Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The global capital markets are stabilizing for the first time since the UK referendum. It is not uncommon for markets to move in the direction of underlying trends on Friday’s; see follow-through gains on Monday, and a reversal on Tuesday. That is what is happening today. Turnaround Tuesday after such dramatic price action over the last two sessions has the feel of the proverbial dead cat bounce.

The global capital markets are stabilizing for the first time since the UK referendum. It is not uncommon for markets to move in the direction of underlying trends on Friday’s; see follow-through gains on Monday, and a reversal on Tuesday. That is what is happening today. Turnaround Tuesday after such dramatic price action over the last two sessions has the feel of the proverbial dead cat bounce.

Brexit

There has been no significant fundamental driver. The UK was downgraded by S&P and Fitch yesterday. Both now stand at AA with negative outlooks. There are often knock-on effects when a sovereign gets downgraded. For example, the banks are typically not far behind. This should not be surprising.

Meanwhile, there has been revolt in the Labour Party, being led by members of Parliament.They will hold a vote of confidence today amid disappointment with last month’s election results, the lackluster campaigning against Brexit and the alienation of the party’s large donors. Corbyn support, which elected him a year ago, from the party’s rank and file which is to the left of the MPs. The referendum may start the more formal process of a leadership challenge. The results will likely be known in the North American afternoon.

The Tory Party brought forward its leadership contest. It had been scheduled for early-October. Now it is September 2. This brings this Schrodinger’s cat-like situation to a little more than two months rather than three, which still seems like a unnecessarily long period for uncertainty to fester. Merkel has already indicated, and others will follow suit, an acceptance that the UK will not trigger Article 50 immediately, despite what Cameron had indicated previously. However, Merkel was also clear; there is nothing to negotiate until the Article 50 is invoked.

Spain’s weekend election did not result in a large vote for anti-EU parties, but the center-right’s overtures to potential coalition partners has been rebuffed. Rajoy himself is part of the obstacle, but after scoring an unexpected victory (that leaves the PP still shy of a majority) he does not see why he should step down. However, the overall corrective mood of the market has not seen Spain punished for what could be another protracted political stalemate. Spanish 10-year bond yields are off eight bp. Italy’s benchmark yield is six bp lower. Spanish equities are up nearly 3%, while lagging Italy’s 4% rise, they are outperforming the Dow Jones Stoxx 600 (~2.6%).

The MSCI Asia-Pacific Index slipped 0.3%, but MSCI Emerging Market equity index is up nearly 1% after losing 5% over the past two sessions. Emerging market currencies are all firmer on the day, led by the South African rand (1.8%) and the Polish zloty (1.5%). The S&P 500 looks about 1% higher.

Core bond yields are 2-4 bp higher while peripheral bond yields are lower. Oil is trading nearly 2% higher after plummeting 7% in the previous two sessions. Similar, but opposite, gold is off 1% after gaining 5% since the UK voted to leave.

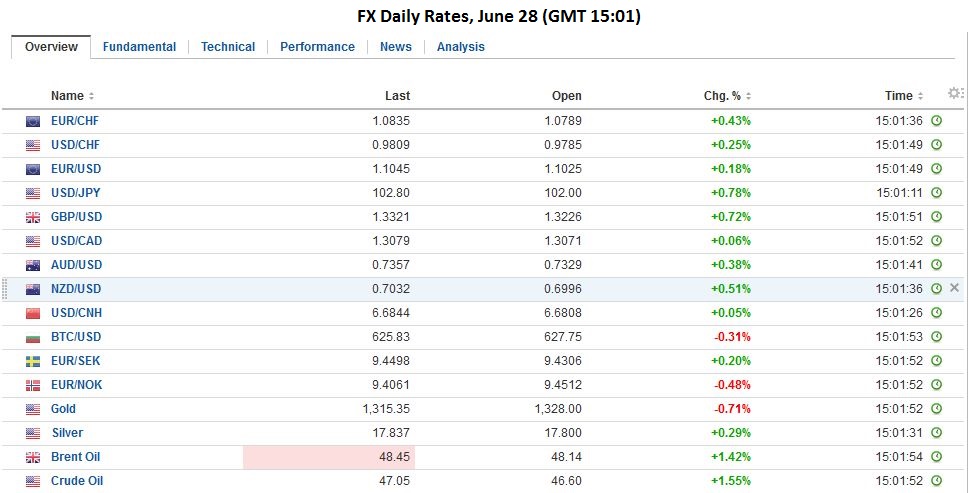

FX RatesWith today’s gains, the euro has retraced 38.2% of the Brexit decline. A move above $1.1110 gives potential toward $1.1170. The 61.8% retracement is found near $1.1230. |

