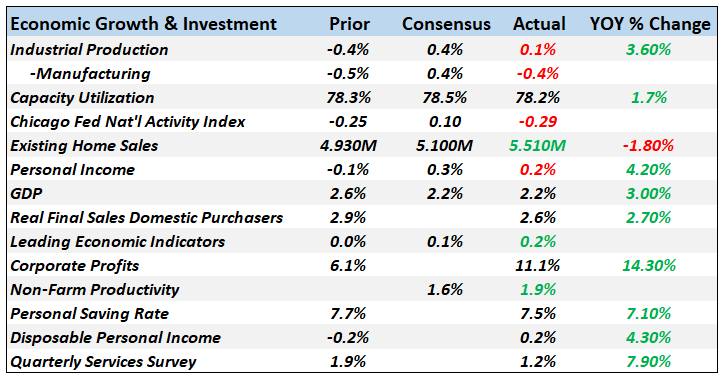

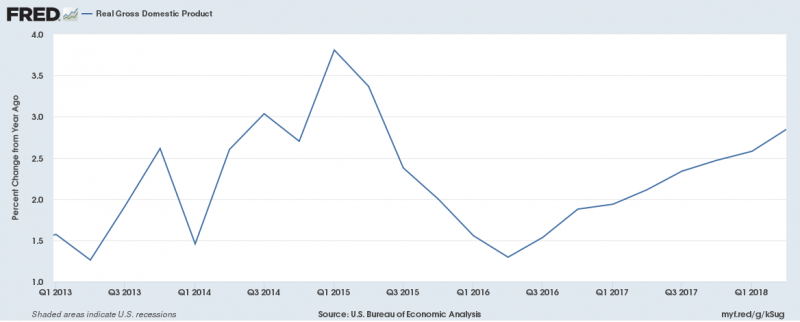

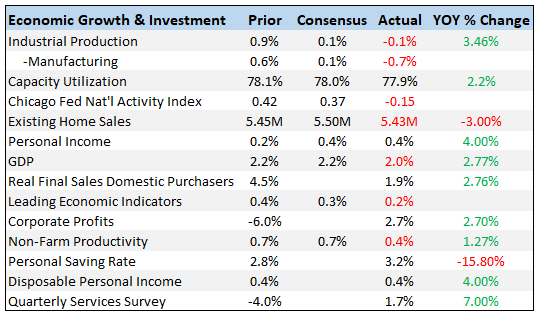

Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

No, Chicken Little, the Sky is Not Falling

No, Chicken Little, the Sky is Not Falling9 Aug 2024

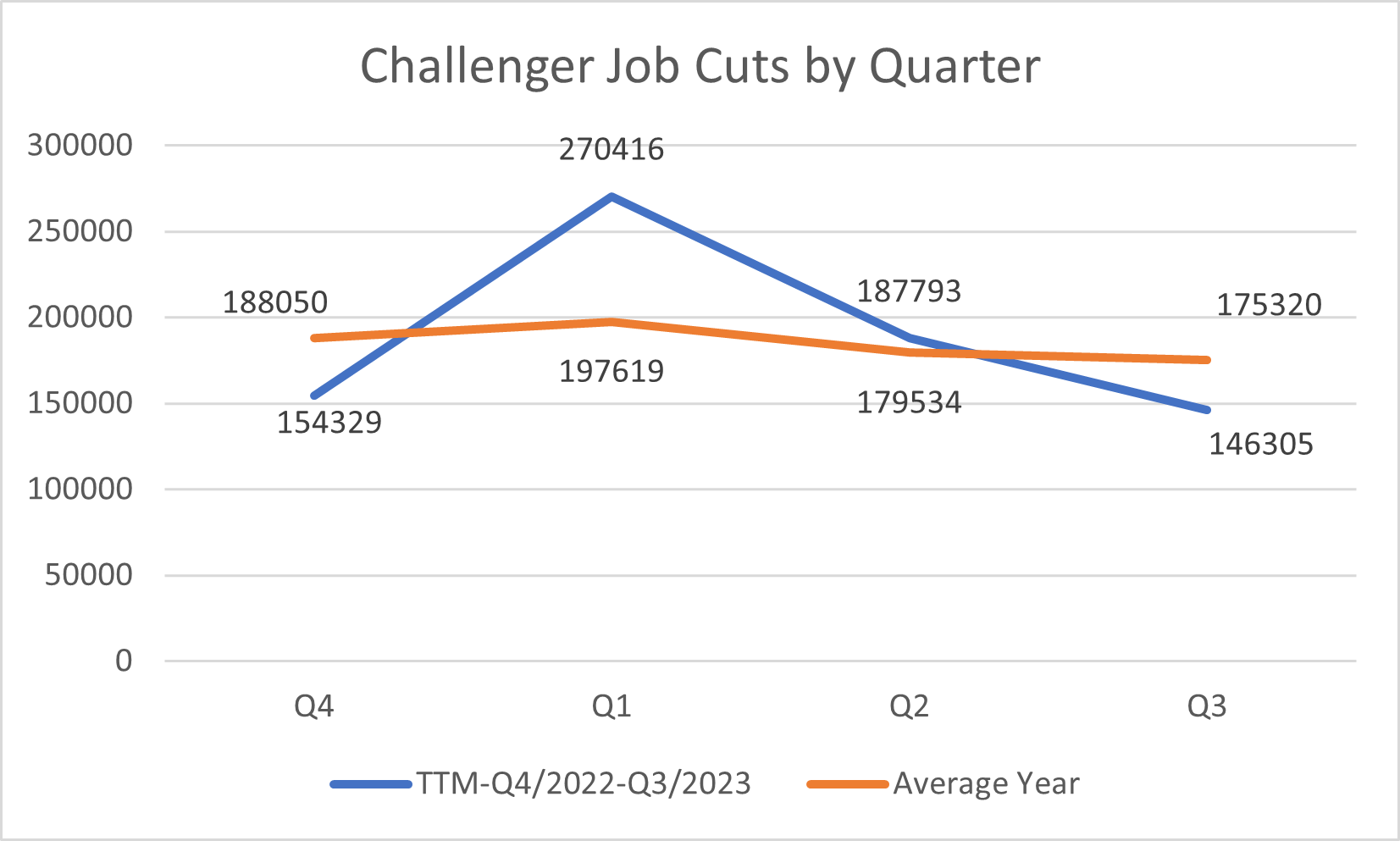

Macro: Challenger Job Cuts — Improvement throughout the year

Macro: Challenger Job Cuts — Improvement throughout the year2 Nov 2023

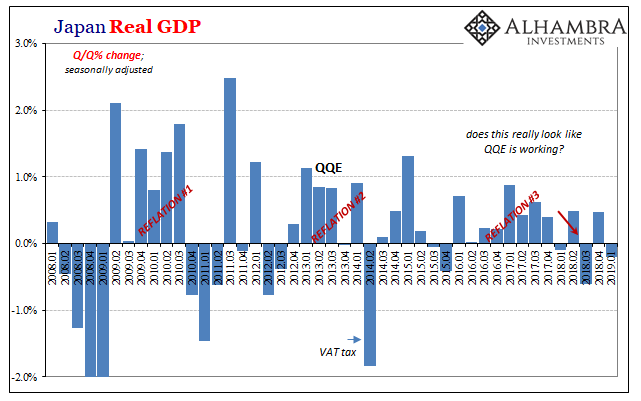

Surprise-Packed Tuesday: China Cut Rates, Japan’s Q2 GDP Rises Twice as Fast as Expected, and UK Wages Accelerate

Surprise-Packed Tuesday: China Cut Rates, Japan’s Q2 GDP Rises Twice as Fast as Expected, and UK Wages Accelerate15 Aug 2023

Simple Economics and Money Math

Simple Economics and Money Math12 Jun 2022

May Payrolls (and more) Confirm Slowdown (and more)7 Jun 2022

ADP Front-Runs BLS and President Phillips

ADP Front-Runs BLS and President Phillips4 Jun 2022

President Phillips Emerges To Reassure On Growing Slowdown

