Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

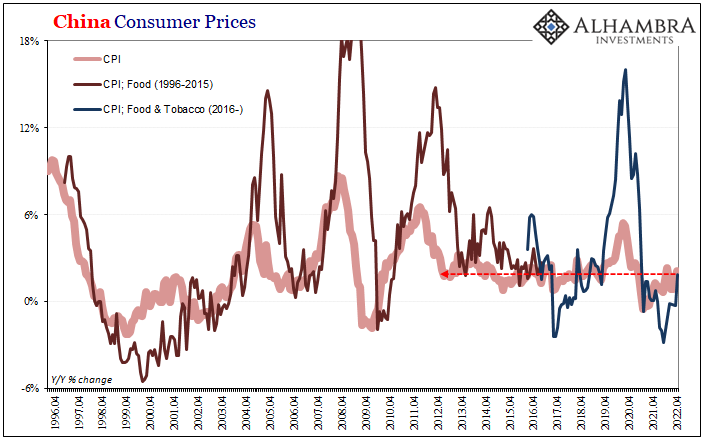

Curve Inversion 101: US CPI Politics Up Front, China PPI Down(ing) The Back

Curve Inversion 101: US CPI Politics Up Front, China PPI Down(ing) The Back16 Jun 2022

Prices As Curative Punishment

Prices As Curative Punishment14 Jun 2022

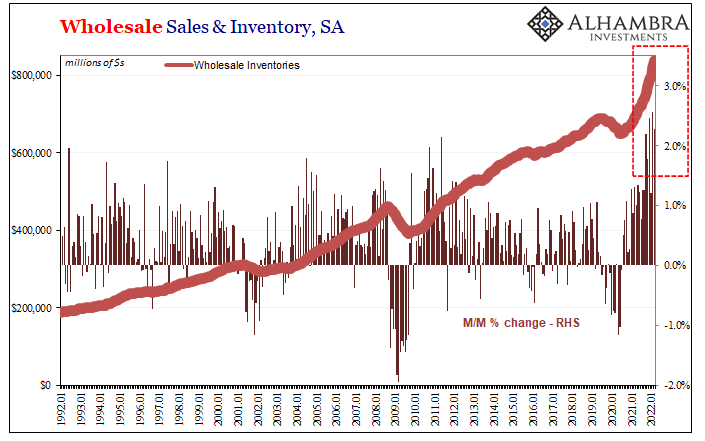

“Inflation” Not Inflation, Through The Eyes of Inventory

“Inflation” Not Inflation, Through The Eyes of Inventory11 Jun 2022

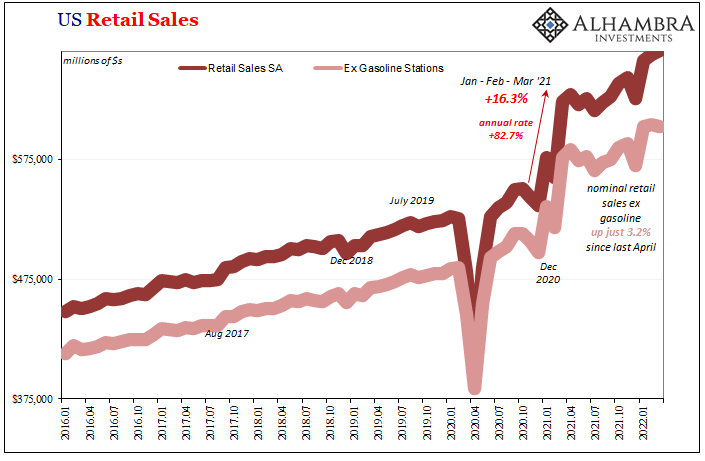

Shipping Around Retail ‘Inflation’

Shipping Around Retail ‘Inflation’22 May 2022

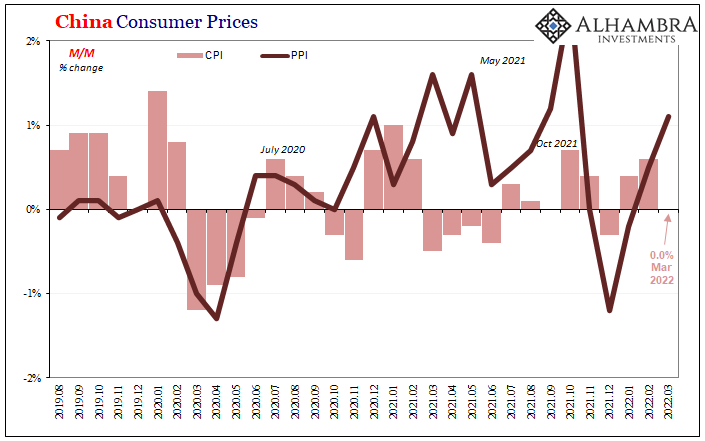

Synchronizing Chinese Prices (and consequences)

Synchronizing Chinese Prices (and consequences)14 May 2022

Who’s Playing Puppetmaster, And Who Is Master of Puppets

Who’s Playing Puppetmaster, And Who Is Master of Puppets9 May 2022

Historic Inventory Continued In March, But Is It All Price Illusion, Too?

