Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The week ahead is arguably the most important here at the start of 2020. The Federal Reserve and the Bank of England meet. The US and the eurozone report initial estimates of Q4 19 GDP. The eurozone also reports its preliminary estimate of January CPI. China returns from the extended Lunar New Year celebration and reports its official PMI. Japan will report December retail sales and industrial production. These data points will provide insight into the state of the recovery from the October sales tax and typhoon.

ChinaFears of the spread of a new virus from China and the potential economic impact weighed on the risk-taking appetites last week. It is still the early days, but the contagion rate appears to be tracking something close to SARS, which ended up slashing Chinese growth by two percentage points. China and Hong Kong equity markets were hit the hardest (3%+), the S&P 500’s decline of a little more than 1%, was only the fourth weekly loss but the largest since the end of Q3 19. China reports the newest PMI readings on January 30. The impact of the coronavirus may not be picked up entirely in the data, which will not offer a clean read on the economy due to the Lunar New Year. To the extent that the virus impact is detected, it will likely hit services harder that manufactured goods in the first instance. That said, January manufacturing and non-manufacturing PMI are expected to have softened a little (50.2 and 53.5, respectively in December). The risk is that the economic disruption will offset the stimulus recently provided. The magnitude of the commitment to buy US goods was already a stretch, according to some estimates, and weaker Chinese growth could provide another hurdle. It has been widely reported that China committed to buying $200 bln more US goods than the $128 bln purchased in 2017, the last year before the tariffs. However, last year, the US exports to China were about $98 bln. So, compared with 2019, China has committed to buying $230 bln more US goods. China will likely import a bit more than $2 trillion of goods and services this year. The political agreement appears to secure for the US a little more than 15% of that market. |

Economic Events: China, Week January 27 - Click to enlarge |

With a press conference after every FOMC meeting, and given Powell’s perceived communication challenges, it is difficult to say that the January 29 meeting is a non-event. Still, for all practical purposes, it is. There is scope for a small technical adjustment. The Fed pays 1.55% interest on both required and excess reserves. It could raise this by five basis points to ensure the fed funds rate remains within the 1.50%-1.75% target range. Many who think the Fed’s bill buying and repo operations represent an easing of monetary policy (as in QE), they may argue that the Fed is tightening. However, most will likely conclude that it would be a technical adjustment and not a change in monetary policy proper.

The forecasts will not be updated until March, and the economy has not materially deviated from Fed expectations. Last year, some media reports played up the two persistent dissents against the series of rate cuts and argued Powell was losing control. However, this does not seem to be the case, and indeed a clear consensus has emerged. At the December meeting, 14 of the 17 officials thought no rate change would be needed this year.

Near-term downside risks have lessened. The US-China trade deal may not deserve the embellished official descriptions, but an escalation in the coming months seems less likely than even a couple of months ago. The UK will leave the EU at the end of January for an 11-month standstill arrangement where nothing changes while a new trade deal is negotiated. The risk of a disruptive no-deal exit at the end of the year remains, but it is not yet pressing. Nevertheless, the implied yield of the December 2020 fed funds futures contract is near 1.30% compared with the current average of 1.55%, suggest a 25 bp Fed cut has been discounted.

The Bank of England is a different story. Two members of the Monetary Policy Committee have dissented at the past couple of meetings in favor of an immediate rate cut. Two other members have indicated if the data did not improve, they too could support a rate reduction. BOE Governor Carney also sounded more dovish in recent comments. The January 30 BOE meeting will be the last Carney chairs. Andrew Baily will take the reins before the next meeting on March 26.

The official comments and the disappointing economic data has spurred a shift in market expectations. On January 10, the derivatives market implied a little less than a one-in-four chance of a rate cut on January 30. By January 17, the odds jumped to almost three-in-four. But sentiment swung back last week, and the odds narrowed to a little less than 50/50. It is a close call, and on balance, the resilience of the labor market, the recovery in business confidence, and the uptick in the PMI may keep the BOE on hold a bit longer. If this is indeed the case, sterling may pop higher, though ideas that lower rates can still be delivered later in H1 may limit the upside.

