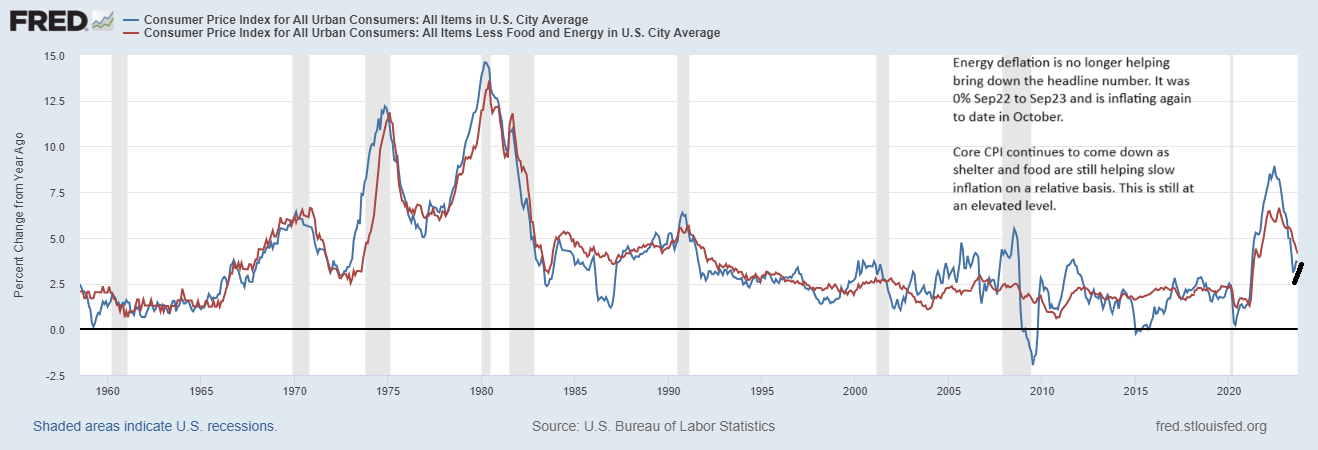

Let’s look under the hood a bit because headlines will mention “sticky” CPI and there are some reasons that CPI will indeed be stickier for longer than we hope.

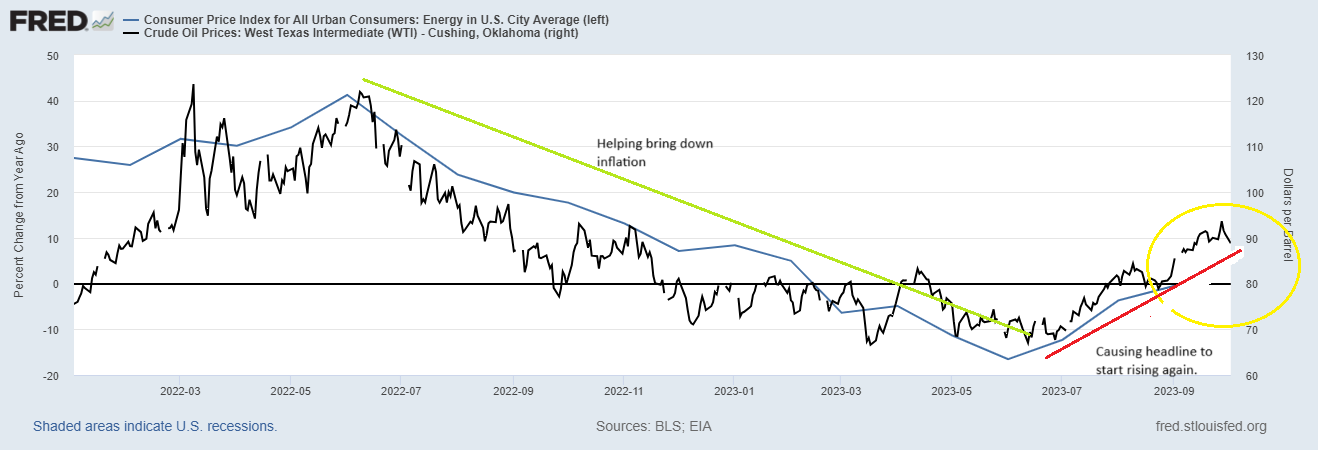

Let’s first start with energy which is about 7.5% of the basket. With the exception of the spike in oil coinciding with the Russian invasion of Ukraine, oil peaked in June 22 at around $122/bbl. So for the whole year of June22-June23 oil was helping bring inflation down. In June22 energy inflation was 41.25% yoy and abated throughout the 12 month period eventually turning negative in March 23 and bottoming in June23 at -16.5% yoy growth. This June to June time period coincides with the peak of oil in 2022 and the low for oil in 2023. For energy to have the same accumulative effect on slowing inflation, it will have to repeat the same level of incremental slowing as it did last year. Oil prices were -42.5% during this period, its not looking like a repeat performance as oil is up around 29% since then. The Sep22-Sep23 change in energy prices is -0.5%. While not outright additive for the last year, a -0.5% rate growth in energy prices is higher than last month’s -3.6% change. And this increase in the change of energy prices this year relative to the decrease we had last year, will cause the headline number to go up, all else being equal. This is the sticky dynamic we’re seeing and the reason the headline number is up since June.

