Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: There Is No Certainty In Investing

Weekly Market Pulse: There Is No Certainty In Investing18 Jul 2022

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.6 Jun 2022

Synchronized Not Coronavirus

Synchronized Not Coronavirus19 May 2022

Industrial Synchronized Demand

Industrial Synchronized Demand11 May 2022

Euro$ #5 in Goods

Euro$ #5 in Goods27 Apr 2022

Shanghai’s Current Plight Began in 2017

Shanghai’s Current Plight Began in 201723 Apr 2022

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’21 Apr 2022

White-Hot Cycles of Silence

White-Hot Cycles of Silence28 Dec 2021

The ‘Growth Scare’ Keeps Growing Out Of The Macro (Money) Illusion

The ‘Growth Scare’ Keeps Growing Out Of The Macro (Money) Illusion26 Nov 2021

The Enormously Important Reasons To Revisit The Revisions Already Several Times Revisited

The Enormously Important Reasons To Revisit The Revisions Already Several Times Revisited29 Oct 2021

Far Longer And Deeper Than Just The Past Few Months

Far Longer And Deeper Than Just The Past Few Months20 Oct 2021

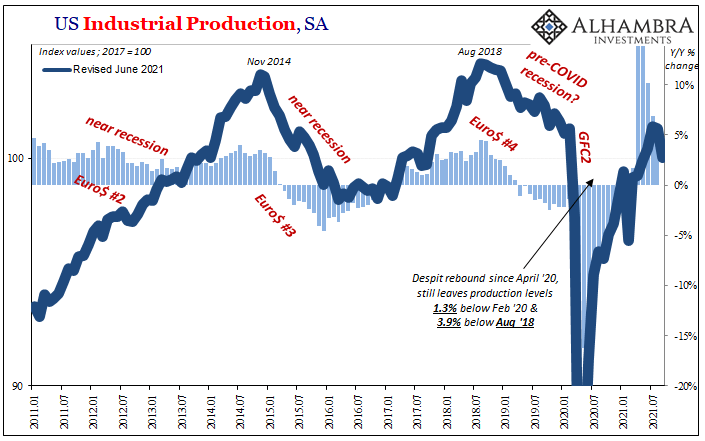

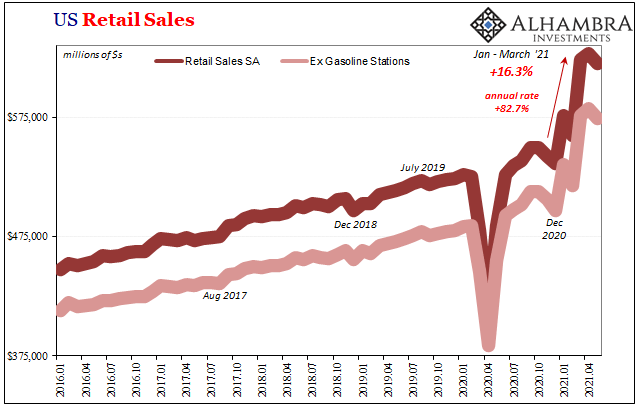

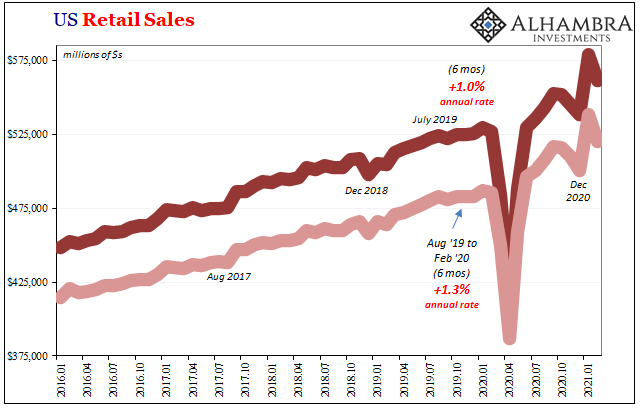

