Read More »

Category Archive: 1) SNB and CHF

ECB rate cut creates complex situation for SNB

Read More »

Weekly Newspaper on Swiss National Bank and Swiss Franc

Feel free to click into the other categories “politics”, “business”, #chf, #snb in order to see more articles.

Read More »

Read More »

Fast CHF and Gold Price Movements

Read More »

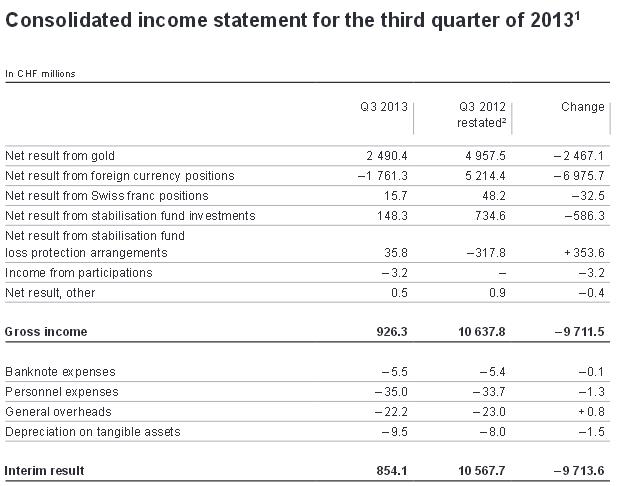

In Which Positions Does the SNB Win and Where Does it Lose Money: Details on the Q3 Results

Read More »

Weekly Newspaper on Swiss National Bank, Edition October 28

Read More »

SNB’s Jordan Responds to the Critique from the Peterson Institute: What They Forgot to Ask Him …

Read More »

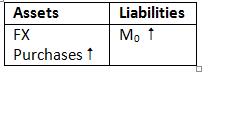

No SNB Intervention: Massive Swiss M0 Increase due to Post Finance Transformation into a Bank

Read More »

Danthine: SNB would end franc cap once it raises interest rates

Read More »

SNB Q2/2013 Composition of Reserves

Read More »

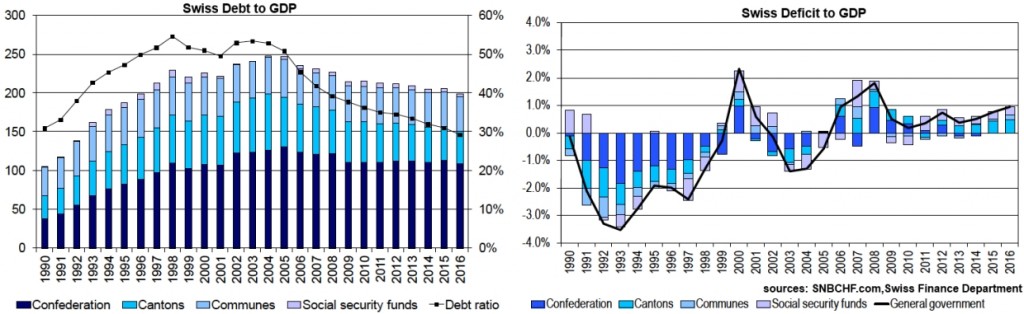

Debt Reduction, the new Financial Cycle, an Important Driver of EUR/CHF

Read More »