President Phillips Emerges To Reassure On Growing Slowdown2 Jun 2022

Neither Confusing Nor Surprising: Q1’s Worst Productivity Ever, April Decline In Employed

Neither Confusing Nor Surprising: Q1’s Worst Productivity Ever, April Decline In Employed13 May 2022

A Global JOLT(s) In July

A Global JOLT(s) In July9 Dec 2021

The Productive Use Of Awful Q3 Productivity Estimates Highlights Even More ‘Growth Scare’ Potential

The Productive Use Of Awful Q3 Productivity Estimates Highlights Even More ‘Growth Scare’ Potential8 Dec 2021

Weekly Market Pulse: Inflation Scare!

Weekly Market Pulse: Inflation Scare!25 Oct 2021

Weekly Market Pulse: Perception vs Reality

Weekly Market Pulse: Perception vs Reality18 Oct 2021

For The Love Of Unemployment Rates

For The Love Of Unemployment Rates12 Oct 2021

Weekly Market Pulse: Inflation Scare?

Weekly Market Pulse: Inflation Scare?11 Oct 2021

Weekly Market Pulse: Time For A Taper Tantrum?

Weekly Market Pulse: Time For A Taper Tantrum?20 Sep 2021

Do Rising ‘Global’ Growth Concerns Include An Already *Slowing* US Economy?

