Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

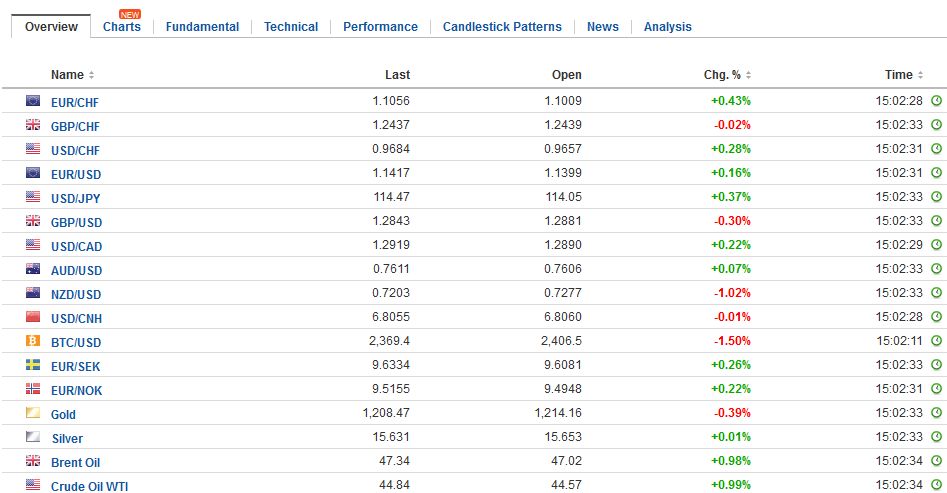

Swiss FrancThe Euro has risen by 0.41% to 1.1054 CHF. |

EUR/CHF - Euro Swiss Franc, July 11(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesInvestors await fresh policy clues as the Bank of England’s Broadbent is seen as a key vote on a closely balanced MPC, while the Fed’s Brainard, is also seen as a bellwether, will speak shortly after midday in NY. Broadbent has not spoken since the election, and his current views are not known. If he sides with the dissenting hawks, sterling could rally and rechallenge the $1.30 cap. On the other hand, if the Deputy Governor sides with Governor Carney, as we suspect, sterling could return to sub-$1.29 area. Note that there are two large option strikes that expire today. At $1.2933 there is a GBP400 bln that is on the bubble today, and GBP773 struck at $1.30. |

FX Daily Rates, July 11 - Click to enlarge |

| Oil prices briefly extended yesterday’s recovery, ostensibly helped by talk that OPEC may seek to cap Nigerian and Libyan output. However, prices reversed course after briefly rising through yesterday’s highs. The August light sweet crude was turned back from $45. Yesterday’s low was set near $43.65, while last month’s low was set near $42.00. US production increases and strong exports are seen blunting the impact of a decline in local inventories.

The dollar is up against the yen for a third session. It has now edged through the May highs set near JPY114.35. The next chart point is near JPY114.60, but the JPY115 area is more psychologically important. The euro is consolidating in less than a 20 tick range through the Asian session and most of the European morning. The Australian dollar edged higher for the third session today but it is finding the air above $0.7600 is thin. The three-day rally snapped a four-day down draft. |

FX Performance, July 11 - Click to enlarge |

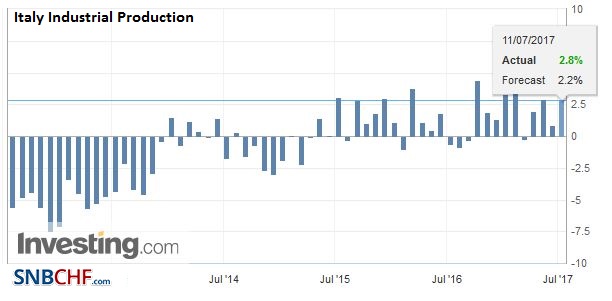

ItalyThe main economic news comes from Europe today, where Italy reported stronger than expected industrial production for May. The 0.7% increase on the month compares with the median forecast in the Bloomberg survey for a 0.5% rise. The April decline was revised to -0.5% from -0.4%. However, the year-over-year pace (work-day adjusted) was 2.8%. Germany, France, and Spain have reported their figures (all 1% of above), and the aggregate figure is due tomorrow. Industrial output in Q2 appears to be running at its best clip in a couple of years. |

Italy Industrial Production YoY, May 2017(see more posts on Italy Industrial Production, ) Source: Investing.com - Click to enlarge |

United Kingdom

BRC sales figures were stronger than expected, rising 1.2% in June after a 0.4% fall in May. This seemed to underpin sterling, which largely held support seen near $1.2860 yesterday. BRC cautioned that unseasonably warm weather boosted clothes sales and higher food prices flattered the report. Tomorrow, the UK’s employment report will provide an update on wage pressures, which, at the headline rate, may have slowed.

United States

The Fed’s Brainard express caution recently in the face of the four-month slide in core prices (both CPI and PCE deflator). Little has been reported to make her less cautious. However, if she indicates that she is sympathetic to what seems like a majority view that the decline in price pressures are due to transitory factors it could neutralize her cautious stance. Still, we expect the Federal Reserve to announce the beginning of its balance sheet operations at the September FOMC meeting to start in October, leaving the possibility of a third rate hike this year to December.

Brainard is not the only Fed news. Late yesterday, reports indicate that the White House has indicated it will nominate Quarles, formerly in the G.W. Bush Treasury Department as the Vice Chairman of Supervision to the Federal Reserve. If Quarles is confirmed, and there is little doubt over this, he would have a four-year term as in that role as Vice Chair and 14 years as a Governor, (serving until 2032). Note that even though the Trump Administration has been critical of Dodd-Frank,the appointment fulfills one of the law’s requirements.

US economic data includes the JOLTS report and wholesale inventories and sales. These are not typically market-moving reports. The Fed’s Beige Book is out tomorrow, and Yellen’s semi-annual testimony begins. Canada reports housing starts today ahead of the Bank of Canada meeting tomorrow. A rate hike is well discounted. The Bank of Canada appears to have initiated a campaign beginning in the middle of last month to prepare the market for a hike. Since May 5, the Canadian dollar has been the strongest major currency, appreciating 5.7% against the US dollar.

Japan

Japan dodged a trouble with its successful five-year bond auction today. There was concern that although the BOJ drew a line before the weekend to buy unlimited 10-year bonds, its defense did not extend to the five-year. Nevertheless, today’s five-year bond sale was well-received. The bid-cover was 4.85x, the highest in nearly three years. Nevertheless, yields stay elevated, and the focus shifts to tomorrow’s scheduled BOJ short-end bond purchases.

Separately, we note reports suggest that the BOJ has begun applying the negative deposit rate to some deposits by foreign central banks and other international institutions. If the deposits exceed a threshold amount, they will be charged the market rate (zero) minus five basis points. As of the end of March, foreign official accounts had about JPY13.6 trillion (~$119 bln) at the BOJ. Note that according to the IMF’s COFER data, the dollar value of yen reserves at the end of Q1 was $403 bln.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$EUR,$JPY,EUR/CHF,FX Daily,Italy Industrial Production,newslettersent