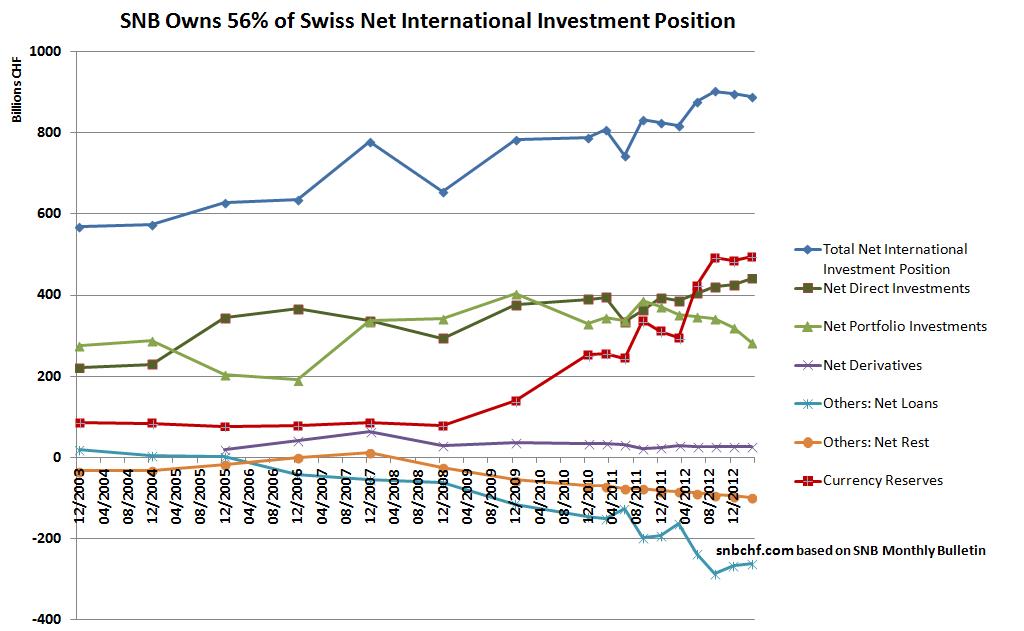

A Nationalization of Swiss Foreign Assets? SNB Owns 56% of Swiss Net International Investment Position

Read More »

Our Detailed Estimate of SNB Q2 Results: 17 Billion Francs Loss, The Reality 18 Billion

Read More »

Swiss ZEW Investor Survey Sees 1.20 per Euro Cap Gone within 2 Years

The Swiss ZEW investor sentiment has risen to 4.8 by 2.6 points, news that do not influence markets. More interesting is the following: Swiss ZEW Investor Survey Sees 1.20 per Euro Cap Gone within 2 Years * Majority see no change in euro/franc for next 6 months (Reuters) – The Swiss National Bank will most … Continue reading »

Read More »

Read More »

Swiss Franc History, 2012: CHF becomes a “safe” Risk-On Currency

Read More »

SNB Monetary Assessment June 2013: Very risk-averse, nearly hawkish tone

Read More »

Danthine’s Latest Statements Imply that SNB Might Remove Cap in 2014

Read More »

On Swiss National Bank

-

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

-

Household wealth in 2025

-

Heads up for NZD and CHF traders, RBNZ Gov Breman and SNB Chair Schlegel to speak

-

Swiss franc appreciation has led to tighter monetary conditions – SNB minutes

-

SNB’s Chairman Schlegel: A few months of negative inflation wouldn’t be a problem

Main SNB Background Info

Featured and recent

-

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week -

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete -

-40 Kilo! Ricarda Lang feiert Abnehmerfolg! Das Internet feiert!

-40 Kilo! Ricarda Lang feiert Abnehmerfolg! Das Internet feiert! -

Steuerrecht digitalisieren mit KI – eine gute Idee?

Steuerrecht digitalisieren mit KI – eine gute Idee? -

Why Switzerland is launching a charm offensive in Southeast Asia

Why Switzerland is launching a charm offensive in Southeast Asia -

Ex-Raiffeisen bank CEO fined for tax evasion

Ex-Raiffeisen bank CEO fined for tax evasion -

The price of gold matters, but availability matters more.

The price of gold matters, but availability matters more. -

FATAL: EU Chefdiplomatin blamiert ganz Europa! China außer sich!

FATAL: EU Chefdiplomatin blamiert ganz Europa! China außer sich! -

India’s situation shows why physical gold is different from paper exposure.

India’s situation shows why physical gold is different from paper exposure. -

ZUGRIFF auf dein Vermögen: So schützen sich INSIDER

ZUGRIFF auf dein Vermögen: So schützen sich INSIDER

More from this category

- Household wealth in 2025

28 Apr 2026

- Swiss franc appreciation has led to tighter monetary conditions – SNB minutes

16 Apr 2026

- Heads up for NZD and CHF traders, RBNZ Gov Breman and SNB Chair Schlegel to speak

15 Apr 2026

- SNB’s Chairman Schlegel: A few months of negative inflation wouldn’t be a problem

21 Jan 2026

- 2025-07-31 – Interim results of the Swiss National Bank as at 30 June 2025

31 Jul 2025

SNB Brings Back Zero Percent Interest Rates

SNB Brings Back Zero Percent Interest Rates26 Jun 2025

- 2/2025 – Business cycle signals: SNB regional network

25 Jun 2025

- 2025-06-25 – Quarterly Bulletin 2/2025

25 Jun 2025

- Hold-up sur l’eau potable (2/2) : la supercherie de « l’hydrogène vert ». Par Vincent Held

24 Jun 2025

- Hold-up sur l’eau potable (1/2) : la fin de l’abondance. Par Vincent Held

20 Jun 2025

- Swiss interest rate cut to zero

20 Jun 2025

- 2025-06-20 – Swiss balance of payments and international investment position

20 Jun 2025

- ICYMI – Swiss National Bank cut interest rates by 25 basis points to 0%

20 Jun 2025

- SNB chairman Schlegel: We don’t take decision on negative interest rates lightly

19 Jun 2025

- 2025-06-19 – Martin Schlegel / Antoine Martin / Petra Tschudin: Introductory remarks, news conference

19 Jun 2025

- 2025-06-19 – Monetary policy assessment of 19 June 2025

19 Jun 2025

- 2025-06-19 – Publication of Financial Stability Report 2025

19 Jun 2025

Was kann die Schweizerische Nationalbank tatsächlich bewirken?