Do Rising ‘Global’ Growth Concerns Include An Already *Slowing* US Economy?23 Jul 2021

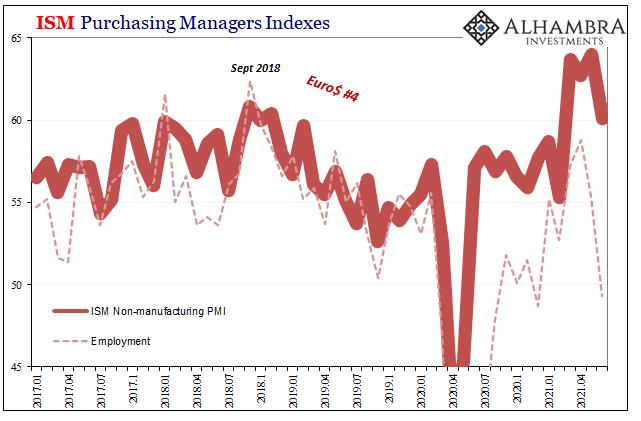

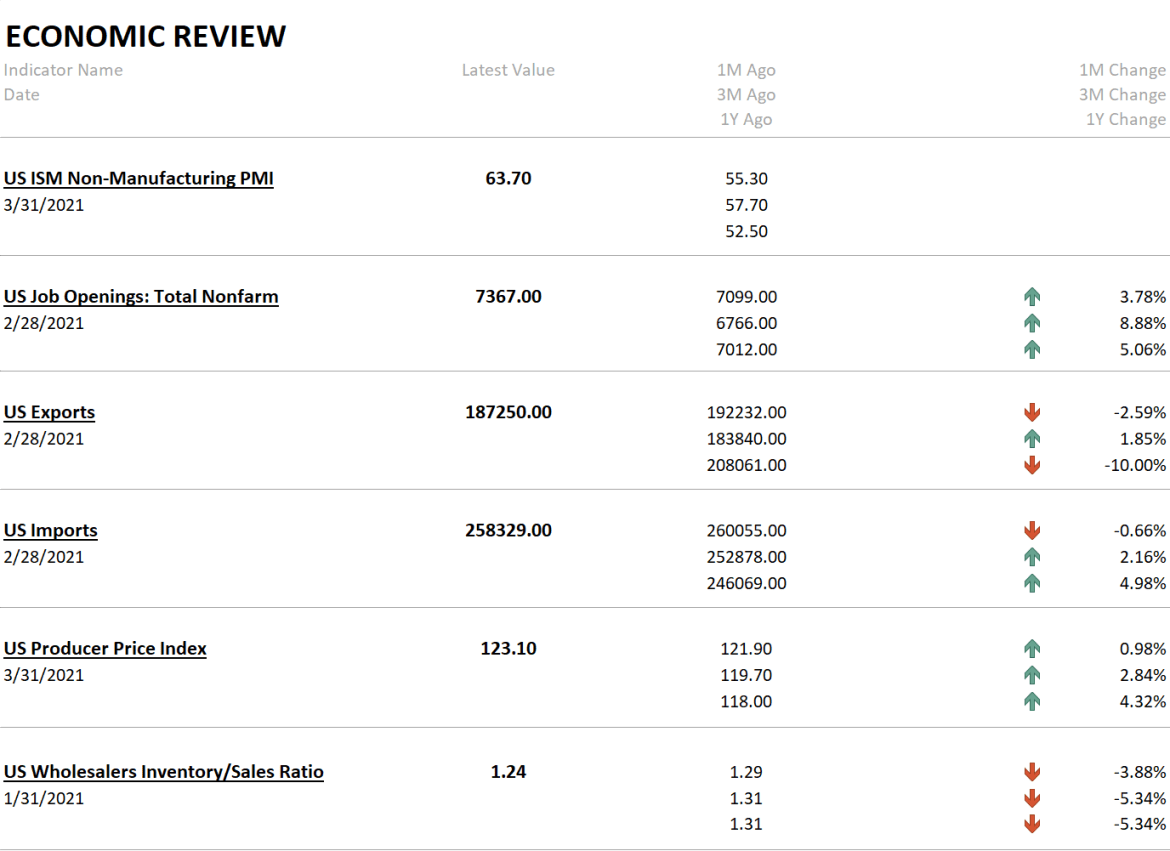

ISM’s Nasty Little Surprise Isn’t Actually A Surprise

ISM’s Nasty Little Surprise Isn’t Actually A Surprise7 Jul 2021

Weekly Market Pulse: Nothing To See Here. No, Really. Nothing.

