Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Financial Forecast 2025-2032: Please Don’t Be Naive

Financial Forecast 2025-2032: Please Don’t Be Naive15 Apr 2024

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?

Weekly Market Pulse: Are Higher Interest Rates Good For The Economy?15 Apr 2024

Sound Money Vs. Fiat Currency: Trade and Credit Are the Wild Cards

Sound Money Vs. Fiat Currency: Trade and Credit Are the Wild Cards11 Apr 2024

Global Recession’s Winners and Losers

Global Recession’s Winners and Losers6 Mar 2024

Rates, Risk and Debt: The Unavoidable Reckoning Ahead

Rates, Risk and Debt: The Unavoidable Reckoning Ahead26 Feb 2024

How the Economy Changed: There’s No Bargains Left Anywhere

How the Economy Changed: There’s No Bargains Left Anywhere23 Feb 2024

Digital Service Dumpster Fires and Shadow Work

Digital Service Dumpster Fires and Shadow Work14 Feb 2024

Market Morsels: ISM and Recession

Market Morsels: ISM and Recession7 Feb 2024

Irony Alert: "Outlawing" Recession Has Made a Monster Recession Inevitable

Irony Alert: "Outlawing" Recession Has Made a Monster Recession Inevitable7 Feb 2024

What the Fed Accomplished: Distorted the Economy, Enriched the Rich and Crushed the Middle Class

What the Fed Accomplished: Distorted the Economy, Enriched the Rich and Crushed the Middle Class4 Jan 2024

Macro: GDP Q3 — Inflationary BOOM!

Macro: GDP Q3 — Inflationary BOOM!22 Dec 2023

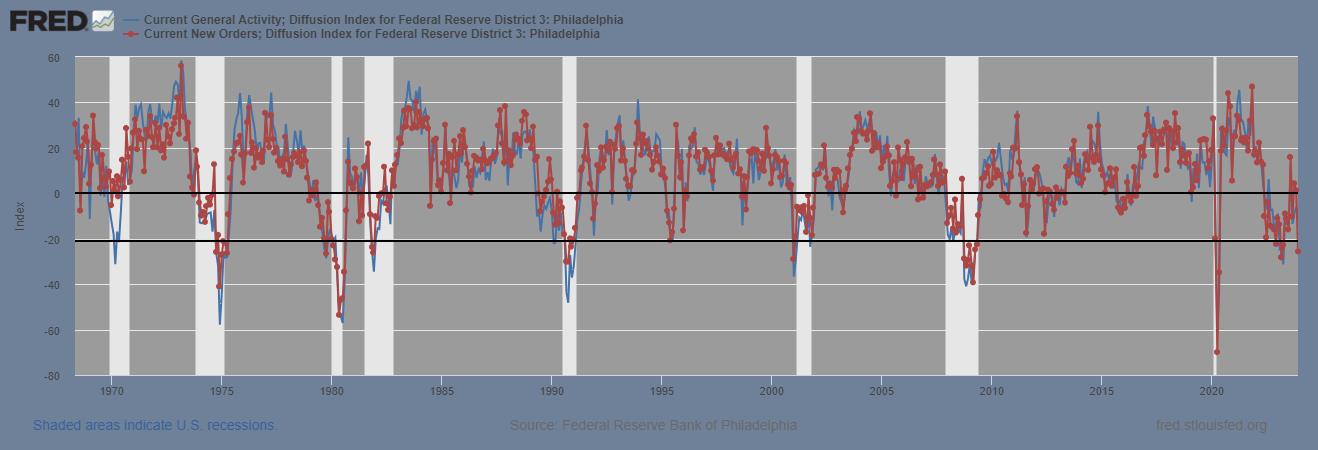

Macro: Philly Fed Mfg Survey — Umm

Macro: Philly Fed Mfg Survey — Umm22 Dec 2023

The Invisible Court’s Verdict: You Are Hereby Exiled to Digital Siberia

The Invisible Court’s Verdict: You Are Hereby Exiled to Digital Siberia9 Nov 2023

