Jeffrey P. Snider

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

Back in October, the Bureau of Economic Analysis released GDP figures that suggested what those behind “reflation” had hoped. After a near miss to start 2016, the economy had shaken off the effects of “transitory” weakness, mainly manufacturing and oil, poised to perform in a manner consistent with monetary policy rhetoric. The Federal Reserve had been since 2014 itching to “raise rates” if for no other reason than to signal a successful end to their post-crisis mandate.

The advance estimate for Q3 2016 GDP was 2.9%, at the time the highest in two years dating back to 2014. It has since been revised up to nearly 3.5%, which does on the surface seem like an economy more so on the move. That was how it was interpreted in widespread fashion.

From CNBC:

“As long as you have consumer spending, some stabilization of capital spending, trade kicking in and inventories switching from being a significant drag, that balanced composition will make us confident that things are moving in the right direction,” said Anthony Karydakis, chief economic strategist at Miller Tabak in New York.

The New York Times:

“This is a good, solid number,” said Gus Faucher, deputy chief economist at PNC Financial Services in Pittsburgh. “The economy is growing at a decent clip. Consumer spending will continue to lead growth, and the fundamentals there remain positive.”

For all the quarterly blips, the ups and downs on Wall Street and the back and forth between political parties, the American economy remains more or less on the same trajectory since the recovery began more than seven years ago: modest but consistent growth.

There is it, the claim of “modest but consistent growth” that drives all this commentary. Nobody is really satisfied with the rate of expansion, but at least, we are told, it is expansion. That idea implies that at some point the pace will pick up, and if the Fed is trying to “raise rates” it must be just around the corner. No wonder people are so confused.

As always, we have to define these terms because these words are not being used in a manner consistent with their general meaning. For one, “consistent growth.” It and others like it refers to what is a substitute standard for recovery. Officials in particular have over the past year with greater frequency alluded to the length of this economic expansion, as if that was some meaningful achievement. Therefore, what “consistent growth” is transformed into is something different from what it has meant in the past.

| The fact that quarterly GDP has not indicated recession, several quarters of negatives, does not alleviate the depression burden; if anything, it makes it worse (the worst case). Stuck in this state no matter how consistently positive the GDP figures is for as long as it has gone on several times more damaging than back-to-back Great “Recessions.” As I have argued before, a second massive contraction would have been preferable if it at least corrected all these substandard standards and the loose application of terms with which they are always described.

The actual, visible trend in GDP is on the other hand absolutely clear, meaning highly inconsistent. We alternate between muddled quarters and bad ones, with an occasional decent number sprinkled in. And in those decent quarters, not really “good” by historical experience let alone symmetry, the upward bounce is extrapolated wildly and inappropriately into a future economy that has no chance of coming about. That should have been the lesson of 2013-14 (really 2011-12), where a cluster of decent quarters after the 2012 slowdown convinced economists and policymakers that a full recovery was not just possible but actually close at hand. If the economy had been as consistent, even modestly consistent, as it was described there would have been no Polar Vortex (which was a warning) nor the plethora of great contradictions (especially heavy reliance on a record inventory buildup predicated, I believe, on that mistaken commentary) like the distinct lack of income and wage growth. |

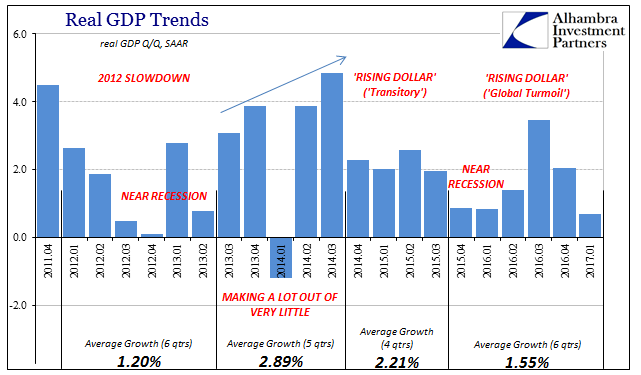

Real GDP Trends 2011-2017(see more posts on Gross Domestic Product, ) - Click to enlarge |

| The advance estimate for Q1 2017 (+0.6617%) was slightly better than the last forecast from the Atlanta Fed’s GDPNow tracking model (+0.2%), but close enough that it was still another washout. As of now, it is the worst quarterly growth rate since early 2014, a very fitting comparison. In those five quarters between the “taper tantrum” summer of 2013 and the first that included the initial “rising dollar” in 2014 (Q3), those that convinced economists that QE3 (and 4) was really working and the risks had shifted toward “overheating”, the average growth rate was still less than 3%.

