Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Simple Economics and Money Math

Simple Economics and Money Math12 Jun 2022

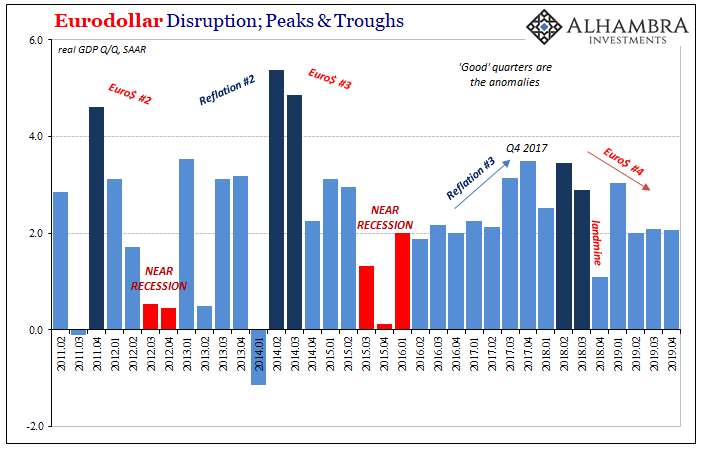

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.6 Jun 2022

T-bills Targeted Target

T-bills Targeted Target20 May 2022

Is It Recession?

Is It Recession?30 Apr 2022

Not Good Goods

Not Good Goods24 Apr 2022

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data29 Jan 2022

Trying To Project The Goods Trade Cycle

Trying To Project The Goods Trade Cycle17 Dec 2021

A Global JOLT(s) In July

A Global JOLT(s) In July9 Dec 2021

August Retail Sales Surprise To The Upside, Because They Were Down?

August Retail Sales Surprise To The Upside, Because They Were Down?17 Sep 2021

Inflation Isn’t Just The Outlier, The Inflation In It Is, Too

Inflation Isn’t Just The Outlier, The Inflation In It Is, Too29 Jun 2021

Spending Here, Production There, and What Autos Have To Do With It

Spending Here, Production There, and What Autos Have To Do With It17 Mar 2021

Uncle Sam Was Back Having Consumers’ Backs

Uncle Sam Was Back Having Consumers’ Backs18 Feb 2021

Consumers, Producers, and the Unsettled End of 2020

Consumers, Producers, and the Unsettled End of 202017 Jan 2021

Consumers, Too; (Un)Confident To Re-engage

Consumers, Too; (Un)Confident To Re-engage19 Dec 2020

Extending the Summer Slowdown

Extending the Summer Slowdown20 Nov 2020

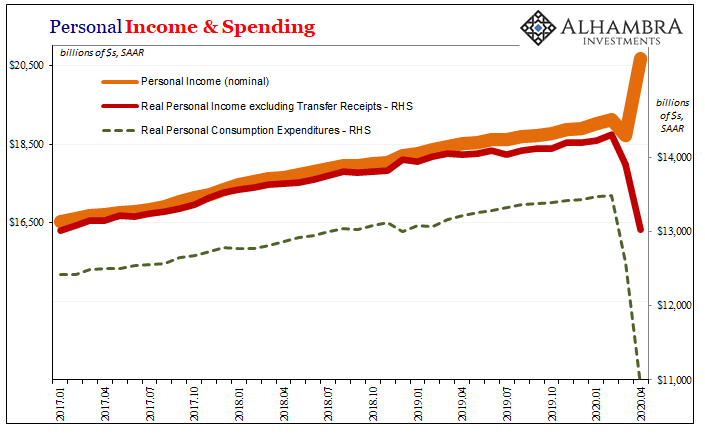

Personal Income and Spending: The Other Side

Personal Income and Spending: The Other Side1 Jun 2020

We All Know Who’s On First, But What’s On Second?

We All Know Who’s On First, But What’s On Second?8 May 2020

US Sales and Production Remain Virus-Free, But Still Aren’t Headwind-Free

US Sales and Production Remain Virus-Free, But Still Aren’t Headwind-Free18 Feb 2020

Three Straight Quarters of 2 percent, And Yet Each One Very Different

Three Straight Quarters of 2 percent, And Yet Each One Very Different2 Feb 2020

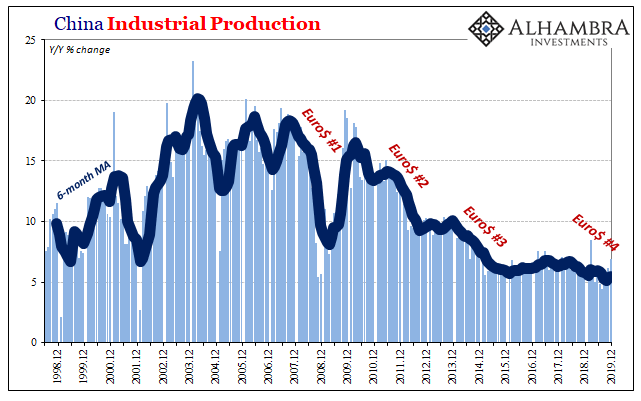

China Enters 2020 Still (Intent On) Managing Its Decline

China Enters 2020 Still (Intent On) Managing Its Decline21 Jan 2020