Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

What Did Hamper Growth ‘In A Few Months’

What Did Hamper Growth ‘In A Few Months’18 Dec 2020

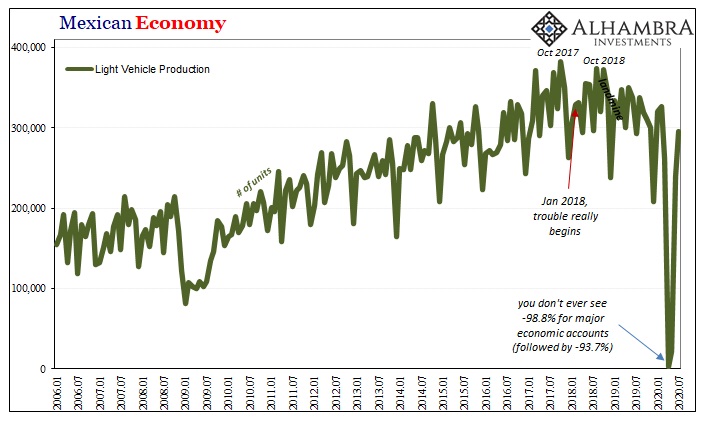

Meaning Mexico25 Aug 2020

The Real Diseased Body12 Apr 2020

Stagnation Never Looked So Good: A Peak Ahead21 Mar 2020

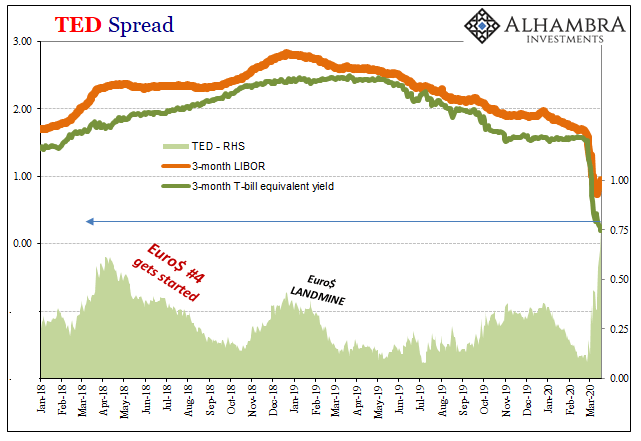

Is GFC2 Over?18 Mar 2020

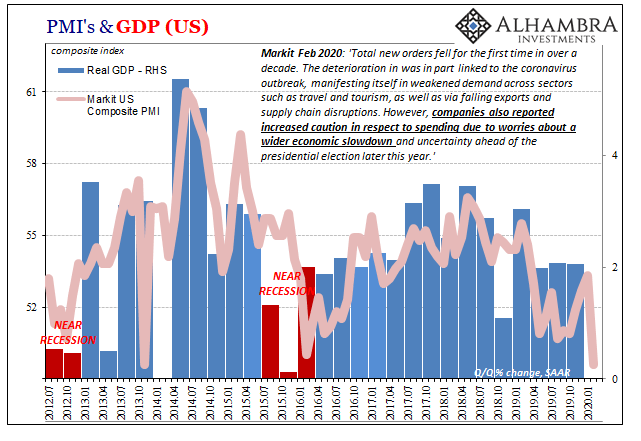

Take Your Pick of PMI’s Today, But It’s Not Really An Either/Or6 Mar 2020

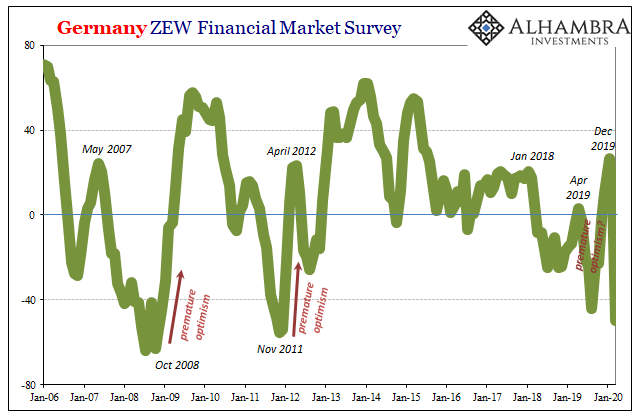

Schaetze To That26 Feb 2020

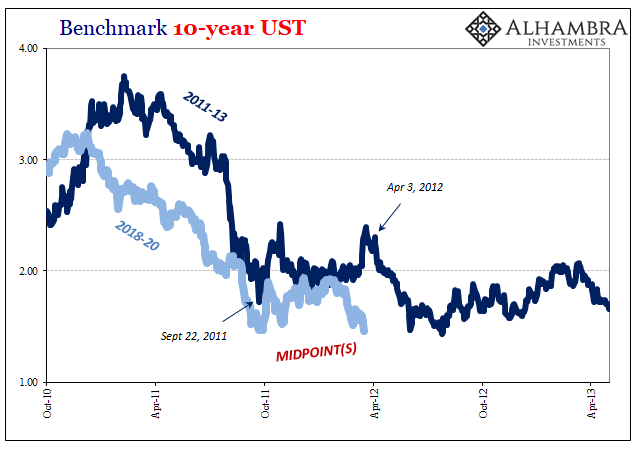

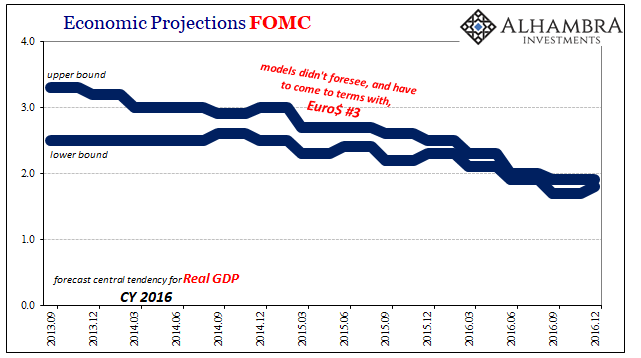

Was It A Midpoint And Did We Already Pass Through It?25 Feb 2020

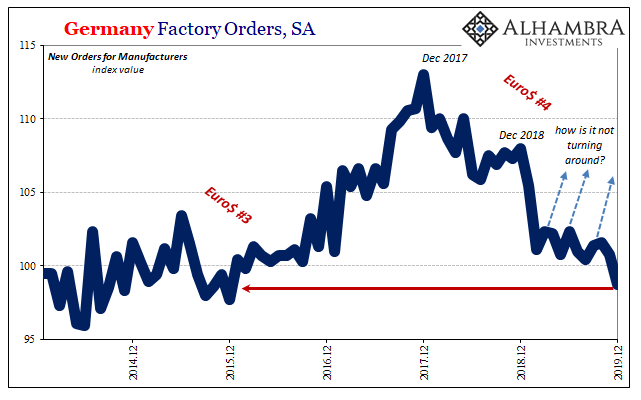