Weekly Market Pulse: Nothing To See Here. No, Really. Nothing.12 Apr 2021

Weekly Market Pulse – Real Rates Finally Make A Move

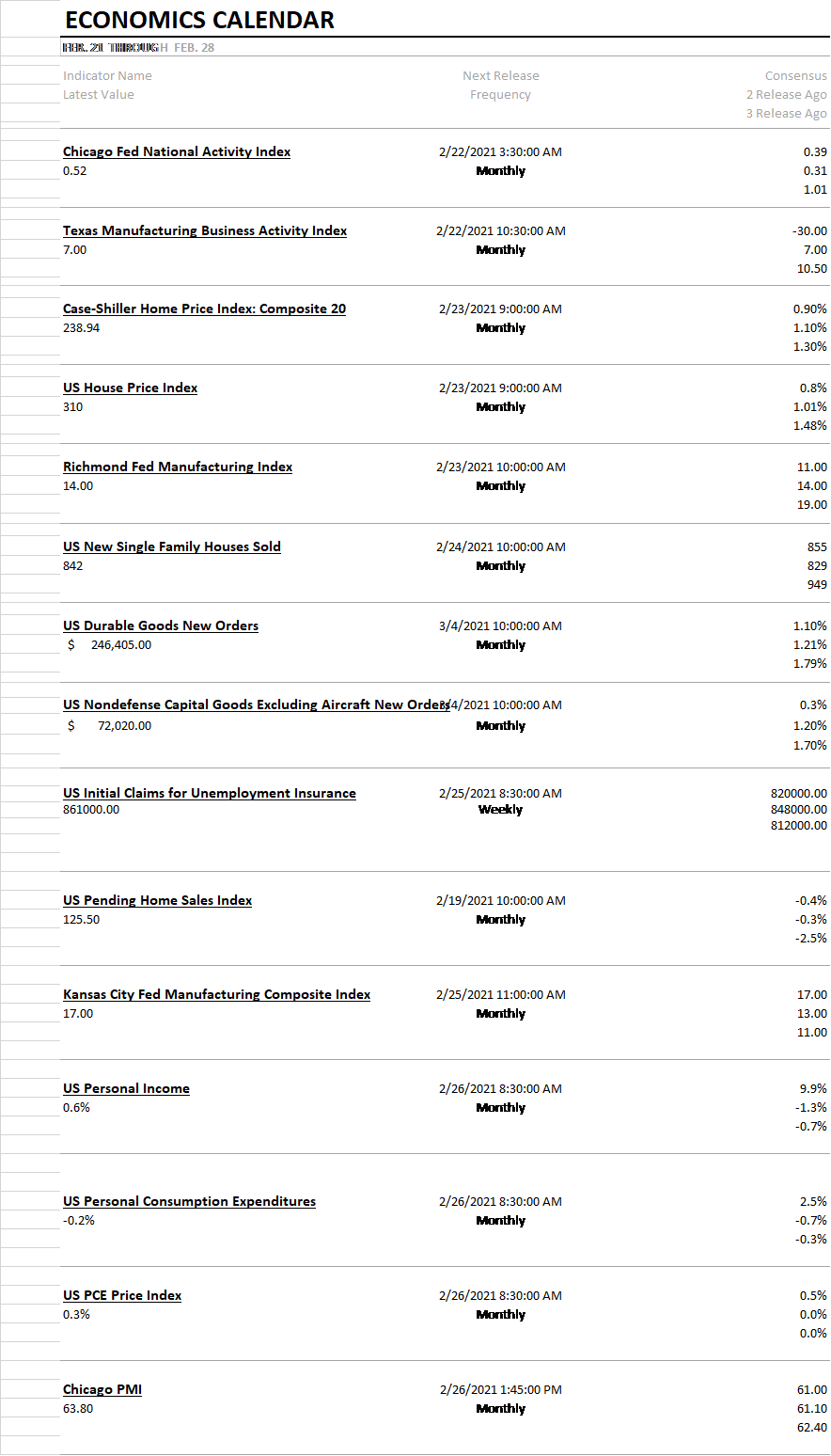

Weekly Market Pulse – Real Rates Finally Make A Move22 Feb 2021

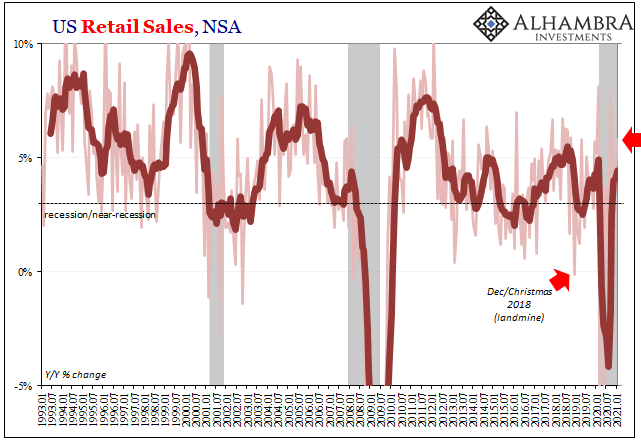

Uncle Sam Was Back Having Consumers’ Backs

Uncle Sam Was Back Having Consumers’ Backs18 Feb 2021