Another Round of Transitory: US Retail Sales & (revised) IP

Another Round of Transitory: US Retail Sales & (revised) IP16 Jun 2021

Spending Here, Production There, and What Autos Have To Do With It

Spending Here, Production There, and What Autos Have To Do With It17 Mar 2021

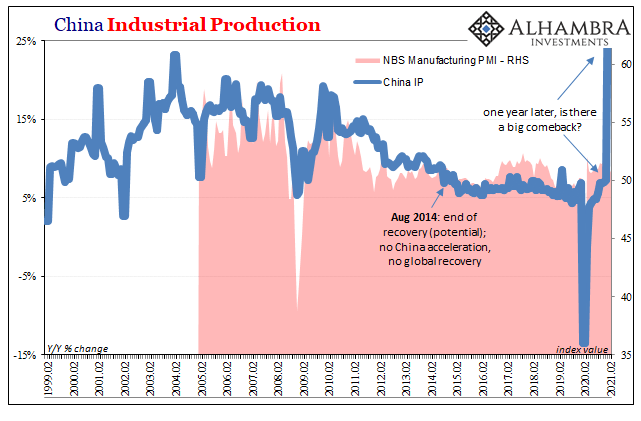

Looking Past Gigantic Base Effects To China’s (Really) Struggling Economy

Looking Past Gigantic Base Effects To China’s (Really) Struggling Economy16 Mar 2021

Consumers, Producers, and the Unsettled End of 2020

Consumers, Producers, and the Unsettled End of 202017 Jan 2021

Seizing The Dirt Shirt Title

Seizing The Dirt Shirt Title6 Jan 2021

What Did Hamper Growth ‘In A Few Months’

What Did Hamper Growth ‘In A Few Months’18 Dec 2020

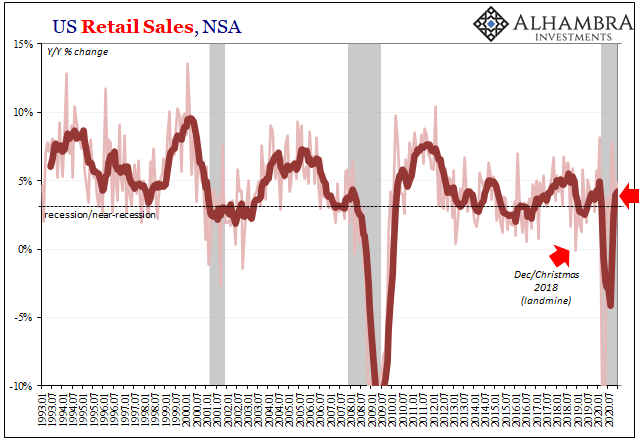

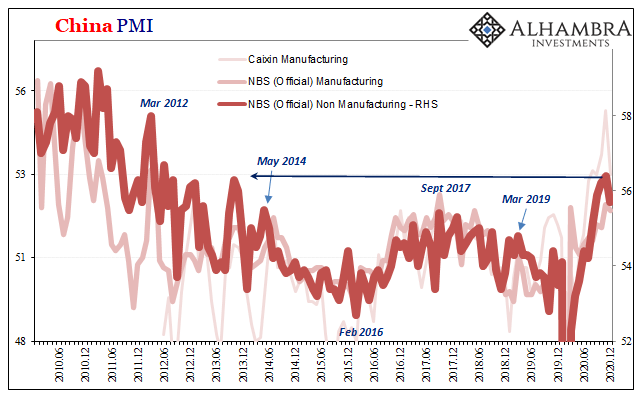

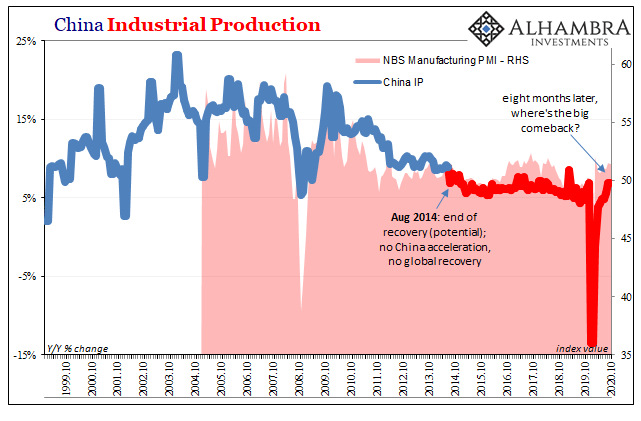

This Global Growth Stuff, China Still Wants A Word

This Global Growth Stuff, China Still Wants A Word16 Dec 2020

Extending the Summer Slowdown

Extending the Summer Slowdown20 Nov 2020

Six Point Nine Times Two Equals What It Had In Twenty Fourteen

Six Point Nine Times Two Equals What It Had In Twenty Fourteen17 Nov 2020