Historic Inventory Continued In March, But Is It All Price Illusion, Too?28 Apr 2022

Not Good Goods

Not Good Goods24 Apr 2022

China More and More Beyond ‘Inflation’

China More and More Beyond ‘Inflation’17 Apr 2022

You Know What They Say About The Light At The End Of The Tunnel

You Know What They Say About The Light At The End Of The Tunnel14 Apr 2022

US CPI Reaches Seven On US Goods Prices, With Disinflation Setting In Everywhere Else (incl. US Services)

US CPI Reaches Seven On US Goods Prices, With Disinflation Setting In Everywhere Else (incl. US Services)16 Jan 2022

Testing The Supply Chain Inflation Hypothesis The Real Money Way

Testing The Supply Chain Inflation Hypothesis The Real Money Way18 Dec 2021

Perfect Time To Review What Is, And What Is Not, Inflation (and why it matters so much)

Perfect Time To Review What Is, And What Is Not, Inflation (and why it matters so much)13 Oct 2021

Inflation Isn’t Just The Outlier, The Inflation In It Is, Too

Inflation Isn’t Just The Outlier, The Inflation In It Is, Too29 Jun 2021

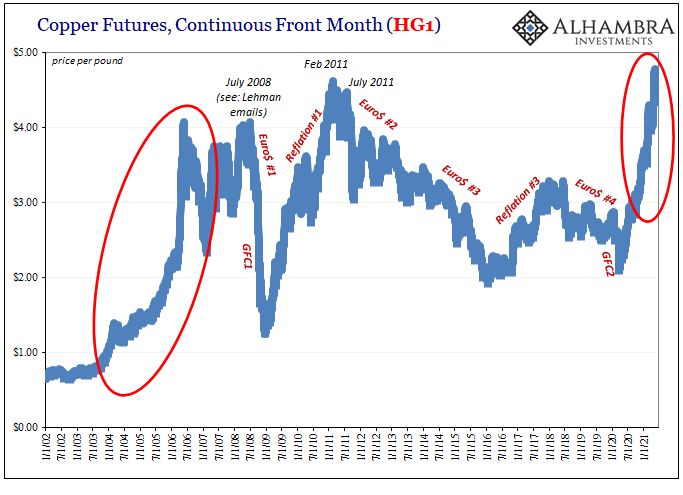

Copper Corroding PPI

Copper Corroding PPI17 Jun 2021

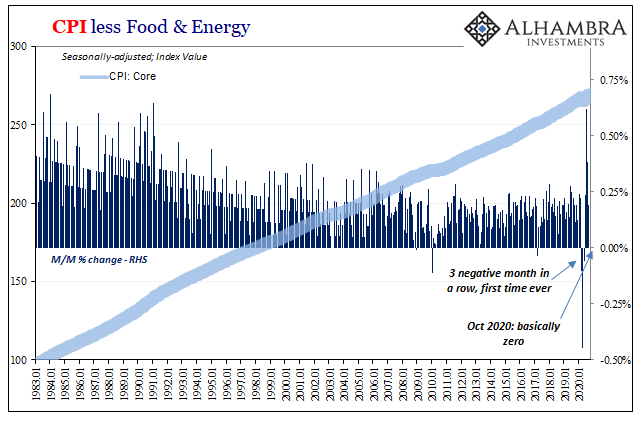

If the Fed’s Not In Consumer Prices, Then How About Producer Prices?

If the Fed’s Not In Consumer Prices, Then How About Producer Prices?16 Jan 2021

Where Is It, Chairman Powell?

Where Is It, Chairman Powell?15 Nov 2020

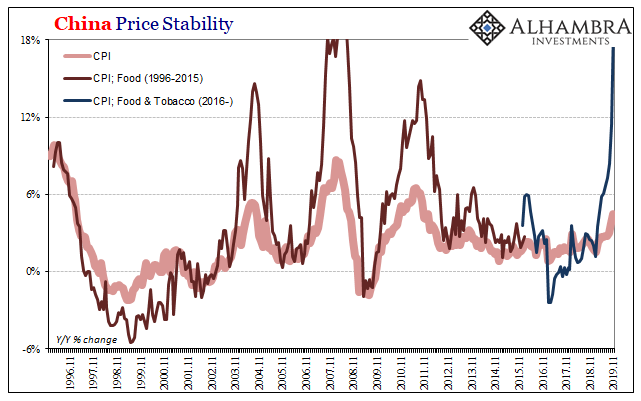

The Prices And Costs Of What Xi Believes He’s Got To Do

The Prices And Costs Of What Xi Believes He’s Got To Do12 Nov 2020

Transitory, The Other Way

Transitory, The Other Way18 Jul 2020

If Trade Wars Couldn’t, Might Pig Wars Change Xi’s Mind?

If Trade Wars Couldn’t, Might Pig Wars Change Xi’s Mind?12 Dec 2019