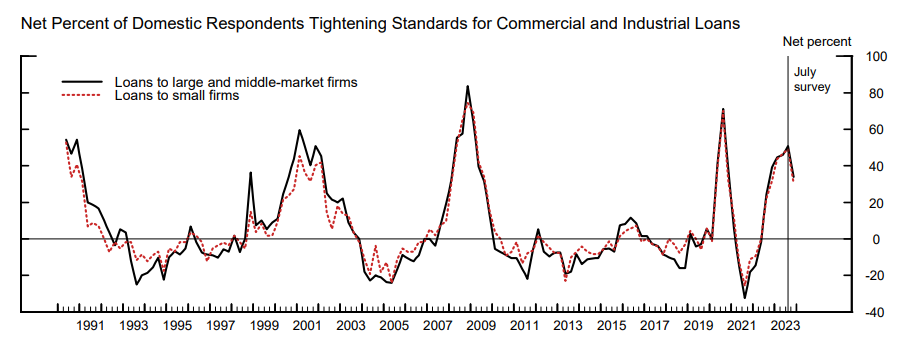

Macro: Banking: Senior Loan Officer’s Survey and Lending

Macro: Banking: Senior Loan Officer’s Survey and Lending8 Nov 2023

Weekly Market Pulse: Monetary Policy Is Hard

Weekly Market Pulse: Monetary Policy Is Hard6 Nov 2023

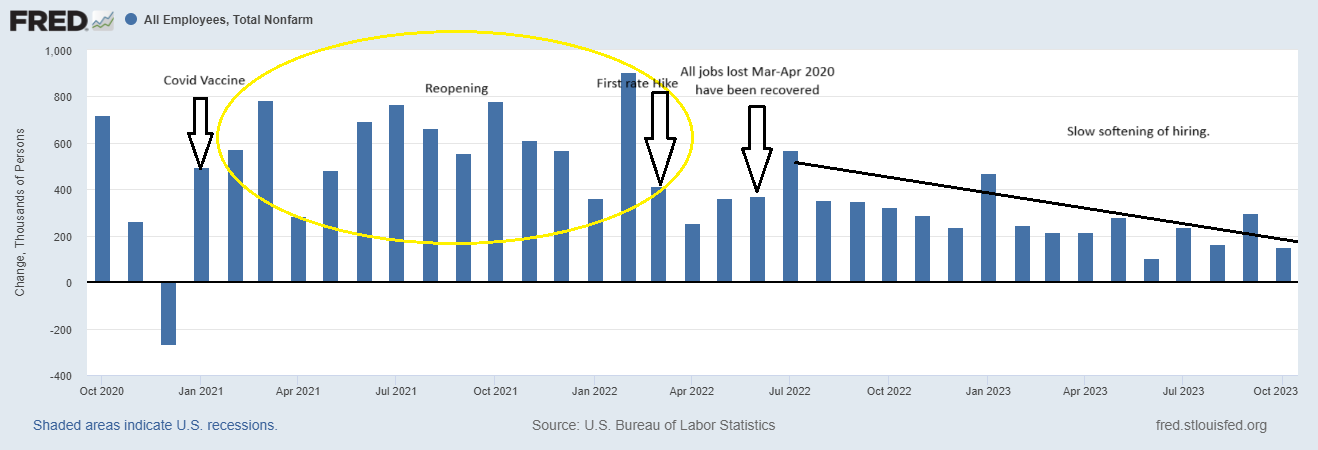

