Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’21 Apr 2022

Weekly Market Pulse: Oil Shock

Weekly Market Pulse: Oil Shock8 Mar 2022

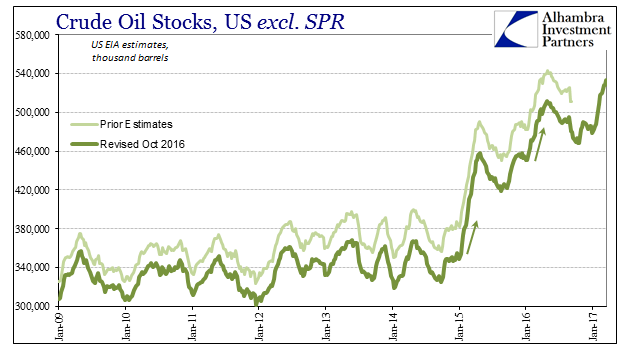

Houston, We Have An Oil (and inventory) Problem

Houston, We Have An Oil (and inventory) Problem7 Mar 2022

Short Run TIPS, LT Flat, Basically Awful Real(ity)

Short Run TIPS, LT Flat, Basically Awful Real(ity)28 Oct 2021

Perfect Time To Review What Is, And What Is Not, Inflation (and why it matters so much)

Perfect Time To Review What Is, And What Is Not, Inflation (and why it matters so much)13 Oct 2021

Weekly Market Pulse: Zooming Out

Weekly Market Pulse: Zooming Out3 Oct 2021

Inflation Hysteria #2 (WTI)

Inflation Hysteria #2 (WTI)12 Dec 2020

What’s Going On, And Why Late August?

What’s Going On, And Why Late August?29 Oct 2020

Inflation Karma

Inflation Karma15 Sep 2020

A Big One For The Big “D”

