Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

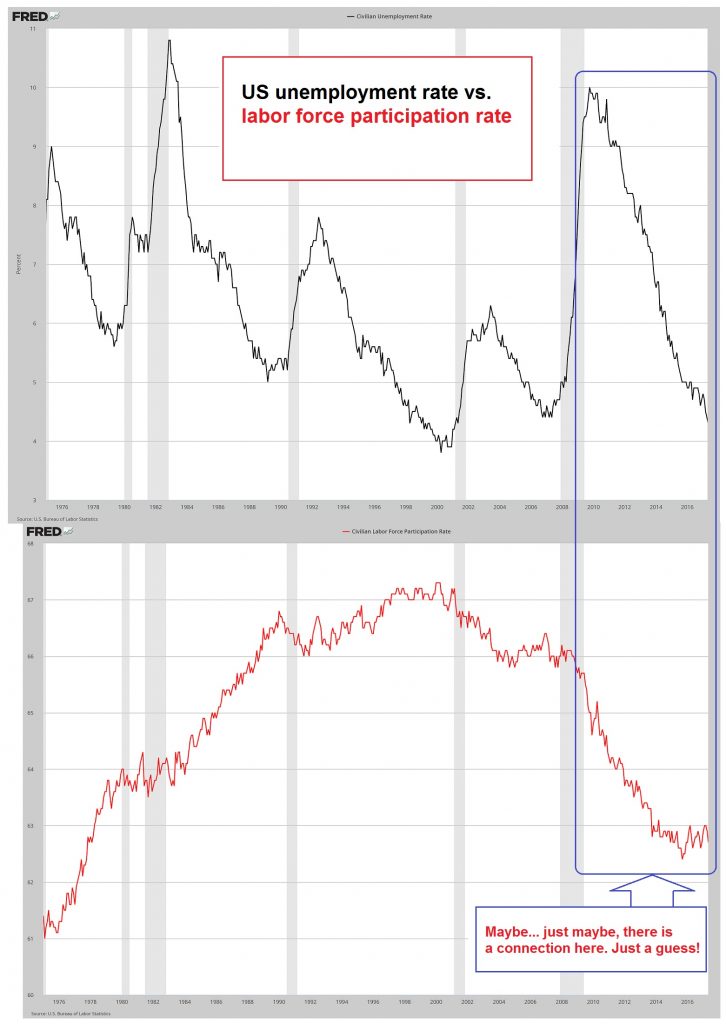

The US dollar traded higher before the weekend with the help a fairly robust jobs report. Although the jobs growth itself was somewhat disappointing, the details were constructive: More people working a longer work week and earning more. The participation rate rose, and the unemployment rate (U-3) fell. The Atlanta Fed GDPNow tracker increased to 2.2% in Q1 16 from 1.2% at the start of the week.

Despite the pre-weekend gains, the greenback lost ground against all the major currencies last week. We had anticipated a stronger showing for the dollar following the BOJ surprise rate cut and the ECB's reassessment of its monetary policy next month. The market has jumped from the China-driver to oil and now to the risks of a US recession. We did not anticipate the rise of this fear outside of a few who have been pessimistic throughout the entire expansion cycle.

Neither the US jobs data nor the prospects for a stronger economic recovery in Q1 will persuade the cynics that the US is not recession-bound. Here the tightening of the financial conditions are important, and NY Fed President Dudley cited this in a recent speech. The Survey of Senior Loan Officers showed a tightening of lending conditions and weaker demand for the second consecutive quarter.

This means that real sector data, like the jobs report, but also next week's retail sales, to push back against the recession talk. While next FOMC meeting is five weeks away, it is difficult to see the pendulum of expectations swinging back in favor of a March hike.From a technical perspective, the dollar's pullback has been largely corrective in nature. Leaving aside the yen, against the other major currencies, the dollar is correcting a run-up that began in mid-October. The chief exception is sterling, which arguably is retracing the move that began in December. This is not to say there has not been a fundamental development. We do recognize that interest rate differentials have narrowed as the market had nearly priced out any rate hike by the Fed this year. We continue to expect that the Obama dollar rally has more life in it, and overtime the negative rates in Europe and Japan will encourage the demand for dollars and dollar-denominated assets.

