Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The US dollar is narrowly mixed. The euro and yen remain within yesterday's ranges, while sterling continues to trade heavily. The stabilization of oil prices has not lifted the Canadian dollar, while the other Antipodean currencies turn higher.

Emerging market currencies are mostly lower, though the South African rand is slightly firmer. The Russian ruble's decline has been extended into the fourth sessions and brings its loss this month to 8.5%, the worst performing emerging market currency after the Argentine peso that sank as it was floated.

Equity markets are mostly higher. The MSCI Asia-Pacific Index is rose a little more than a 0.33% to reach a three-week high. The index is still off about 4.4% this year, which will be the second consecutive losing year. Chinese shares rose nearly 1% in light volume after posting their biggest decline in a month yesterday.

Australian and New Zealand markets opened after a two-day holiday and both rose over 1%. European bourses are rallying. The Dow Jones Stoxx 600 is up about 0.9% near midday in London, with utilities, health care and consumer discretion leading the way. It has been a difficult December for European equities. The Dow Jones Stoxx 600 is off 4.65% this month, which is the worst December in more than a decade. Indicative pricing suggests the S&P 500 may open 0.4% higher.

Bond markets are trading heavier in Europe with German and French 10-year benchmark yields three basis points higher. Spanish, Italian and Portuguese yields are flat. The 10-year gilt yield is off 2 bp, after UK markets were closed yesterday. Australian and New Zealand bonds also rallied upon their return from the two-day holiday.

We note that the US two-year premium over German stands at new multi-year highs today of 140 bp. Although euro has not responded, we see this as lending credibility to our argument that the euro's bounce is corrective in nature. The widening interest rate differential provides a powerful and ongoing incentive to be long US dollars. Similarly, the US two-year premium over the UK has also jumped to new multi-year highs near 45 bp. It was less than 10 bp in early November, when sterling was trading near $1.55. Likewise, the US two-year premium over Canada is also continuing to rise. Indicative prices put it near 58 bp. It began the month near 30 bp.

In the light economic calendar Spain stands out. Retail sales rose 3.3% on a seasonally adjusted year-over-year basis. The Bloomberg consensus called for a 4.6% increase. The October series was revised to show a 6.0% gain rather than the 5.8% initially reported. The last time Spanish retail sales fell on this basis was July 2014. Tomorrow Spain reports its preliminary December CPI. The harmonized measure is expected to rose to 0.1% from -0.4%. It has not been above zero since May 2014.

Spain's political situation remains far from clear. The Socialists appear to have ruled out a coalition with Podemos on grounds that it supports a referendum on Catalonia's independence. The chances of a grand coalition of the center-right PP and center-left Socialists were never high and appear to be receding. Meanwhile, Catalan politics are also very fluid. It also cannot put together a new government (election was in September). The pro-independent, but anti-EU and anti-NATO left Popular Unity Candidacy (CUP) is split over whether to support CDC's Mas. If there is no agreement by January 9, new elections are mandated.

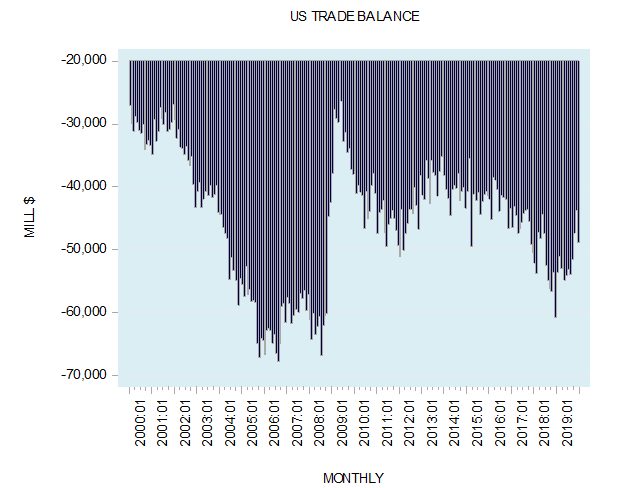

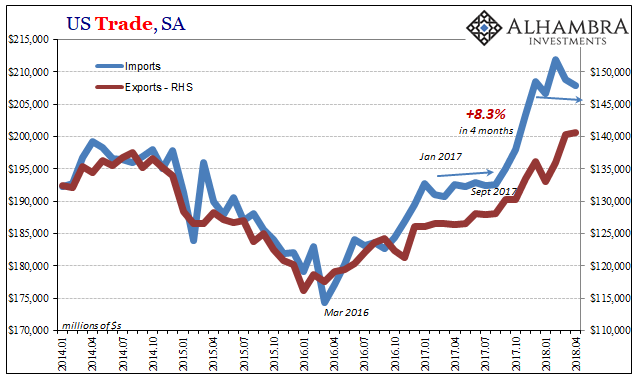

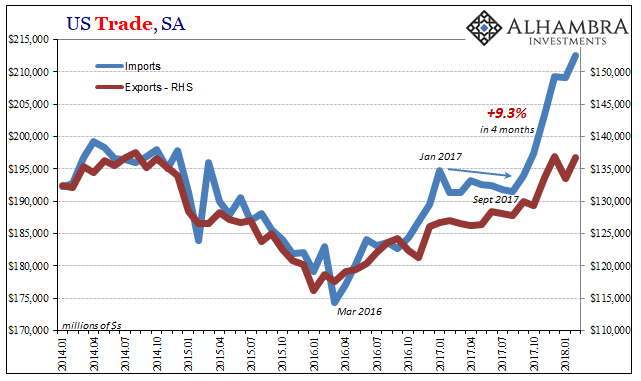

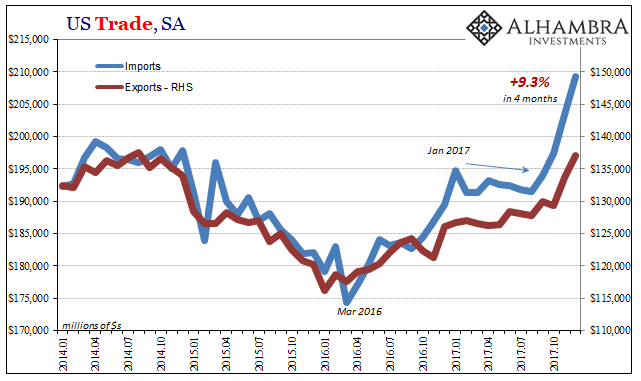

US data today includes the advance goods trade report and S&P/Case-Shiller house prices. The combination of a stronger US dollar and growth differentials have seen some deterioration of the US trade balance. The three-month average shortfall in Q4 14 was $60.66 bln. In October, the monthly deficit averaged $62.32 bln over the past three months. House prices in the top 20 urban centers rose 4.35% in 2014 and are up 5.45% year-over-year in September. The Bloomberg consensus calls for a 5.6% year-over-year rise in October.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: U.S. Trade Balance