Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Sex, Money and Demographics

Sex, Money and Demographics27 Apr 2026

Monthly Macro Monitor: A Lot Of Noise, Little Effect

Monthly Macro Monitor: A Lot Of Noise, Little Effect27 Apr 2026

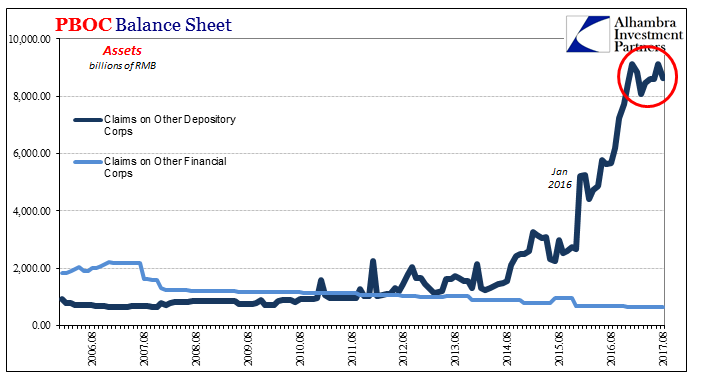

Mercantilism: China and Beyond

Mercantilism: China and Beyond25 Apr 2026

Weekly Market Pulse: The Only Free Lunch In Investing

Weekly Market Pulse: The Only Free Lunch In Investing13 Apr 2026

I’ll Turn Bullish When This Happens

I’ll Turn Bullish When This Happens13 Apr 2026

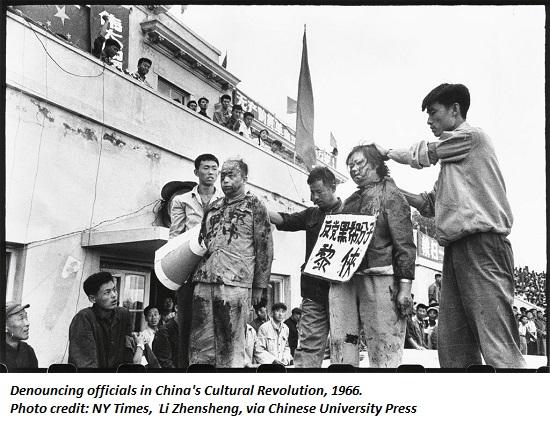

Lessons from China’s Cultural Revolution

Lessons from China’s Cultural Revolution21 Jan 2026

Weekly Market Pulse: An Energetic Market

Weekly Market Pulse: An Energetic Market18 Sep 2025

Weekly Market Pulse: Big Rate Cuts? Not Right Now

Weekly Market Pulse: Big Rate Cuts? Not Right Now18 Aug 2025

AI for Dummies: AI Turns Us Into Dummies

AI for Dummies: AI Turns Us Into Dummies30 Jul 2025

Hollowed Out

Hollowed Out26 Jun 2025

Meta-Thoughts on the War

Meta-Thoughts on the War23 Jun 2025

Weekly Market Pulse: The Turkey Leg

Weekly Market Pulse: The Turkey Leg23 Jun 2025

Weekly Market Pulse: No Free Lunches

Weekly Market Pulse: No Free Lunches19 May 2025

Living on Meds, Vitamin C and Ibogaine: American Precarity

Living on Meds, Vitamin C and Ibogaine: American Precarity14 May 2025

The One Real Economic Indicator: "Upgrade to Premium"

The One Real Economic Indicator: "Upgrade to Premium"12 May 2025

Weekly Market Pulse: On The Road Again

Weekly Market Pulse: On The Road Again12 May 2025

Tariffs Are Not Enough

Tariffs Are Not Enough8 May 2025

The Terminal Rot in Corporate America

The Terminal Rot in Corporate America5 May 2025

The Wile E. Coyote Recession

The Wile E. Coyote Recession24 Apr 2025

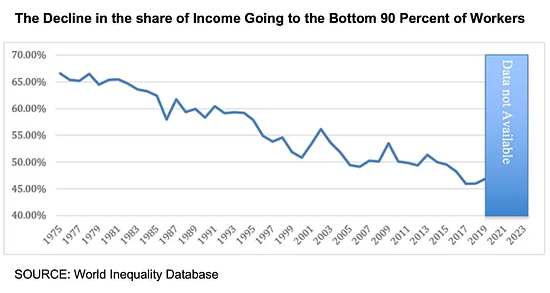

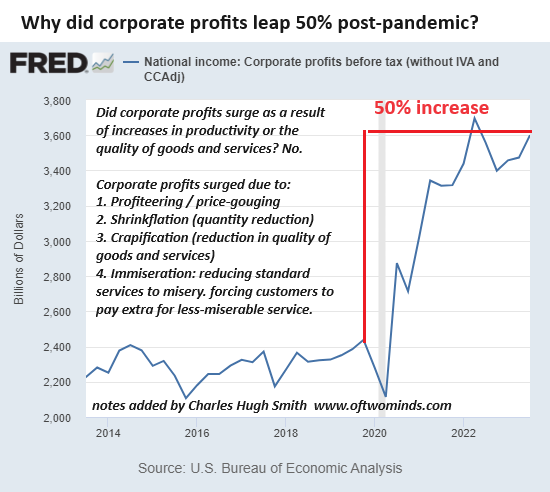

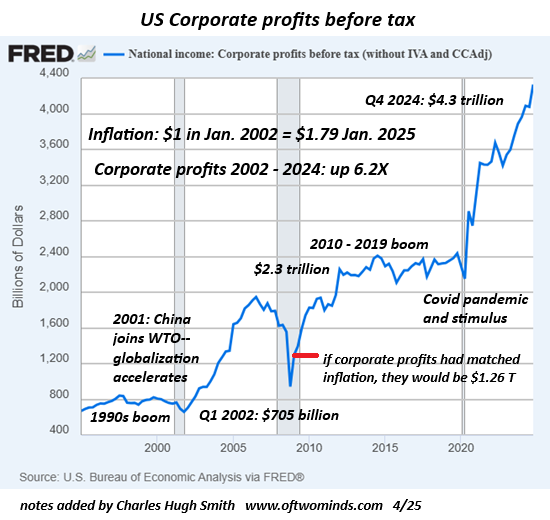

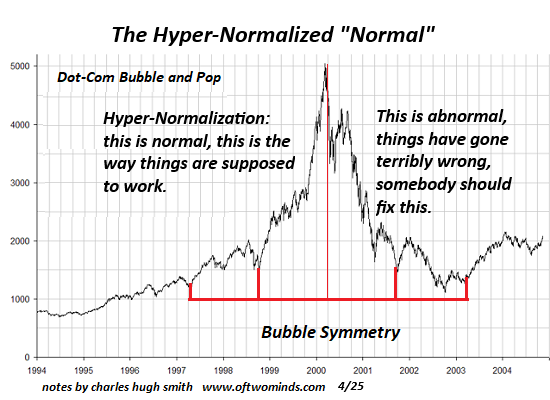

What’s "Normal" in a Hyper-Normalized World?

What’s "Normal" in a Hyper-Normalized World?21 Apr 2025