A Big One For The Big “D”13 May 2020

COT Black: No Love For Super-Secret Models

COT Black: No Love For Super-Secret Models1 May 2020

The Path Clear For More Rate Cuts, If You Like That Sort of Thing

The Path Clear For More Rate Cuts, If You Like That Sort of Thing15 Aug 2019

When Verizons Multiply, Macro In Inflation

When Verizons Multiply, Macro In Inflation16 Jun 2019

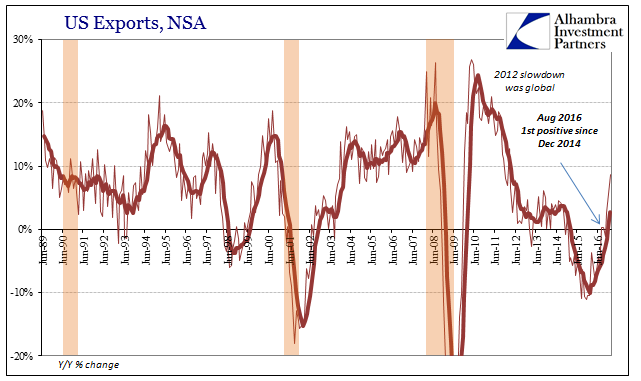

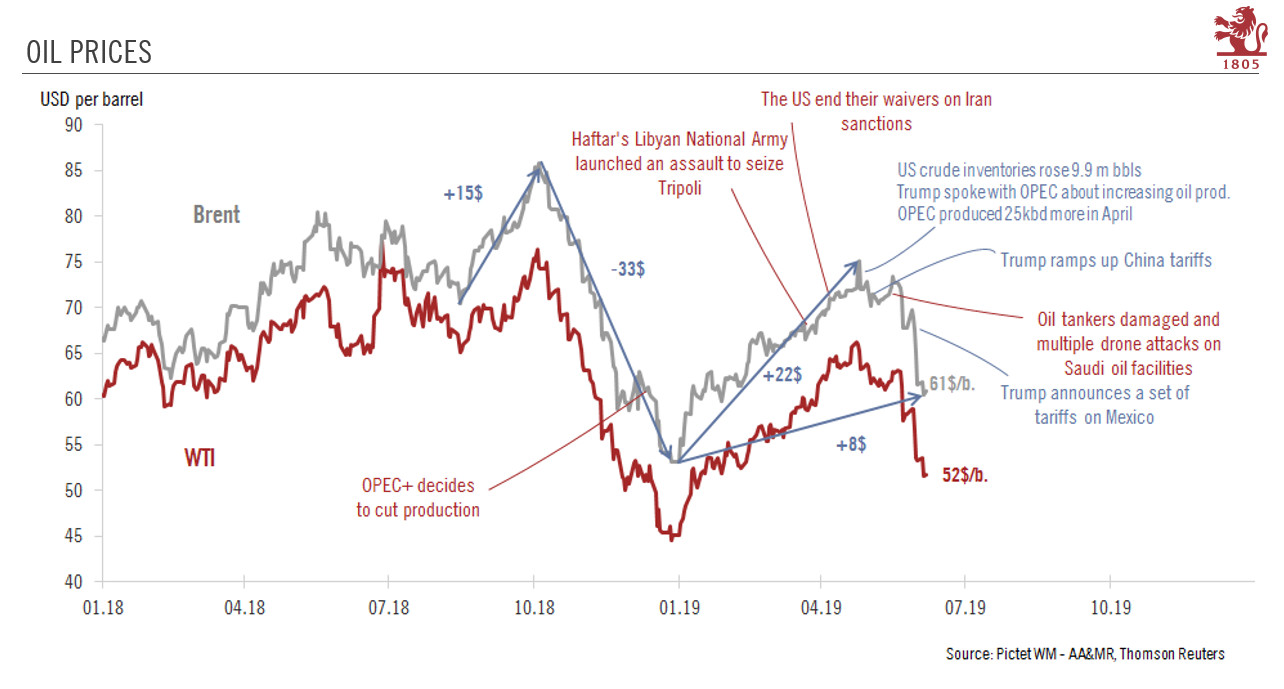

Oil prices are reeling

Oil prices are reeling11 Jun 2019

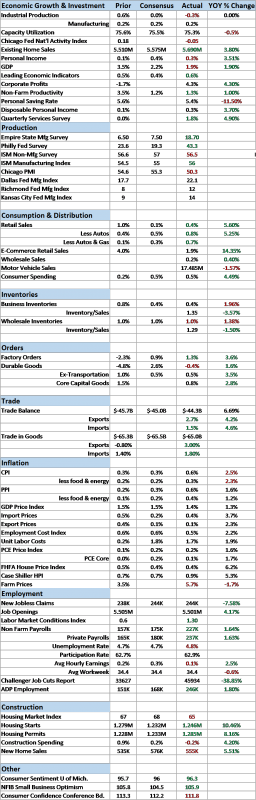

Green Shoot or Domestic Stall?

Green Shoot or Domestic Stall?17 Apr 2019

Oil prices supported by OPEC+ cuts…before market risks being flooded again

Oil prices supported by OPEC+ cuts…before market risks being flooded again5 Apr 2019

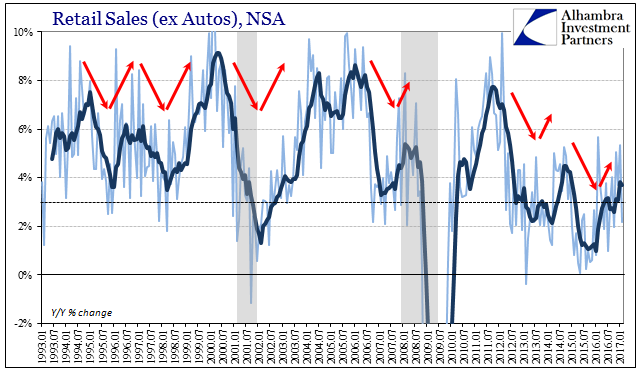

Retail Sales In Bad Company, Decouple from Decoupling

Retail Sales In Bad Company, Decouple from Decoupling4 Apr 2019

Downturn Rising, No ‘Glitch’ In Retail Sales

Downturn Rising, No ‘Glitch’ In Retail Sales13 Mar 2019

Inflation Falls Again, Dot-com-like

Inflation Falls Again, Dot-com-like16 Feb 2019

Wasting the Middle: Obsessing Over Exits

Wasting the Middle: Obsessing Over Exits28 Dec 2018