Click to enlarge. |

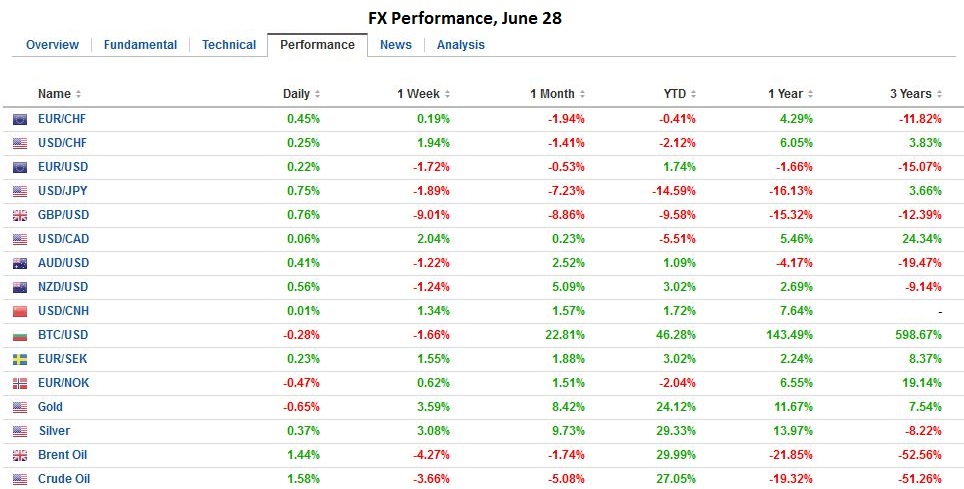

| The dollar is trading within yesterday’s range against the yen but seems to want to move higher. Initial resistance is seen near JPY103.00 and then JPY103.45. |

Click to enlarge. |

British pound

Sterling bounced from $1.3120 yesterday to a little more than $1.3370 today. There may be potential toward $1.3400, but the risk is that sterling stops shy of technical objectives, which is also a symptom of the poor sentiment.

Australian Dollar

The Australian dollar is also inside yesterday’s range. We had thought the Aussie could outperform this week. If this is indeed the case, it would be helpful for it to move above $0.7440 toward $0.7480. We also recognized that in a strong US dollar environment, the Canadian dollar typically does better on the crosses. Higher oil prices have not yet sent the US dollar through yesterday’s lows in the Canadian dollar, but it appear poised to do so shortly. A break of CAD1.2950 could see CAD1.2900.

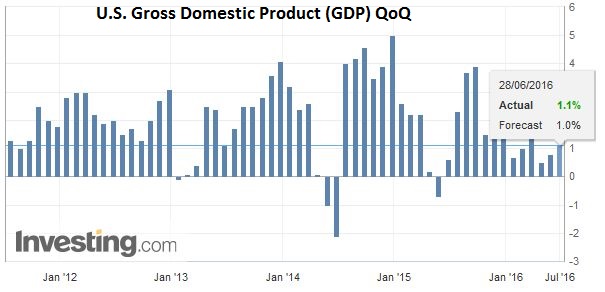

Economic Data: United StatesUS Q1 GDP is too historical for the revision, likely upward, to command much attention. Corporate profits may be more interesting for equity investors. |

Click to enlarge. Source investing.com |

| Case-Shiller house prices and |

Click to enlarge. Source investing.com |

| the Richmond Fed manufacturing index is not the stuff that captures the markets’ attention in more normal conditions, and even less so now. The Fed announces the results of its latest stress tests tomorrow. |

Click to enlarge. Source investing.com |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: Article 50,Australian Dollar,British Pound,FX Daily,GDP,Japanese yen,newslettersent,Post-Brexit,U.S. Case Shiller Home Price Index (Macro),U.S. Consumer Spending,U.S. Gross Domestic Product