Was kann die Schweizerische Nationalbank tatsächlich bewirken?12 Jun 2025

Swiss National Bank Trials Blockchain to Modernise MDB Financial Processes

Swiss National Bank Trials Blockchain to Modernise MDB Financial Processes24 Apr 2025

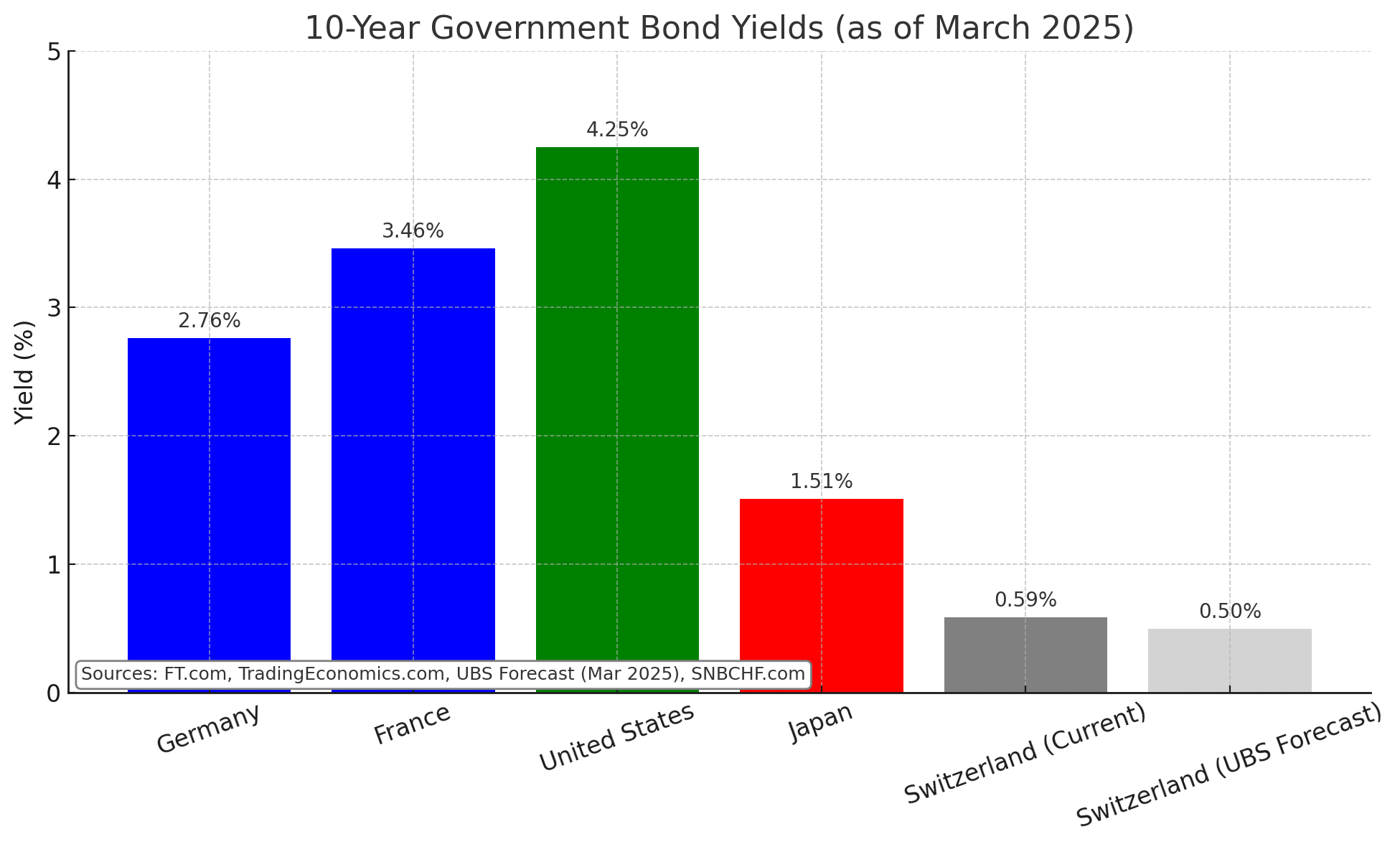

SNB Monetary Assessment March 2025

SNB Monetary Assessment March 202523 Mar 2025