Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

SNB Sight Deposits: decreased by 5.6 billion francs compared to the previous week

SNB Sight Deposits: decreased by 5.6 billion francs compared to the previous week30 Apr 2024

11 May 2020

28 Feb 2019

24 May 2018

18 May 2018

23 Mar 2018

28 Feb 2018

The Secret History Of The Banking Crisis

The Secret History Of The Banking Crisis14 Aug 2017

28 Mar 2017

If It Didn’t Abandon The Gold Standard, U.S. Empire Would Have Collapsed…

If It Didn’t Abandon The Gold Standard, U.S. Empire Would Have Collapsed…19 Feb 2017

Sound Money and Your Personal Finances

Sound Money and Your Personal Finances24 Jan 2017

Pension Funds Need Gold before It’s Too Late

Pension Funds Need Gold before It’s Too Late19 Jan 2017

Rich Middle Class, Poor Middle Class

Rich Middle Class, Poor Middle Class15 Dec 2016

200 Russian Propaganda Sites, or simply alternative media?

200 Russian Propaganda Sites, or simply alternative media?10 Dec 2016

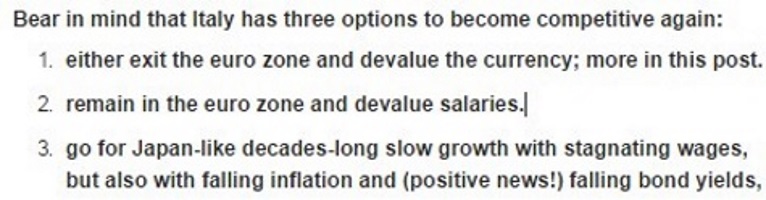

Italian Euro Exit: Why it Might Come in some Years and Why it Will Help the Euro Zone and Italy

Italian Euro Exit: Why it Might Come in some Years and Why it Will Help the Euro Zone and Italy5 Dec 2016

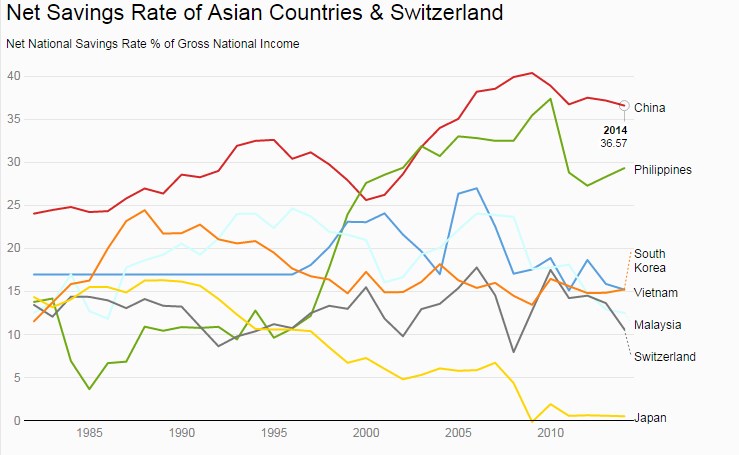

Net National Savings Rate, the Best Alternative Indicator to GDP Growth

Net National Savings Rate, the Best Alternative Indicator to GDP Growth4 Dec 2016

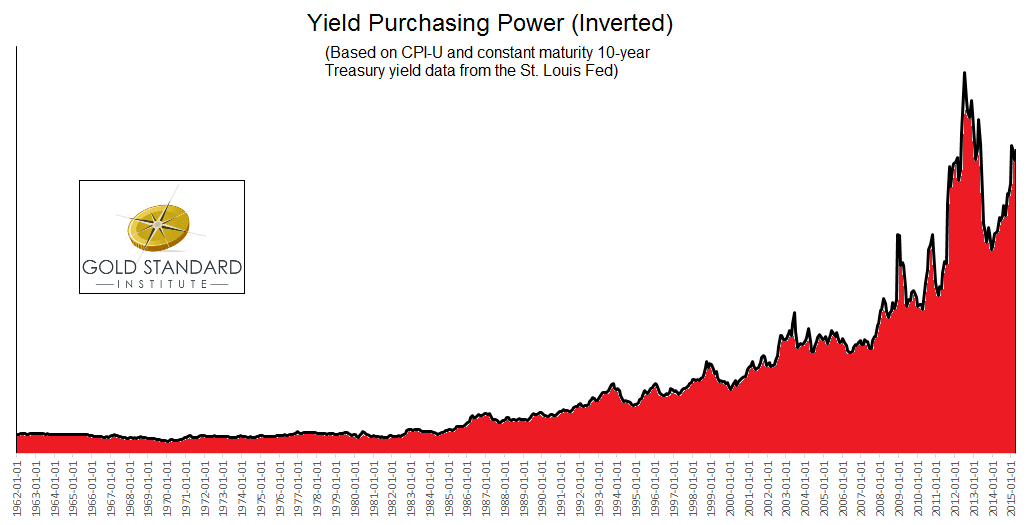

Introducing Yield Purchasing Power, the Video

Introducing Yield Purchasing Power, the Video26 Oct 2016

50 Slides for Gold Bulls – The Full Chart Book

50 Slides for Gold Bulls – The Full Chart Book25 Oct 2016

8 Oct 2016

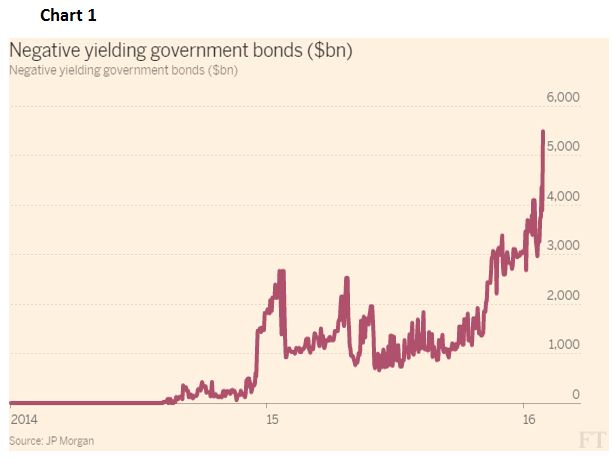

Understanding Negative Interest Rates

Understanding Negative Interest Rates1 Oct 2016