Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

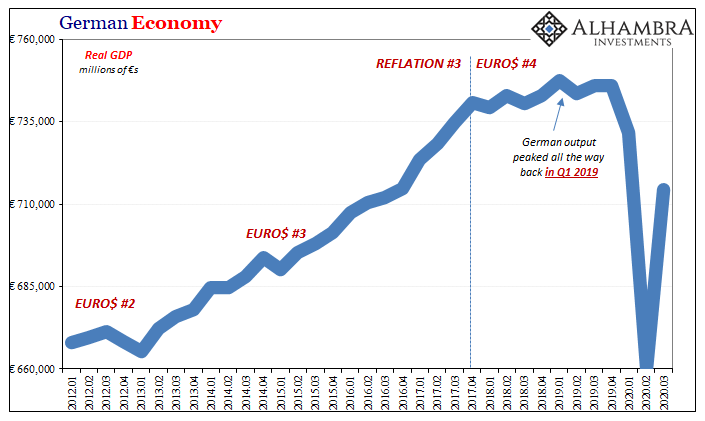

Is It Recession?

Is It Recession?30 Apr 2022

Shanghai’s Current Plight Began in 2017

Shanghai’s Current Plight Began in 201723 Apr 2022

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)3 Nov 2021

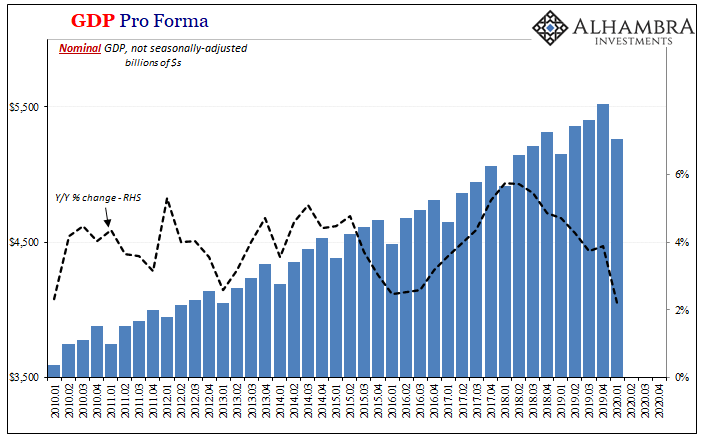

GDP Red Flag

GDP Red Flag31 Oct 2021

Meanwhile, Outside Today’s DC

Meanwhile, Outside Today’s DC5 Nov 2020

It Was Bad In The Other Sense, So Now What?

It Was Bad In The Other Sense, So Now What?18 Aug 2020

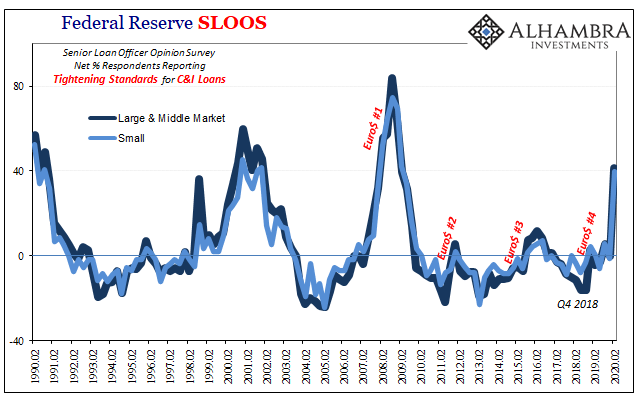

Not COVID-19, Watch For The Second Wave of GFC2

Not COVID-19, Watch For The Second Wave of GFC227 Jun 2020

Getting A Sense of the Economy’s Current Hole and How the Government’s Measures To Fill It (Don’t) Add Up

Getting A Sense of the Economy’s Current Hole and How the Government’s Measures To Fill It (Don’t) Add Up29 May 2020

Stagnation Never Looked So Good: A Peak Ahead

Stagnation Never Looked So Good: A Peak Ahead21 Mar 2020

What Happens When Central Banks Buy Stocks (ETFs)? Well, We Already Know

What Happens When Central Banks Buy Stocks (ETFs)? Well, We Already Know13 Mar 2020