Let’s look under the hood a bit because headlines will mention “sticky” CPI and there are some reasons that CPI will indeed be stickier for longer than we hope.

Let’s first start with energy which is about 7.5% of the basket. With the exception of the spike in oil coinciding with the Russian invasion of Ukraine, oil peaked in June 22 at around $122/bbl. So for the whole year of June22-June23 oil was helping bring inflation down. In June22 energy inflation was 41.25% yoy and abated throughout the 12 month period eventually turning negative in March 23 and bottoming in June23 at -16.5% yoy growth. This June to June time period coincides with the peak of oil in 2022 and the low for oil in 2023. For energy to have the same accumulative effect on slowing inflation, it will have to repeat the same level of incremental slowing as it did last year. Oil prices were -42.5% during this period, its not looking like a repeat performance as oil is up around 29% since then. The Sep22-Sep23 change in energy prices is -0.5%. While not outright additive for the last year, a -0.5% rate growth in energy prices is higher than last month’s -3.6% change. And this increase in the change of energy prices this year relative to the decrease we had last year, will cause the headline number to go up, all else being equal. This is the sticky dynamic we’re seeing and the reason the headline number is up since June.

Now let’s move to the 2 biggest pieces of the consumer basket, food and shelter. Shelter is by far the largest at about 1/3 of the pie. Unfortunately, we are going to see the same sticky dynamic for food and shelter, just a bit delayed relative to the short term price translation of energy and not as extreme as the volatile prices of energy.

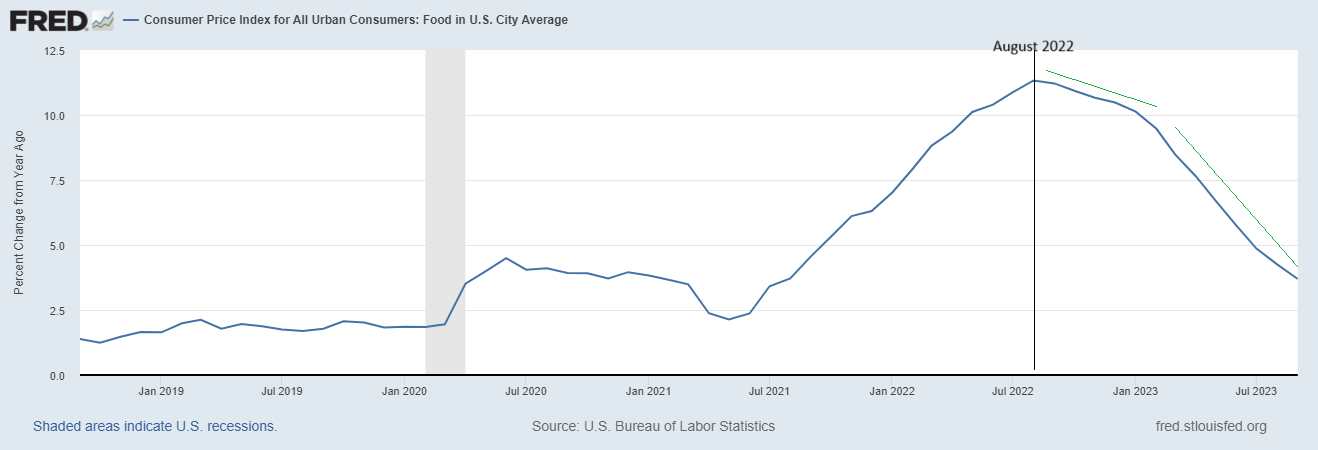

Starting with food, the sticky dynamic is starting to happen now given the peak in food inflation was August 2022 (11.3%). The rate of food inflation came down inch by inch throughout the remainder of 2022 before really slowed in the first half of 2023. In the current release of Sept23 data, food inflation is currently 3.7%yoy. Food disinflation on a relative basis is starting to have difficult comparisons and these will get more difficult in beginning in March 24. This is hard to conceptualize, but if inflation remains at this MOM level as it has for the past 3 months, food inflation on an annual basis will decline at a slower rate from now until February 2024 and then start to actually go up in March 24. This is part of the dynamic of the persistent stickiness that we are dealing with. Just as sticky energy dynamics may abate, sticky food kicks in.

Now let’s move to the 2 biggest pieces of the consumer basket, food and shelter. Shelter is by far the largest at about 1/3 of the pie. Unfortunately, we are going to see the same sticky dynamic for food and shelter, just a bit delayed relative to the short term price translation of energy and not as extreme as the volatile prices of energy.

