Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Invest Or Index – Exploring 5-Different Strategies

Invest Or Index – Exploring 5-Different Strategies15 Sep 2025

Speculator Or Investor? 10-Rules From Legendary Investors

Speculator Or Investor? 10-Rules From Legendary Investors25 Apr 2025

S&P 500 – A Bullish And Bearish Analysis

S&P 500 – A Bullish And Bearish Analysis10 Sep 2024

Technological Advances Make Things Better – Or Does It?6 Sep 2024

Risks Facing Bullish Investors As September Begins

Risks Facing Bullish Investors As September Begins3 Sep 2024

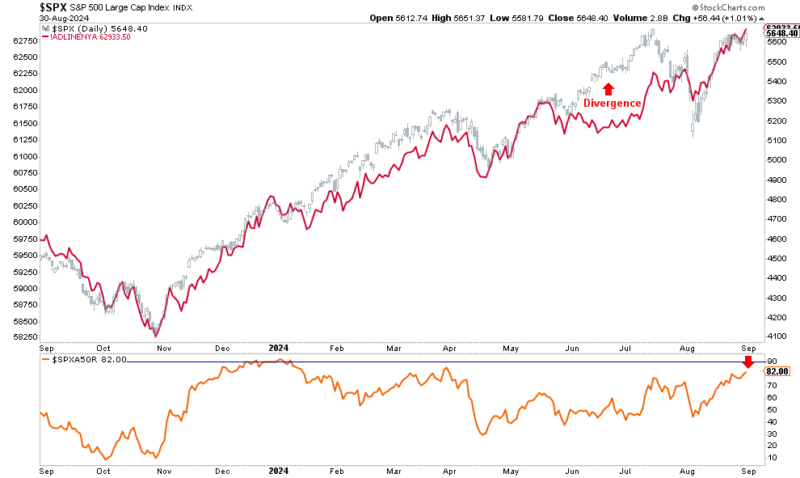

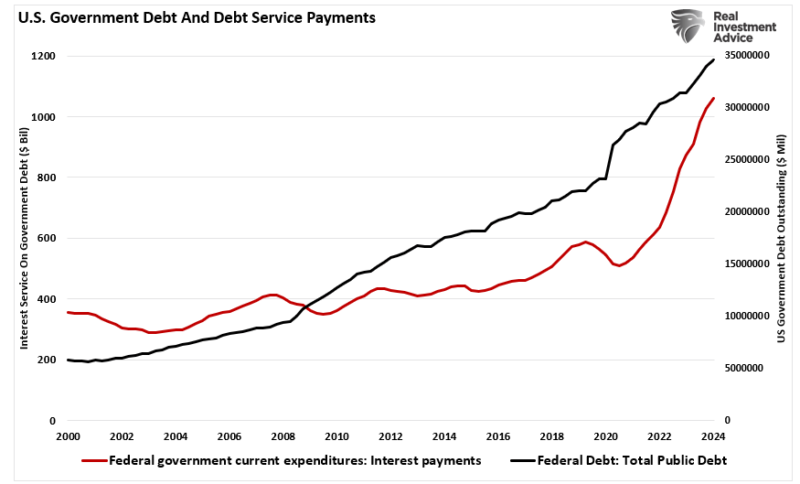

Japanese Style Policies And The Future Of America

Japanese Style Policies And The Future Of America30 Aug 2024

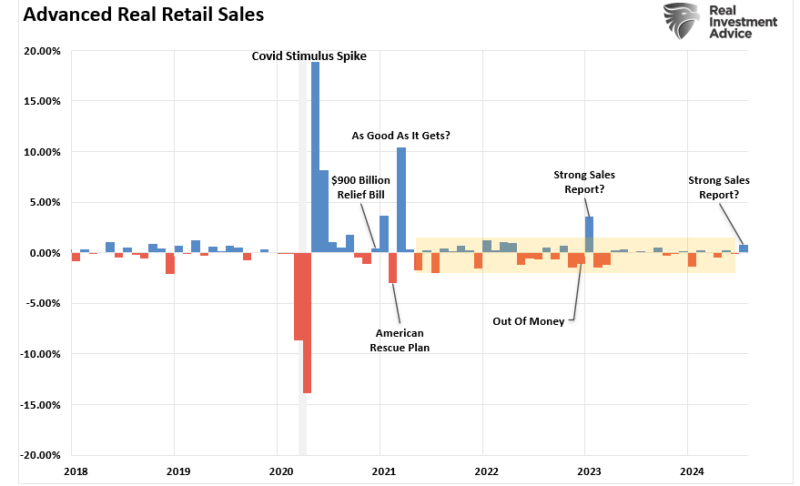

Red Flags In The Latest Retail Sales Report

Red Flags In The Latest Retail Sales Report23 Aug 2024

Dollar Mixed as Markets Digest US Political Developments22 Jul 2024

Macro: GDP Q3 — Inflationary BOOM!

Macro: GDP Q3 — Inflationary BOOM!22 Dec 2023

Is the Market Putting on Risk Ahead of the Weekend?27 Oct 2023

Market Awaits US Data and Leadership30 Aug 2023

Markets Becalmed Ahead of Key Data and BOJ Meeting Outcome27 Apr 2023

Weekly Market Pulse: Look Up In The Sky! It’s A UFO! Or Not!13 Feb 2023

Weekly Market Pulse: The Real Reason The Fed Should Pause11 Oct 2022

Goldilocks Calling

Goldilocks Calling2 Sep 2022

Weekly Market Pulse: Opposite George

Weekly Market Pulse: Opposite George1 Aug 2022

The Fed and GDP: Week Ahead23 Jul 2022

Sorry Chairman Powell, Even FRBNY Now Has To Forecast Serious and Seriously Rising Recession Risk20 Jun 2022

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.6 Jun 2022

Another Month Closer To Global Recession26 May 2022