As the Data Comes In, 2019 Really Did End Badly

As the Data Comes In, 2019 Really Did End Badly12 Feb 2020

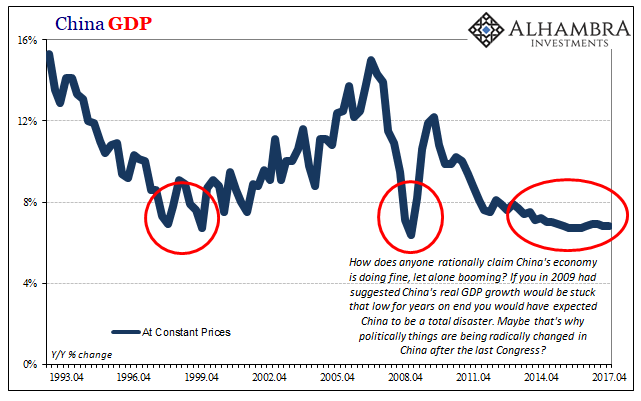

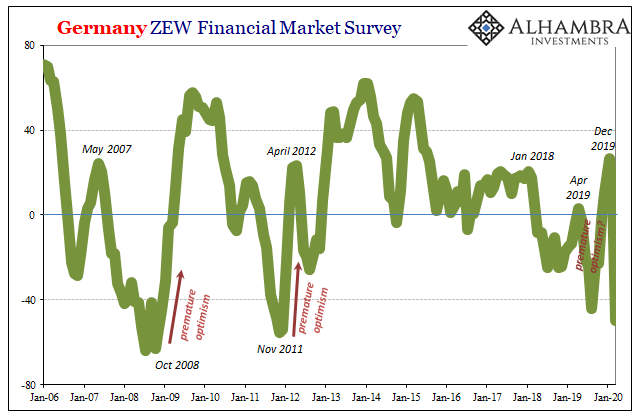

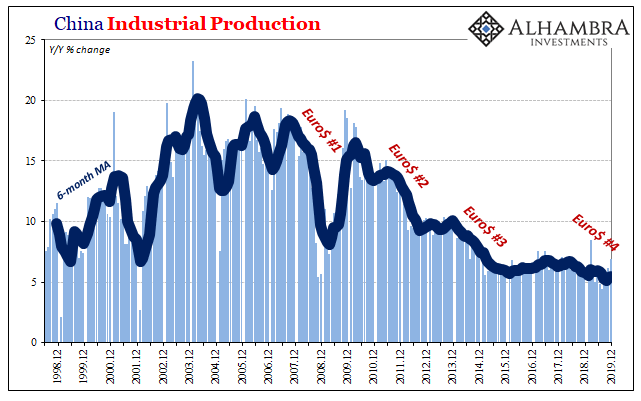

China Enters 2020 Still (Intent On) Managing Its Decline

China Enters 2020 Still (Intent On) Managing Its Decline21 Jan 2020

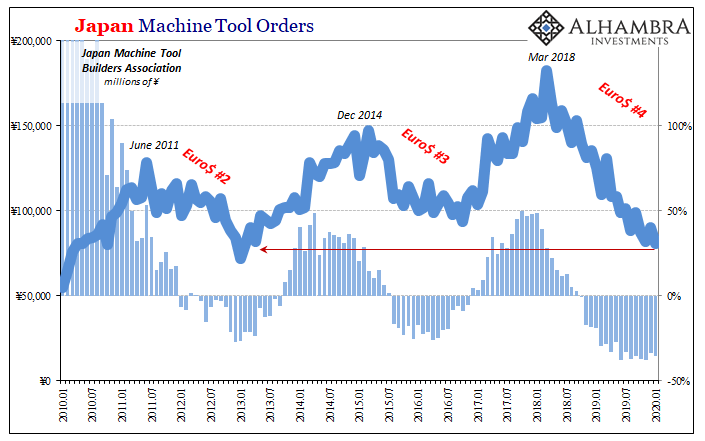

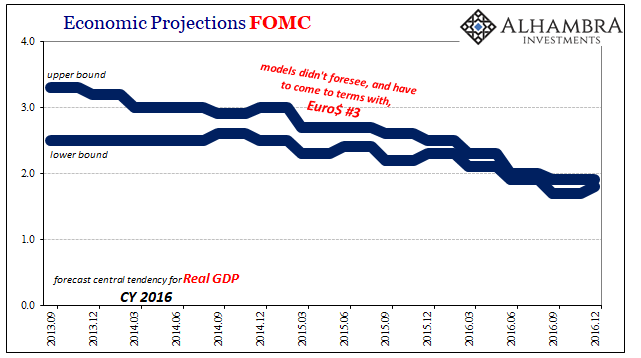

