Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

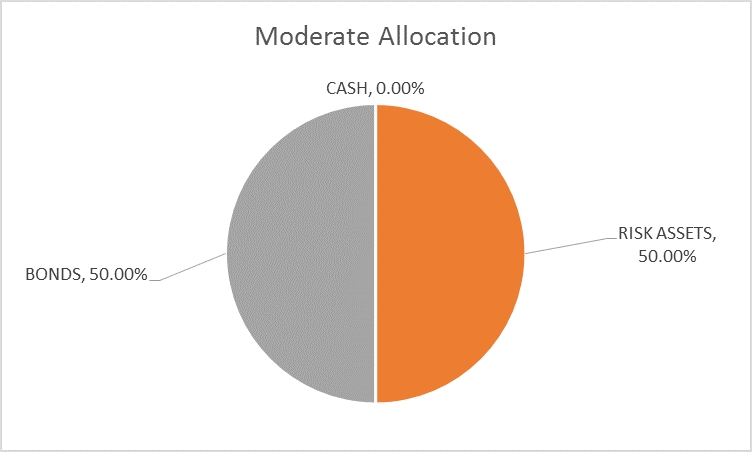

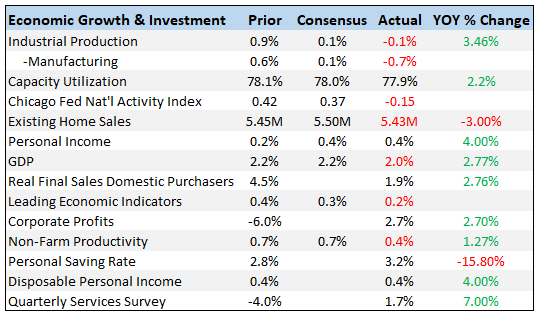

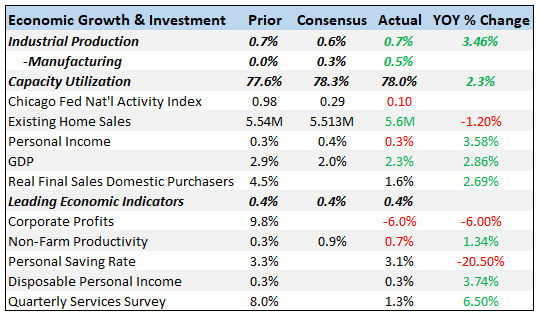

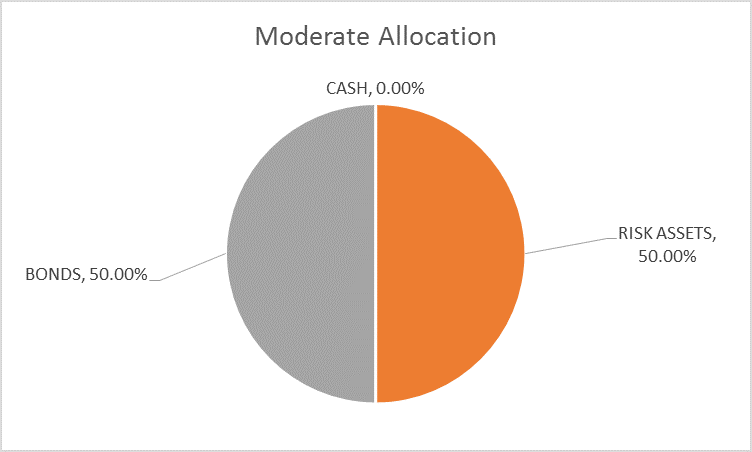

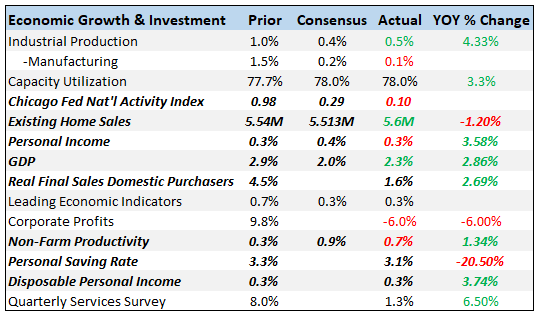

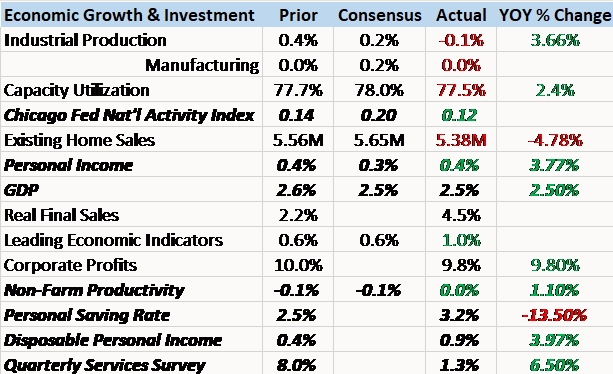

Monthly Macro Monitor: A Lot Of Noise, Little Effect

Monthly Macro Monitor: A Lot Of Noise, Little Effect27 Apr 2026

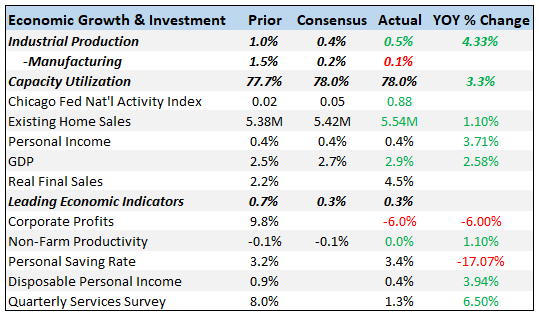

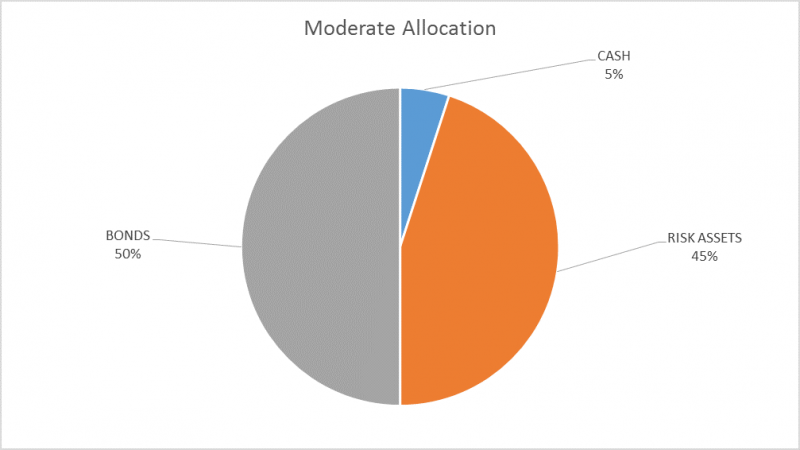

Investor Dilemma: Pavlov Rings The Bell – Draft

Investor Dilemma: Pavlov Rings The Bell – Draft3 Nov 2025

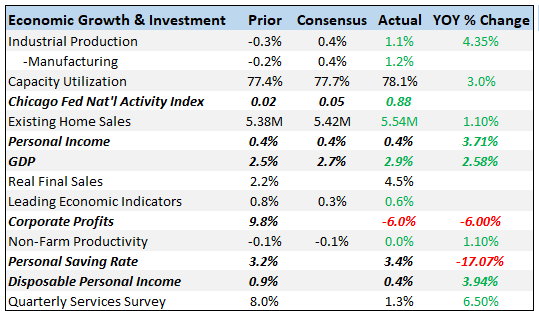

Weekly Market Pulse: An Energetic Market

Weekly Market Pulse: An Energetic Market18 Sep 2025

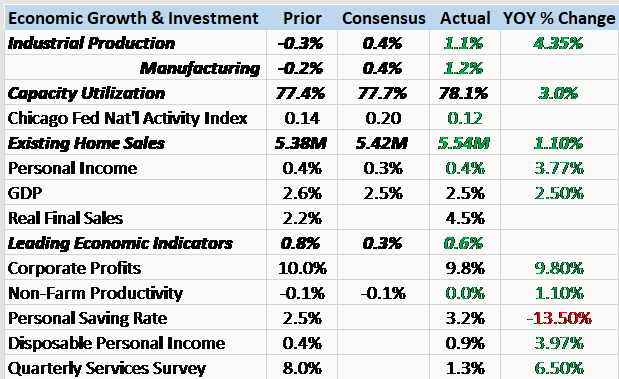

Invest Or Index – Exploring 5-Different Strategies

Invest Or Index – Exploring 5-Different Strategies15 Sep 2025

Weekly Market Pulse: Big Rate Cuts? Not Right Now

Weekly Market Pulse: Big Rate Cuts? Not Right Now18 Aug 2025

Weekly Market Pulse: The Turkey Leg

Weekly Market Pulse: The Turkey Leg23 Jun 2025

Weekly Market Pulse: No Free Lunches

Weekly Market Pulse: No Free Lunches19 May 2025