Given the state of the economy to that point, having contracted so far during the Great “Recession” and then spent years failing to find symmetry, that period of inconsistent growth should have been recognized for being far, far short of the rhetoric. Given the circumstances, GDP should have averaged at least 5% if not more to both keep up with the unemployment rate as well as conform to actual recovery expectations. Again, what really happened was heavy dependence on extrapolations, where it was simply expected that growth would continue to gather pace and that by sometime in 2015 there would be an average of something ~5%, maybe ~4% at worst. |

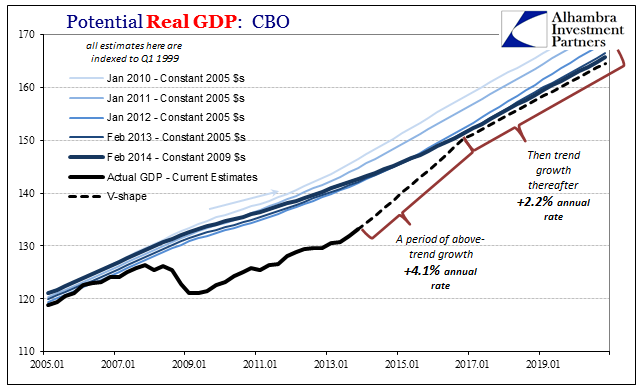

Potential Real GDP from 2005(see more posts on Gross Domestic Product, ) - Click to enlarge |

| That expectation, however, was based on the economy that “should be” rather than the one that existed and still exists. In fact, that has been a good part of the problem all along; the mainstream constantly refers to the conditions as they “should be” only to have them fail time and time again. After a while, as if seven years weren’t enough, you would think that they would finally see this for what it is – an economy that remains stuck in a very bad state. |

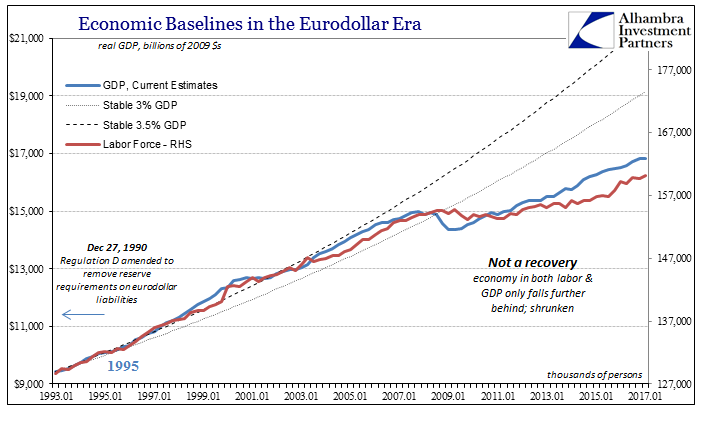

Economic Baselines In The Eurodollar Era 1993-2017 - Click to enlarge |

| Not only is it stuck, the costs of being this way are still rising. They can describe this in terms of “modest but consistent growth” but in truth the economy in non-linear terms continues to shrink; we (not just in the US) are much further behind today than at the trough of the Great “Recession”, which explains everything about the current state of affairs. Therefore, this is not the longest expansion in quite some time, it is instead the longest contraction since the 1930’s. That it is uneven are merely the details of how we go nowhere; one step forward, one step back and sometimes two.

It is the destructive curse of positive numbers. So long as there are plus signs, everything must be fantastic. GDP figures like everything else are subject to gradation; there is a vast difference between uneven low positives and truly steady modest growth. It has been ten years since the latter, and twenty since growth. This is not even expansion. |

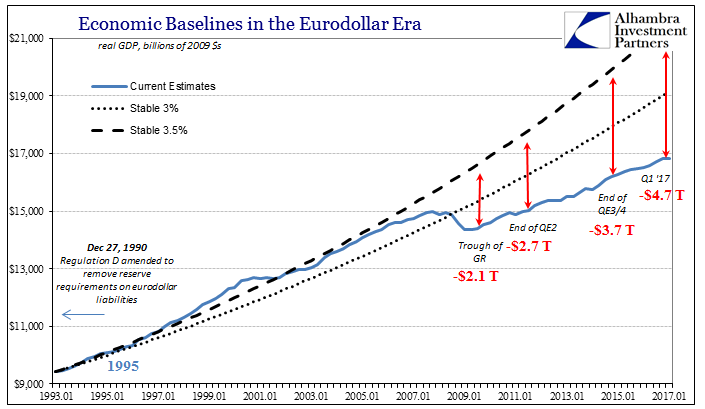

Economic Baselines In The Eurodollar Era 1993-2017 - Click to enlarge |

Tags: depression,dollar,dollar shortage,EuroDollar,eurodollar standard,GDP,global dollar short,Gross Domestic Product,Markets,money,newslettersent,real GDP