The FOMC Channels China’s Xi As To Japan Going Global

The FOMC Channels China’s Xi As To Japan Going Global13 Dec 2019

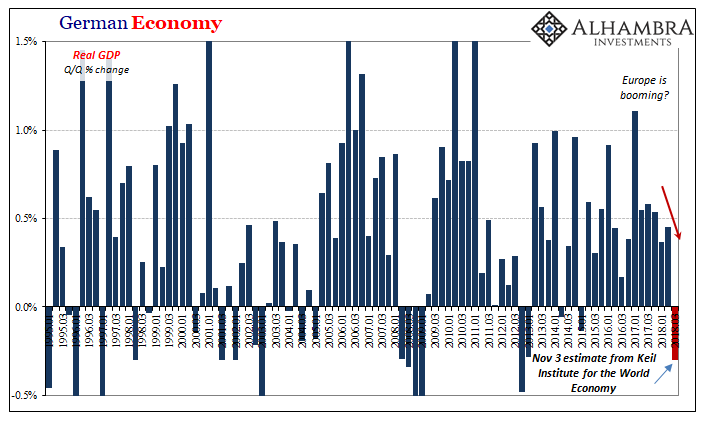

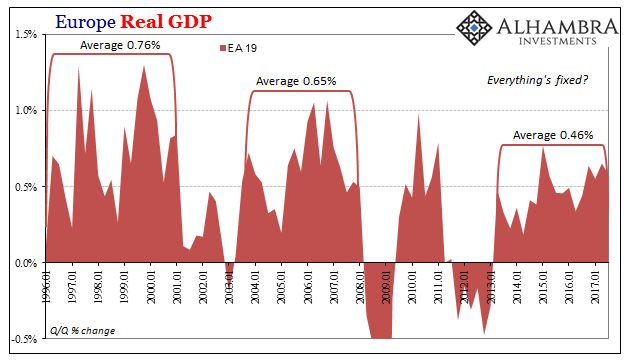

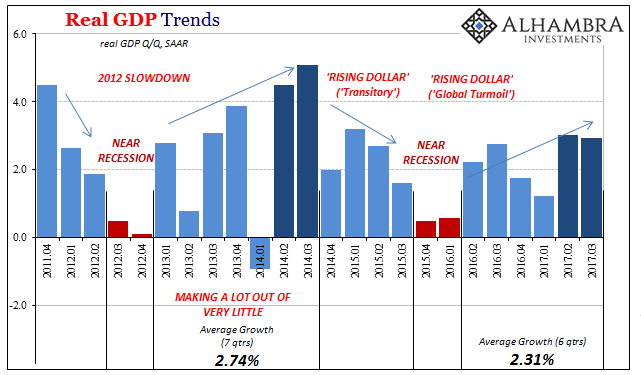

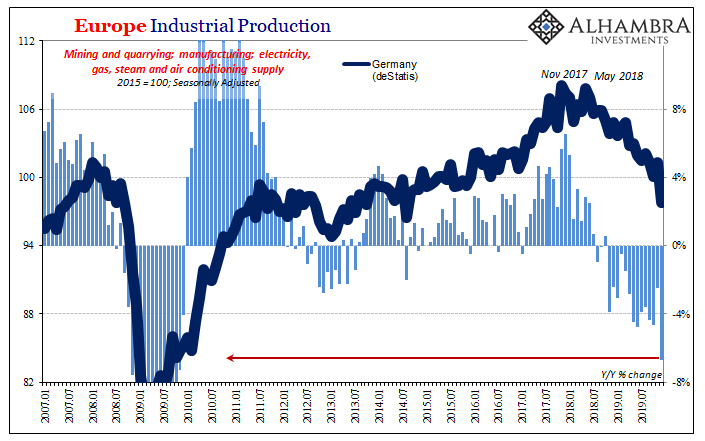

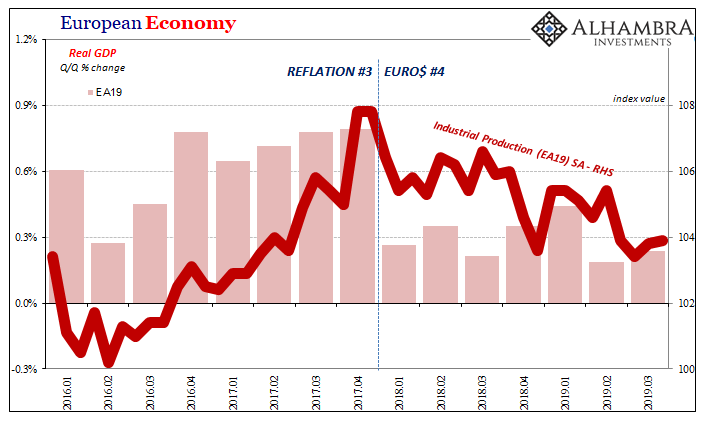

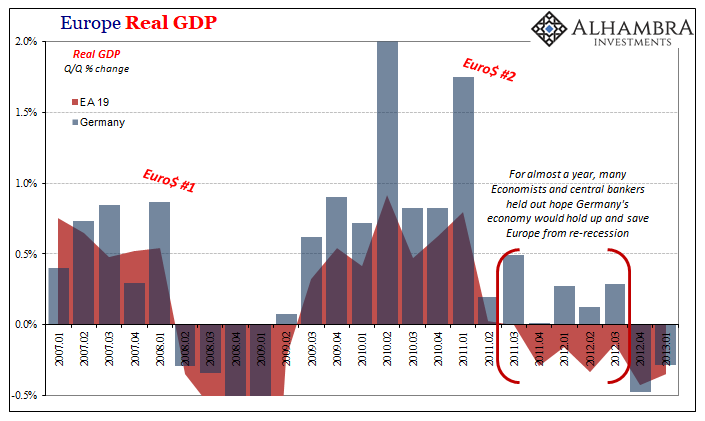

European Economy: A Time Recession