Macro: Employment Report

Macro: Employment Report3 Nov 2023

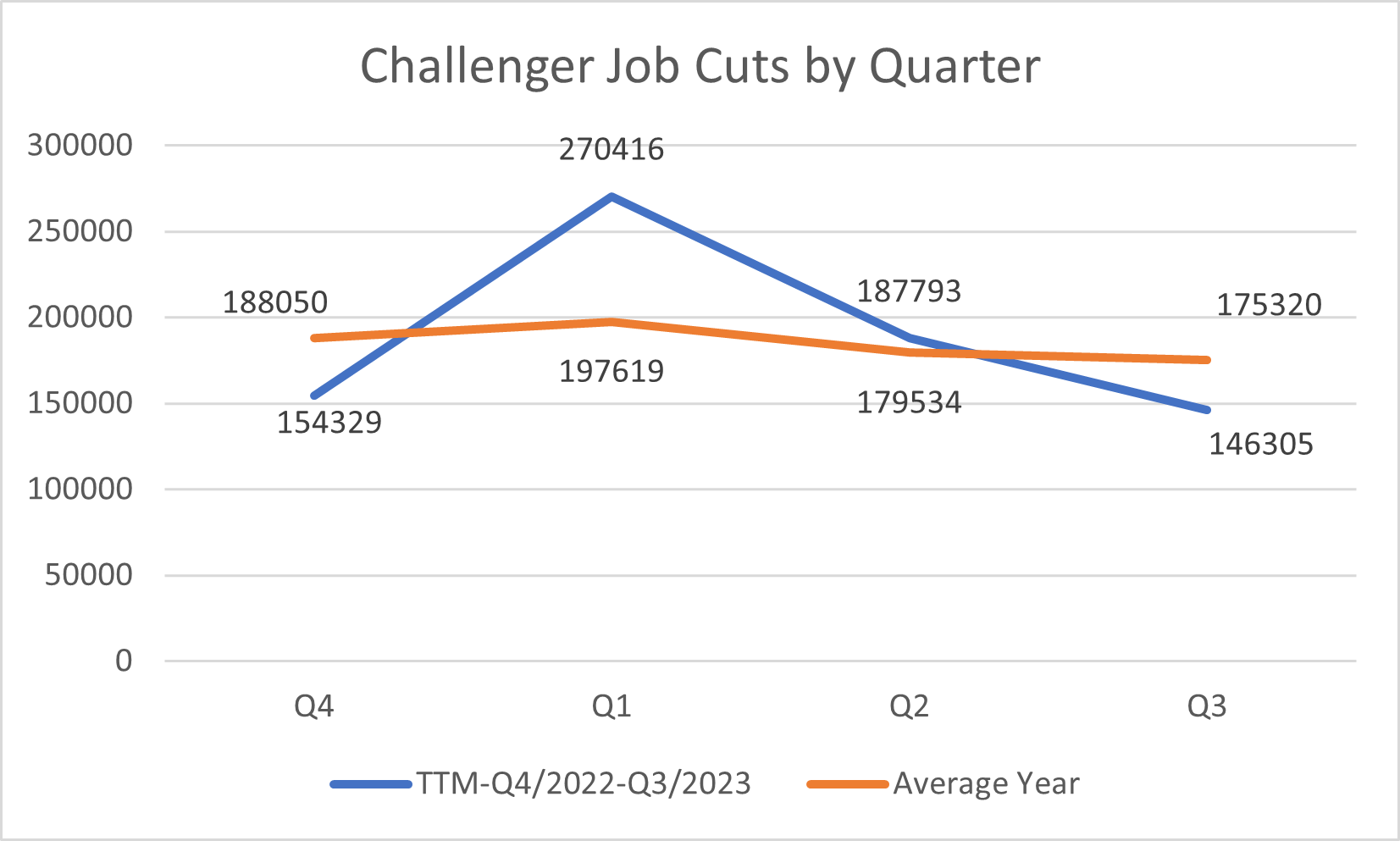

Macro: Challenger Job Cuts — Improvement throughout the year

Macro: Challenger Job Cuts — Improvement throughout the year2 Nov 2023

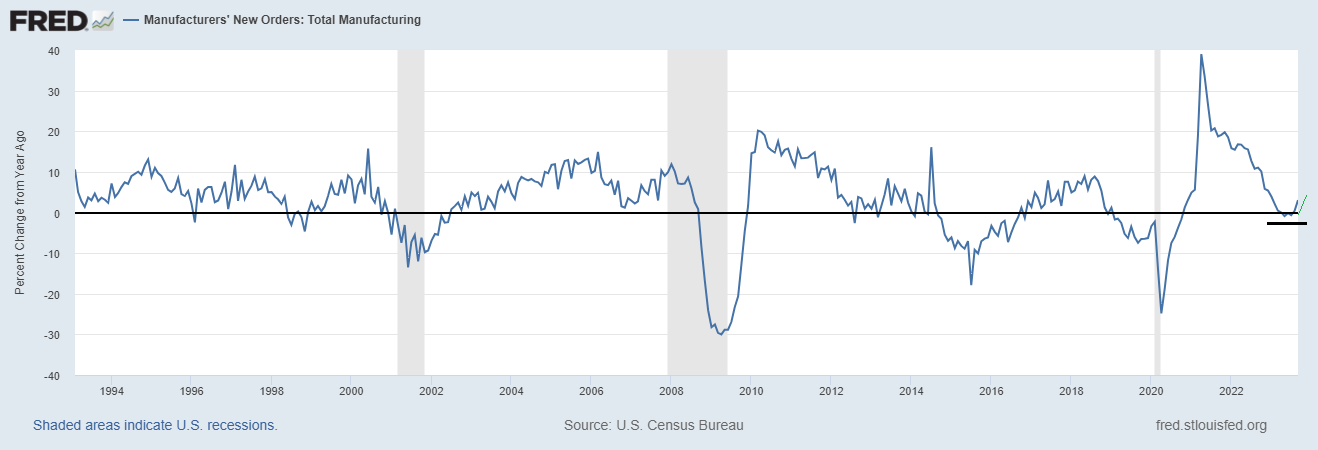