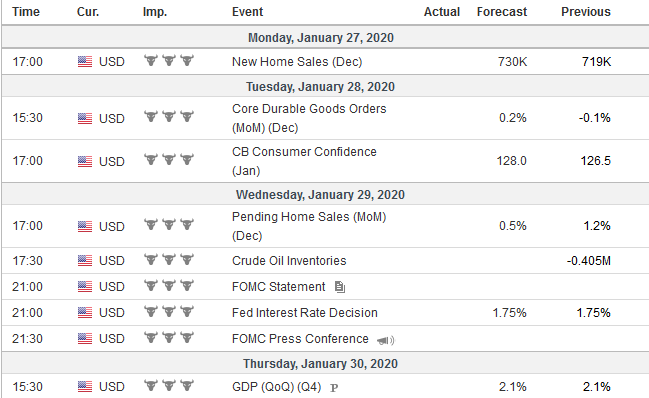

United StatesQuarterly GDP numbers often grab the headline, but for many investors, the report is a culmination of other high-frequency data with some variance. Moreover, GDP data is backward-looking. It is then more a favorite of economists than market participants. That said, the mixed signals of the US economy make this GDP call particularly tricky, and the first estimate is subject to statistically significant revisions, often stemming from trade and inventories. The NY Fed’s GDP tracker (as of January 17) pointed to a sub-par 1.2% annualized pace. The Atlanta Fed’s model pointed to a 1.8% pace. The Bloomberg survey has a median forecast of 2.1%. The composition of US growth may have also changed. Consumption may have slowed from the 3.2% annualized pace in Q3. Residential investment appears to have risen, and trade also may have made a net positive contribution. The headline and core deflator are likely to be mostly steady. The Federal Reserve will look through just about any weakness in Q4 GDP and will make allowances for the production cuts at Boeing in Q1 20. The case of a rate cut is based on ideas that record-long US expansion is fragile and will have increasing difficulty coping with shocks. The lack of pick-up in early Q2 will leave the Fed with the same choice as last year. With price pressures subdued, another insurance policy can be taken out to boost the chances that the expansion can be extended. |

Economic Events: United States, Week January 27 - Click to enlarge |

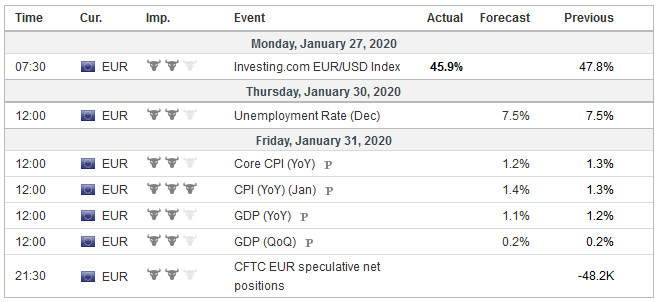

EurozoneEurozone Q4 GDP seems easier to forecast. Growth has been relatively steady, with quarterly growth averaging about 0.3% for the past four quarters and 0.2% for the previous two. The year-over-year pace has been about 1.2% over the same period. It may not be very inspiring, but it is steady, and growth potential is probably only a little higher at around 1.5% or so. Market participants appear to be more confident that the ECB is on hold for the duration that it is of the Fed. The market sees only about a one-in-five chance of a rate cut by the ECB this year. Perhaps the most challenging data point for investors to make sense of will be the initial estimate of the eurozone’s January consumer inflation. Prices fall in January. Last January, prices fell by 1%. That means that if prices fell by 0.9% this month, as economists forecast, the year-over-year rate will tick up. Indeed, the year-over-year rate is expected to rise to 1.4%. It would be the highest since last April. This is one reason why claims of Japanification of Europe are too simplistic: European inflation is nearly twice that of Japan’s. However, while we anticipate a base-effect rise in European CPI, the comparisons are not as friendly, and the true signal, as likely to be reflected in the core rate that may ease to 1.2% after being stuck at 1.3% in November and December. |

Economic Events: Eurozone, Week January 27 - Click to enlarge |

Lastly, we turn to Japan. The issue at hand is how quickly it can rebound from the controversial sales tax increase and the typhoons. The most direct report will be retail sales. Recall the sequence of events. Anticipating the tax increase in October, consumers brought forward purchases, and August retail sales rose by 4.6% and then 7.2%, before plummeting 14.2% in October. They snapped back 4.5% in November and probably a little more than 1% in December.

Industrial output fell by 4.5% in October and another 1% in November. A small rise of around 0.7% is expected in December. Yet, in terms of the yen, these macro considerations seem to be of secondary importance. The heightened anxiety over the new coronavirus expressed through the sale of risk-off assets, and the unwinding of carry-trades and those speculators knowingly or unknowingly riding this wave is the primary driver now as the dollar’s advance was stalling around JPY110.25.

The coronavirus is an economic and financial shock. The extent of that shock still needs to be assessed but it could provide the spark for an arguably long-overdue adjustment in the capital markets. Investors may be risk-averse until there is greater transparency about the contagion rate and health risks. It is humbling to appreciate that despite the advances in science and medicine, some 80k Americans died in 2017-2018 from influenza, the highest toll in 40 years. The World Health Organization estimates that the annual flu epidemic kills between around 250k-500k people globally each year.

Full story here Are you the author?

Tags: Bank of England,China,EMU,federal-reserve,GDP,Japan,newsletter