European Data: Much More In Store For Number Four18 Feb 2020

COT Black: German Factories, Oklahoma Tank Farms, And FRBNY9 Feb 2020

The FOMC Channels China’s Xi As To Japan Going Global13 Dec 2019

China’s Financial Stability: A Squeeze and a Strangle27 Nov 2019

Why The Japanese Are Suddenly Messing With YCC6 Oct 2019

Stuck at A: Repo Chaos Isn’t Something New, It’s The Same Baseline17 Sep 2019

A Bigger Boat11 Sep 2019

Globally Synchronized, After All20 Jul 2019

Japan’s Bellwether On Nasty #425 Jun 2019

Europe Comes Apart, And That’s Before #430 May 2019

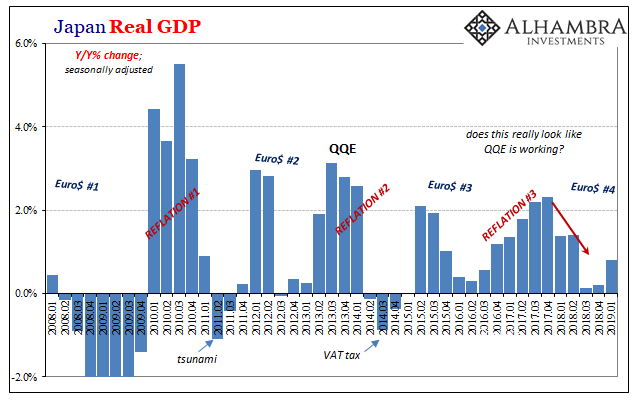

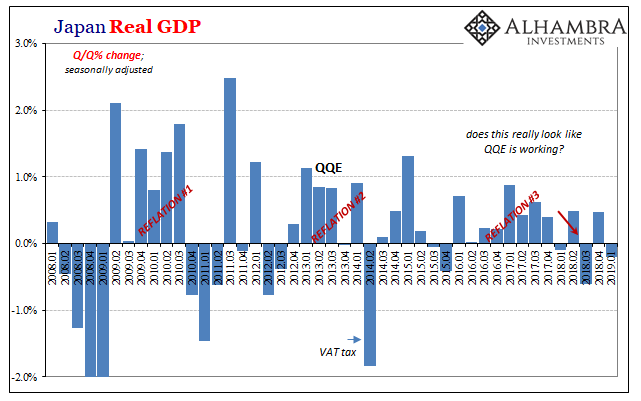

Japan’s Surprise Positive Is A Huge Minus21 May 2019

Effective Recession First In Japan?16 May 2019