European Economy: A Time Recession8 Dec 2019

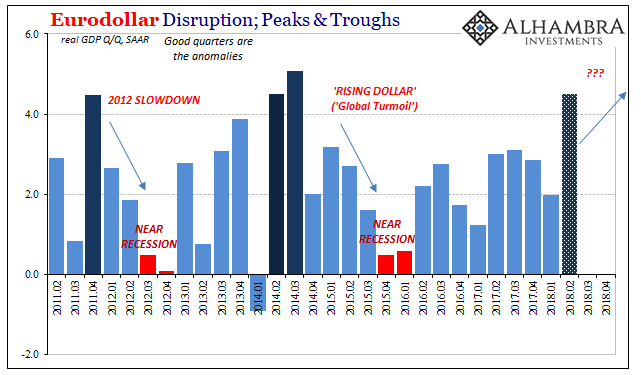

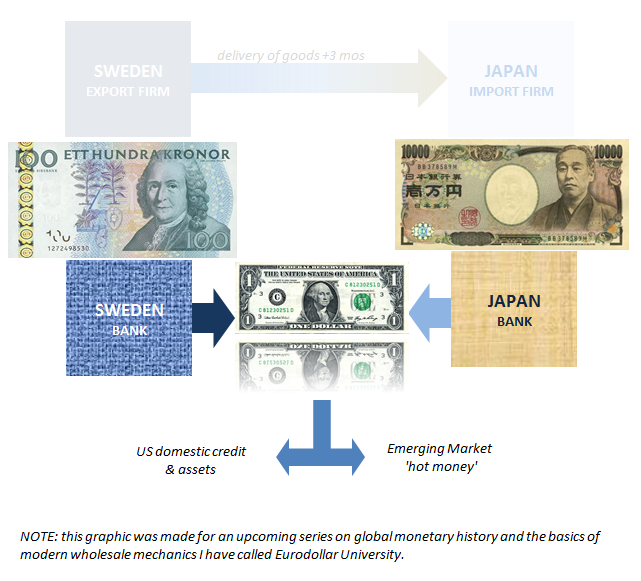

The Risen (euro)Dollar

The Risen (euro)Dollar5 Dec 2019

A Perfect Example of the Euro$ Squeeze

A Perfect Example of the Euro$ Squeeze10 Nov 2019

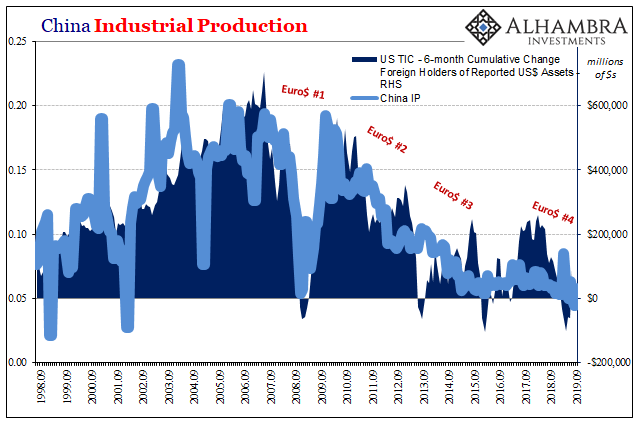

The Dollar-driven Cage Match: Xi vs Li in China With Nowhere Else To Go

The Dollar-driven Cage Match: Xi vs Li in China With Nowhere Else To Go22 Oct 2019