Starting with food, the sticky dynamic is starting to happen now given the peak in food inflation was August 2022 (11.3%). The rate of food inflation came down inch by inch throughout the remainder of 2022 before really slowed in the first half of 2023. In the current release of Sept23 data, food inflation is currently 3.7%yoy. Food disinflation on a relative basis is starting to have difficult comparisons and these will get more difficult in beginning in March 24. This is hard to conceptualize, but if inflation remains at this MOM level as it has for the past 3 months, food inflation on an annual basis will decline at a slower rate from now until February 2024 and then start to actually go up in March 24. This is part of the dynamic of the persistent stickiness that we are dealing with. Just as sticky energy dynamics may abate, sticky food kicks in.

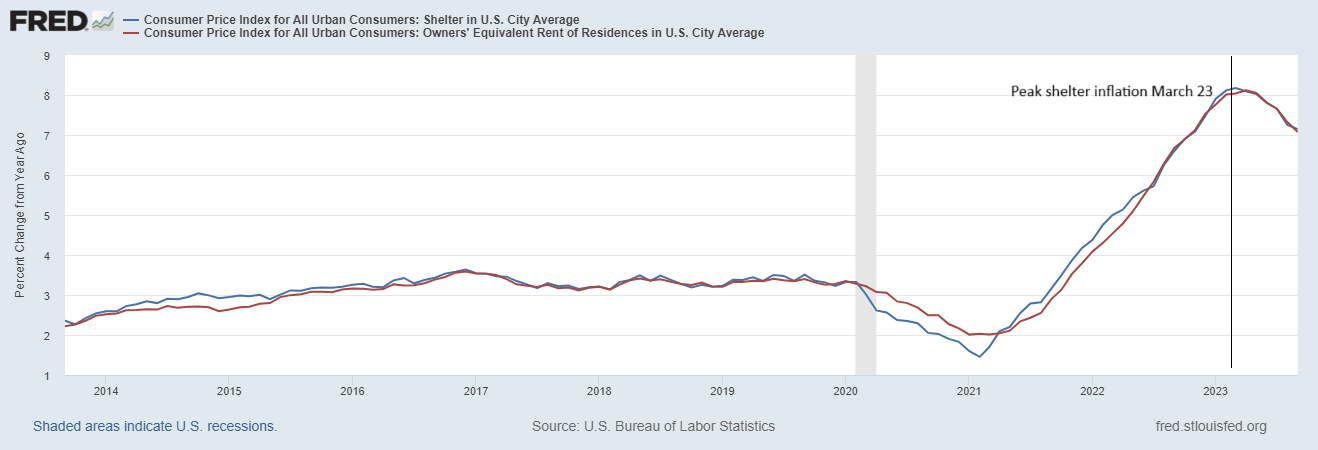

And at this same time, the difficult comparisons for shelter will begin. Luckily the shelter component is like a tortoise compared to food and energy who have been excluded from the core. But it is a big piece of the basket so will certainly have a sticky dynamic for inflation unless it starts to comes down faster next spring than it did in the spring of 22. Shelter went up .35% in this same MOM period last year and it came down .1% this year, so core inflation is coming down. Energy is causing the opposite dynamic with the headline number which rose from 3.09% from June to August and is now stuck.

And at this same time, the difficult comparisons for shelter will begin. Luckily the shelter component is like a tortoise compared to food and energy who have been excluded from the core. But it is a big piece of the basket so will certainly have a sticky dynamic for inflation unless it starts to comes down faster next spring than it did in the spring of 22. Shelter went up .35% in this same MOM period last year and it came down .1% this year, so core inflation is coming down. Energy is causing the opposite dynamic with the headline number which rose from 3.09% from June to August and is now stuck.

What’s the implication for monetary policy? We’ll have to wait and see. The consensus is that a an 89% chance that rates will be held steady at the November meeting. But the Fed will see 2 more employment reports, 2 more PCE reports and 2 more CPI reports between now and the December meeting. Consensus puts the probability of a December hike at 32%.

What’s the implication for monetary policy? We’ll have to wait and see. The consensus is that a an 89% chance that rates will be held steady at the November meeting. But the Fed will see 2 more employment reports, 2 more PCE reports and 2 more CPI reports between now and the December meeting. Consensus puts the probability of a December hike at 32%.

Disclaimer: This information is presented for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy any investment products. None of the information herein constitutes an investment recommendation, investment advice or an investment outlook. The opinions and conclusions contained in this report are those of the individual expressing those opinions. This information is non-tailored, non-specific information presented without regard for individual investment preferences or risk parameters. Some investments are not suitable for all investors, all investments entail risk and there can be no assurance that any investment strategy will be successful. This information is based on sources believed to be reliable and Alhambra is not responsible for errors, inaccuracies, or omissions of information. For more information contact Alhambra Investment Partners at 1-888-777-0970 or email us at [email protected].

Full story here Are you the author?Tags: Core CPI,CPI,Featured,food prices,inflation,Markets,newsletter,OIL