Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary

The two-day bounce in sterling seems technically driven rather than fundamental.

The Brexit decision has set off a unfathomable chain of events whose impact and implications are far from clear.

The economic hit on the UK may spur a BOE rate cut, even if not QE, as early as next month.

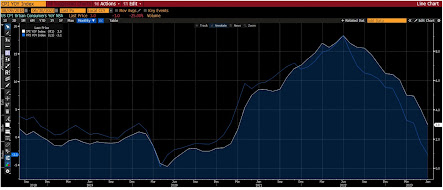

After plummeting 18.6 cents, mostly in a few hours after it became clear that the Brexit would carry the day, sterling has rallied four cents from the low set on Monday. We recognized that the magnitude of the drop left sterling technically over-extended, but we caution against suggests that the worst is behind us and that a durable low is in place.

After plummeting 18.6 cents, mostly in a few hours after it became clear that the Brexit would carry the day, sterling has rallied four cents from the low set on Monday. We recognized that the magnitude of the drop left sterling technically over-extended, but we caution against suggests that the worst is behind us and that a durable low is in place.

This week’s high so far was recorded on Monday around $1.3565. Today’s high has stopped short of this, and beyond it is last week’s close near $1.3680.

Sterling’s firmer tone does not have anything to do with positive developments in the UK. The Tory leadership contest is formally underway, and the nomination phase will end tomorrow. Starting July 5, on Tuesdays and Thursdays, there will be a ballot among Tory MPs in an attempt to narrow the contest to two candidate. The Labour Party is edging toward its own leadership challenge.

It may take a few weeks before the shock feeds into economic reports. Expectations for a BOE rate cut as early as next month (July 14) have risen. From the high point last week to the low point at the start of this week, the implied yield of the September short-sterling (three-month deposit) fell 20 bp. They have recovered about five bp. Many economists are projecting a recession.

Sterling’s gains do not appear to reflect fundamental developments. Instead, we suggest the gains are driven by two considerations. First, is the money management of momentum traders. Once sterling stopped falling, short-term participants (fast-money) bought to take profits on short positions. Remember, in the futures market; speculators had were carrying one of the largest bearish bets on sterling on record (gross shorts = 93.7k contracts–each is for GBP65000). Second, institutional invests are adjusting portfolios and (currency) hedges ahead of the month- and quarter-end.

It is important to recognize the high degree of uncertainty. This will likely keep many institutional portfolio managers on the sidelines. They do not have to be in a hurry. It is true that over the past five sessions, the FTSE 100 is the only major European market that is higher (~1.0%). This is in local currency terms. In dollar terms, the 6.7% slide is a little more than the region’s large markets, including the DAX, CAC, and Dow Jones Stoxx 600. The same is true when returns are calculated in euro and yen. The US holiday on Monday may also discourage new position-taking, and then one might as well wait until the US jobs report on July 8 (early estimates are mostly 150k-180k, which would represent a significant recovery from May’s 38k, even if below the 200k threshold).

While investors are debating the direct and indirect economic consequences of Brexit, and the Fitch and S&P wasted no time to cut the UK’s credit rating, the political implications are far-reaching. The politics within the EU are going to change dramatically. Those countries, like in Eastern and Central Europe, as well as Sweden, who are members of the EU, but not EMU, are going to lose an articulate advocate. Germany is going to lose an ally in resisting the statist approaches that France and Italy often propose.

While the EU is 20% smaller without the UK, the UK itself may see defects. A majority of Scotland and Northern Ireland voted to remain. EC President Juncker seemed so intent on punishing the UK that he was willing to antagonize Spain by suggesting Scotland deserves a hearing about staying in the EU.

Italy’s attempt to address its banking system was faltering before the UK referendum, which effectively made things worse. Prime Minister Renzi’s effort to find a European-wide solution has been firmly rebuffed by Merkel. It is incumbent to find a purely domestic solution without drawing on taxpayers money. Even though nearly every other member in EMU used such state money (except for Italy), that path has been blocked by recently approved Bank Recovery and Resolution Direction.

Some people may link the softening of Renzi’s support with the decision at the end of last year to close four relatively small banks and bail-in some bondholders.However, the takeaway from such a narrative would be to tread cautiously ahead of the October constitutional referendum. That referendum will be more about Renzi than the merits of the constitutional reform he has proposed. If that is the case, Renzi needs to do something to regain the reform momentum and re-energize his base.

One such path could be to allow Italy’s development bank Cassa Depositi e Prestiti (CDP) to issue bonds that could be used to reform and recapitalize Italy’s banks. Those bonds could meet the criteria for ECB purchases. The funds could be provided to banks on strict conditions of reform, which is not just about non-performing loans, Italy appears to have too many banks

Under the status quo, Renzi is likely to lose October referendum. He say if that happens he will step down. Renzi needs to do something big, but Merkel blocked his initial overture. He must of known that was going to happen. He can double down on reform, or he may very well go home.

The UK has not officially triggered Article 50 of the Lisbon Treaty, but its influence has already begun to wane. It has not formally been told that it will not be allowed to assume the rotating EU presidency in 2017 as scheduled. The UK has long been ambivalent about a EU military force, preferring to work through NATO. The divorce proceedings have not even begun, and Europe is moving forward with a new defense and securities initiative.

The effort stops shy of an EU army or headquarters, two issues that the UK opposed, but it does entail greater coordination of more shared military resources and R&D. It also shifts the recognition of Russia from a strategic partner to a strategic challenge. The new proposals by the EU’s foreign policy chief Mogherini appear to enjoy the backing of Merkel and Hollande.

The economic consequences of Brexit have not been felt yet in the UK or elsewhere. The policy response has yet to be seen. Some policy responses may be known in by their absence, as in a Fed rate hike, which the market apparently has given up on this year and next. Contrary to what it may seem like, the US dollar did not appreciate markedly on a trade-weighted basis, despite seemingly large currency swings.

The Bank of England’s trade-weighted measure of the dollar is 99.50 today. It finished last month at 101..40. It is has not been above 100.10 since the referendum results. Rather than in the foreign exchange market, the interest rate market had the larger reaction. The shock is seen as a headwind for growth and another check on inflation.

There are many delicate political balances, especially but not limited to Europe, which will have to find a new equilibrium. The UK is not only leaving a hole in EU finances but also in leadership. French and German elections next year take on added significance. A banking and /or political crisis in Italy in a few months, which is, of course, largely independent of the UK’s decision, needs to be avoided.

There are many known unknowns. That is hard enough for investors, but there are seemingly countless unknown unknowns as well. The path ahead was never envisioned to be easy, but the Brexit decision adds a new dimension to difficult.

Full story here Are you the author?

Tags: Angela Merkel,Article 50,Italy,Matteo Renzi,newslettersent,Post-Brexit