Weekly Market Pulse: On The Road Again

Weekly Market Pulse: On The Road Again12 May 2025

Weekly Market Pulse: Peak America?

Weekly Market Pulse: Peak America?21 Apr 2025

Weekly Market Pulse: Tune Out The Noise

Weekly Market Pulse: Tune Out The Noise24 Feb 2025

Weekly Market Pulse: Questions

Weekly Market Pulse: Questions14 Oct 2024

Weekly Market Pulse: Did The Fed Just Make A Mistake?

Weekly Market Pulse: Did The Fed Just Make A Mistake?23 Sep 2024

S&P 500 – A Bullish And Bearish Analysis

S&P 500 – A Bullish And Bearish Analysis10 Sep 2024

Technological Advances Make Things Better – Or Does It?6 Sep 2024

Risks Facing Bullish Investors As September Begins

Risks Facing Bullish Investors As September Begins3 Sep 2024

Weekly Market Pulse: It’s An Uncertain World

Weekly Market Pulse: It’s An Uncertain World3 Sep 2024

Japanese Style Policies And The Future Of America

Japanese Style Policies And The Future Of America30 Aug 2024

Red Flags In The Latest Retail Sales Report

Red Flags In The Latest Retail Sales Report23 Aug 2024

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?15 Apr 2024

Weekly Market Pulse: Monetary Policy Is Hard

Weekly Market Pulse: Monetary Policy Is Hard6 Nov 2023