The losses in the Dollar Index allowed to finish a retracement of the run-up since mid-October. The 61.8% retracement was found near 96.35. Although it briefly traded through in last Thursday and Friday, it managed to close above there both days. It closed more than three standard deviations below its 20-day average on Thursday. This extreme performance was seen at the last August low as well. Despite the jobs-inspired gains, it still struggled to re-enter the Bollinger Band (~97.25), which is set two standard deviations around the 20-day average. A move above 97.65 would help stabilize the technical tone, which remains fragile.

The euro broke out of the $1.08-$1.10 trading range last week. There have been other false breaks since the trading range was established in December. The euro's gains faltered near the 61.8% retracement of the down move since late-August (~$1.1260). Initial support may be found near previous resistance ($1.1000-$1.1040). Medium-term investors who continue to expect that the divergence of monetary policy will support the dollar over time may want to take advantage of any further euro gains.

After the BOJ rate cut surprise at the end of January, we had expected further yen weakness. However, the drop in equities and US yields offset the monetary policy considerations and drove the dollar from near JPY121.40 to JPY116.30. The technical indicators are mixed, but the inability to move through JPY117.50 after the US jobs data and rise in US rates is disappointing. At the same time, many observers suspect that the BOJ could cut rates further if the yen's strength persists. The JPY116.00 area is still key support for the dollar. A convincing break could open the door to significant dollar losses, and would likely coincide with further market turmoil.

Sterling rose to almost $1.4670 last week. It surpassed the 61.8% retracement of the leg down that began on December 28 (from ~$1.4970) and was found near $1.4630. It fell to $1.4450 before the weekend. The next downside target is near $1.4375, and a break of $1.4300 would suggest the correction that began on January 21 is complete.

Dragged lower by oil and widening interest rate differentials, the Canadian dollar's 11.3% loss from mid-October through January 20 made it the weakest of the major currencies. It snapped dramatically back over two and a half weeks. It appreciated nearly 7%. The US dollar spiked to CAD1.3640 on February 4. The 6.18% retracement objective is found near CAD1.3540. The divergence of the US and Canada's labor markets, wider rate differentials, weaker stocks, and oil, saw the Canadian dollar soften by almost 1% before the weekend, and it finished poorly. There is a reasonable chance the US dollar's downside correction is over. A move above CAD1.3930 would lend credence to this view, with a move through CAD1.40 targeting CAD1.4160 initially.

The Australian dollar met the minimum measuring objective of the head and shoulders bottom pattern we have been discussing over the past couple of weeks. It came in near $0.7250. The Aussie was sold before the weekend, falling back below $0.7100. It finished on the session lows. The immediate downside risk extends toward $0.6985-$0.7035.

In the softer US dollar tone allowed the Mexican peso to claw back some of its recent losses. However, the dollar's pullback stops just shy of the MXN18.00 level. A move now above MXN18.50 warns of another run to the record high seen in late-January near MXN18.80. The only thing that would negate this dollar bullish view is if the dollar falls through MXN17.90.

The US 10-year yield fell to 1.79% on February 3. It is the lowest in a year. Despite the constructive employment data, yields did not resurface the 1.90% level that had been the floor in August and October. The technical indicators on the March note futures contract have not turned. A break of 129-25 would suggest the low print in yields is in place. The 20-day moving average is a full point lower at 128-25. A convincing violation of it would likely signal the end of the rally that began at the end of last year.

The March crude oil contract traded in a wide range ($29.40-$34.20) last week and finished about $2.30 lower. The high was set on Monday, and the low was set on Wednesday. Choppy trading prevailed throughout. Within the $30-$35 trading range, anything is possible, but a break of that range probably is the direction of the next $5 move.

The S&P 500 also made is highs for the week on Monday and the lows on Wednesday. The 1950 area marks the near-term cap. Technical indicators still warn of downside risks. A break of 1872 signals a return toward 1850, if not 1812, the spike low from January 20.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: U.S. Participation Rate