Macro: Factory Orders — revision

Macro: Factory Orders — revision2 Nov 2023

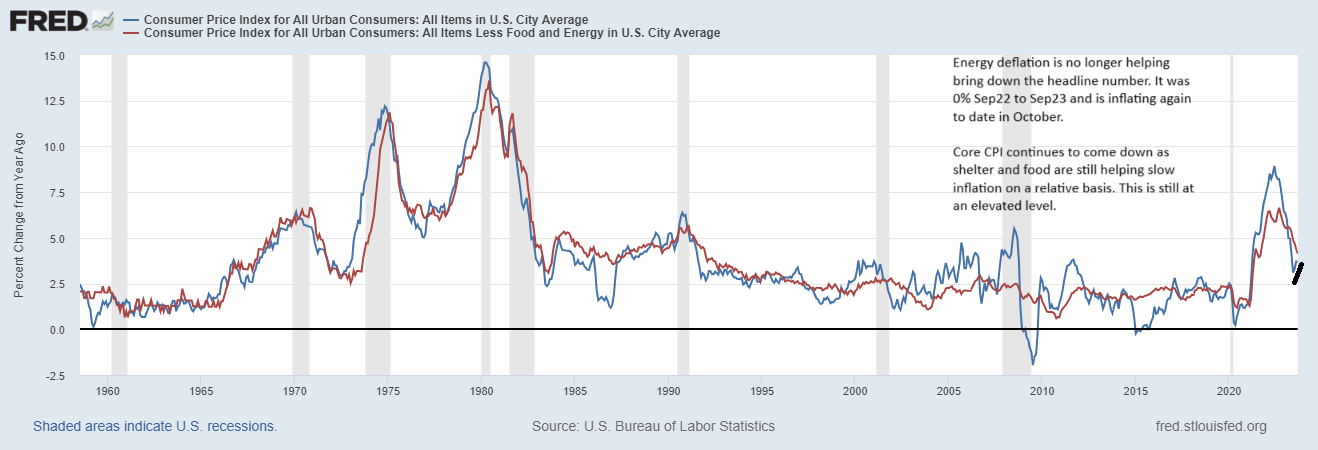

Macro: Sep CPI stuck at 3.7% YOY

Macro: Sep CPI stuck at 3.7% YOY13 Oct 2023

Financial Savvy Ways To Thrive In The Auto Market

Financial Savvy Ways To Thrive In The Auto Market8 May 2023