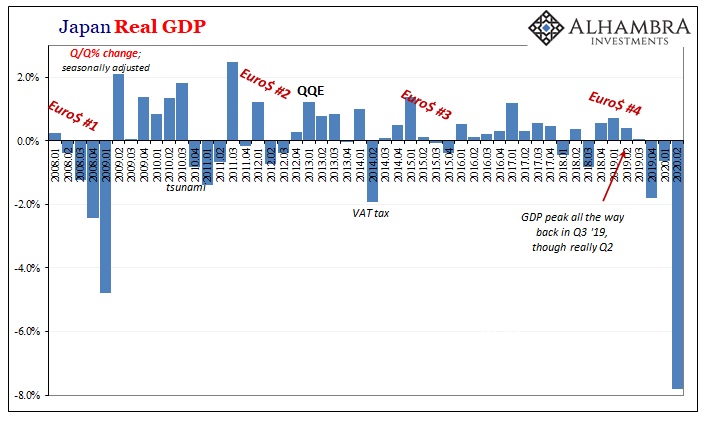

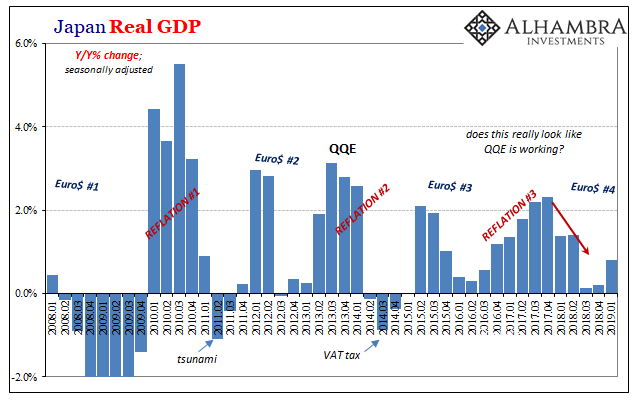

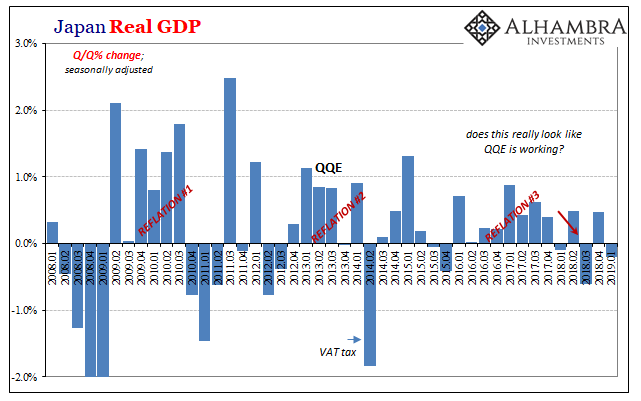

Japan’s Surprise Positive Is A Huge Minus

Japan’s Surprise Positive Is A Huge Minus21 May 2019

Effective Recession First In Japan?

Effective Recession First In Japan?16 May 2019

What’s Germany’s GDP Without Factories

What’s Germany’s GDP Without Factories9 May 2019