cap that it had repeatedly tested in vain. It may have bottomed here today (near-term view). A move above $0.7585-$0.7625 band would spur another test on the cap.

Investors have turned cautious. Equities continue to slip lower. The MSCI Asia-Pacific Index is off 0.7% for its fifth consecutive decline. The losing streak matches last month’s May and April’s run. Recall it started the year with a seven-session slide. MSCI Emerging Market equities are off 1.1%, for the third consecutive losing session. |

. - Click to enlarge |

GermanyThe Dow Jones Stoxx 600 is off 0.8%. It is the third day of declines and the sixth of the past seven sessions. The weakest sector is financials, which are down twice the overall market. Deutsche Bank shares are off 2.55%, which is the biggest loss this month and is sufficient to push shares lower on the week. The losses come as the SEC fined the bank another $9.5 mln for failing to properly safeguard non-public information, while reports suggest the bank has implemented an immediate hiring freeze. Italy’s bank share index is off 1.5%. |

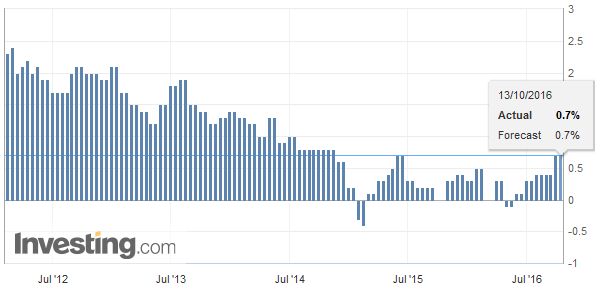

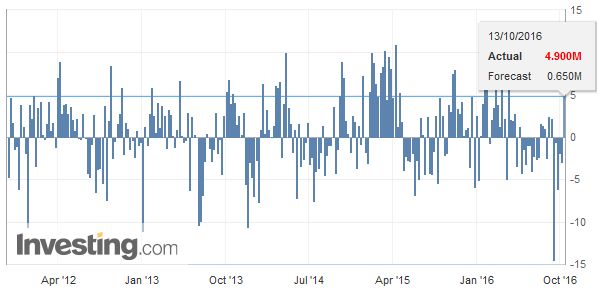

Germany Consumer Price Index (CPI) YoY, October 13 2016(see more posts on Germany Consumer Price Index, ) . Source: Investing.com - Click to enlarge |

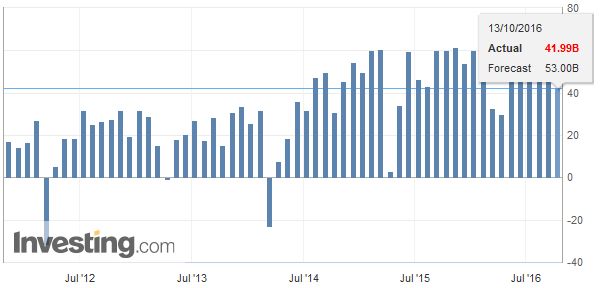

ChinaMeanwhile, the main news today has been China’s trade balance. The $42 bln surplus was much smaller than the market had expected. The median forecast from the Bloomberg survey was $53 bln, which would have been a small increase from August’s $52 bln surplus. It is the smallest surplus since the Lunar New Year distortions that saw the trade surplus fall to $32.5 bln and $29.6 bln in February and March. |

China Trade Balance, September 2016(see more posts on China Trade Balance, ) . Source: Investing.com - Click to enlarge |

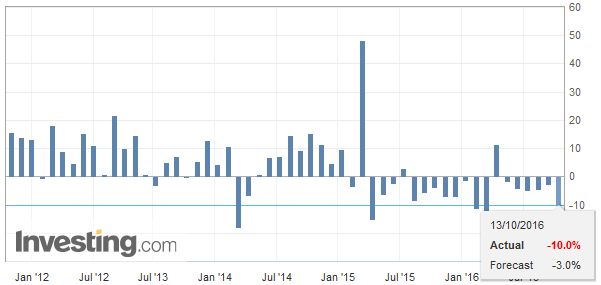

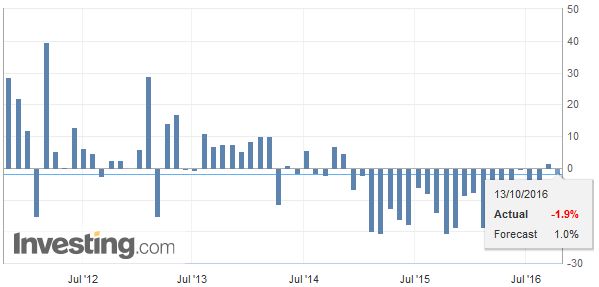

| Imports and exports were weaker than expected, and this plays on ideas that the Chinese economy is continuing to slow though other data has shown it is stabilizing. Exports fell 10% after falling 2.8% in August. Some deterioration was expected, but only about a third of what was reported. Imports fell 1.9% after rising 1.5% in August. Of note, exports to the EU fell 9.8%, and exports to the UK fell 10.8%. China may be more exposed to Brexit than generally perceived. Exports to the US fell 8.1%. Steel exports fell for the third month to stand at their lowest levels since February. |

China Exports YoY, September 2016(see more posts on China Exports, ) China . Source: Investign.com - Click to enlarge |

| Among imports, two products stand out. First, as a new strategic reserve site went online, China’s crude oil imports reached a new record high. Second, China’s copper imports fell for the sixth month to the lowest level since February 2015. Demand slowed, and domestic output increased. Domestic smelters increased output by 8.7% to a new record (5.5 mln tons) in the year through August. |

China Imports YoY, September 2016(see more posts on China Imports, ) . Source: Investing.com - Click to enlarge |

United StatesThe US reports import prices and initial jobless claims. Import prices are expected to firm in August, and a rise of more than 0.2% may warn of bigger than expected rise in tomorrow’s PPI reading. That said, the retail sales report tomorrow, released at the same time as the PPI, is the most important of the two releases. |

U.S. Initial Jobless Claims, October 13 2016(see more posts on U.S. Initial Jobless Claims, ) . Source: Investing.com - Click to enlarge |

| Weekly jobless claims were lower than expected last week, but it is next week’s report that coincides with the monthly survey for non-farm payrolls. The Fed’s Harker and Kashkari speak, but here too, tomorrow’s event, namely, Yellen’s speech at a Boston Fed conference, overshadows the regional Fed Presidents. |

U.S. Crude Oil Inventories, October 13 2016(see more posts on U.S. Crude Oil Inventories, ) . Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$EUR,$JPY,China,China Exports,China Imports,China Trade Balance,EUR/CHF,Germany Consumer Price Index,newslettersent,U.S. Crude Oil Inventories,U.S. Initial Jobless Claims