Jeffrey P. Snider

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

|

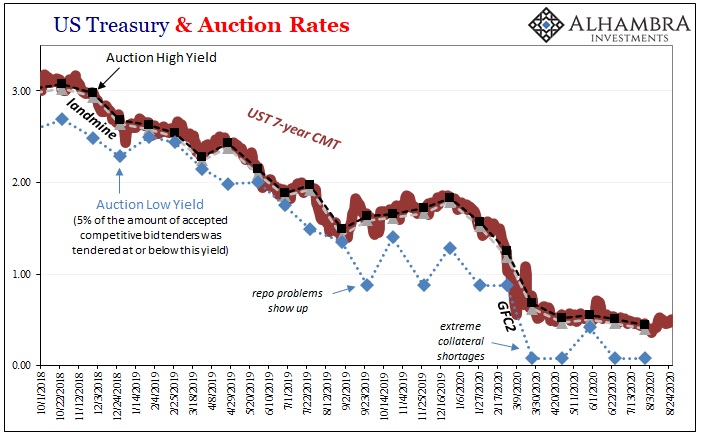

Tomorrow, the Treasury Department is going to announce the results of its latest bond auction. A truly massive one, $47 billion are being offered of CAH4’s notes dated August 31, 2020, maturing out on August 31, 2027. In other words, the belly of the belly, the 7s. We’ve already seen them drop for two-note auctions this week, both equally sizable. Yesterday, Treasury floated $50 billion in 2-year notes that the supposedly under-siege banking system yet had little trouble gobbling up. Before that, $51 billion of 5s with the same number of auction issues: zero. The common explanation is what the common explanation always is: the Fed. Gigantic QE, people say, has monetized the bulk of these assets otherwise it would be game over for the Treasury market. |

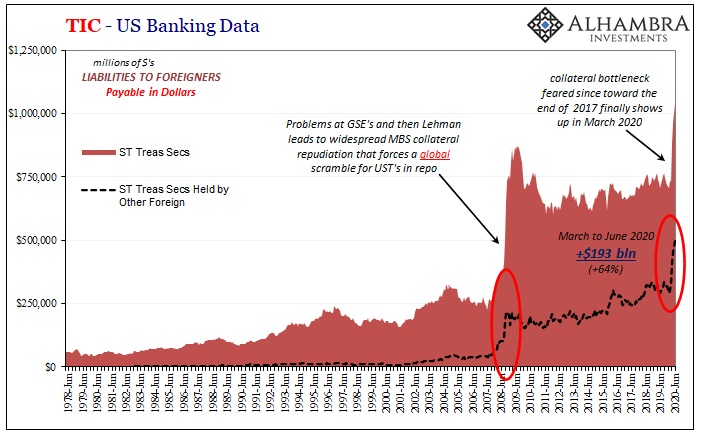

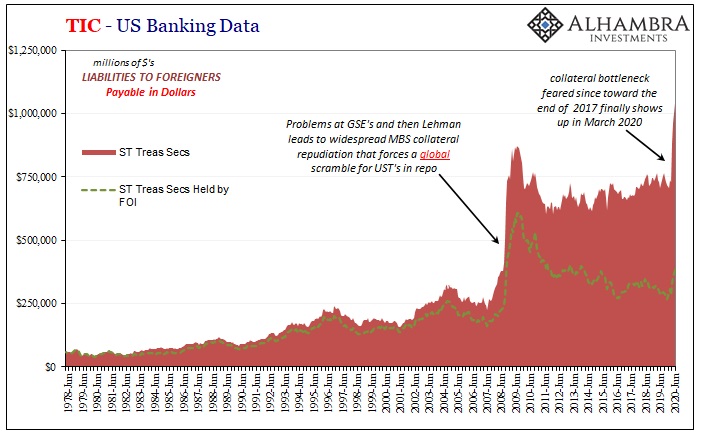

US Banking Data, 1978 - 2020 - Click to enlarge |

| BOND ROUT!!!! in the extreme (maybe five or six exclamations tacked on its end).

Like gold’s recent rise, there’s a fair amount of revisionism in that view. When the Fed is the center of your universe it’s understandable why you’d believe history began in the middle of March 2020. But even that fails to account for how it was the private marketplace which absorbed more than $2 trillion in bills Jay Powell was at least aware enough to stay away from (though he continues to display his complete lack of appreciation for why he was right to do so). |

US Banking Data, 1978 - 2020 - Click to enlarge |

| In fact, the Fed has bought so many bonds and notes that they’re actually trading special in the repo – meaning there aren’t enough of certain issues out in the collateral marketplace! You see, the level of demand hasn’t really changed for UST’s across the curve, the only factor which has is the Fed’s activity in that marketplace.The first “too many” Treasuries explanation didn’t really last beyond 2018, though it would take another year for some of its most vocal proponents to realize this (some still refuse). The idea then was the same as it is now: the government has simply gone batshit crazy, giving drunken sailors and history’s litany of money printing despots a bad name.

And that is absolutely true. |

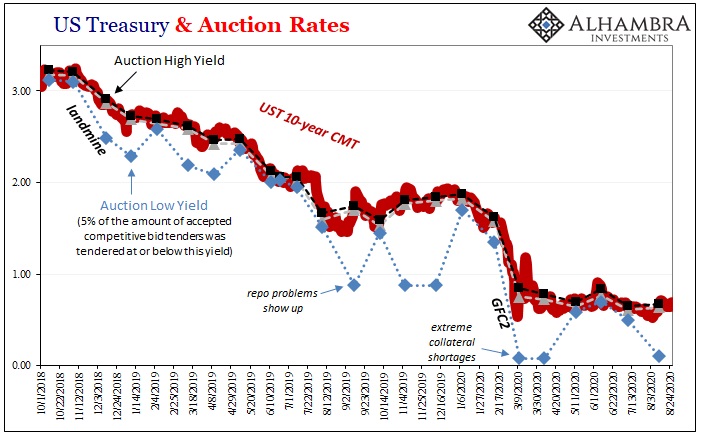

US Treasury and Auction Rates, Oct 2018 - Aug 2020(see more posts on U.S. Treasury, ) - Click to enlarge |

| But what has happened in many circles is that emotion is being substituted for rational analysis; hatred for the abandonment of long-held and historically validated principles has blinded many to the practical nature of what the evidence is saying. Many are simply cheering for the Treasury market’s demise as a way to reclaim their sacred worldview.

It is a worldview that I share, by the way; I take no joy in reporting these things, how the government can just borrow seemingly any amount without paying, literally, the price for being grossly irresponsible (and opening the door wide open for utter stupidity like MMT; we already have one group of “enlightened” bureaucrats telling the world they can manage the economy who have so utterly failed at doing so they’ve created the most fertile conditions for many to begin seeking an even more “enlightened” set of bureaucrats who will, they claim, fix the first mess). What I would like to happen doesn’t enter the equation. |

|

| What the bond markets are demonstrating is that it doesn’t matter what the Fed does. Go back to the height of the last reflation burst (which wasn’t high), back to October and November 2018. The Fed was hiking and running bonds off its balance sheet, and then UST’s started to catch that persistent bid anyway.The federal government was still racking up its deficits, and with Jay Powell, nowhere in sight, the banking system gobbled up every last bit that was offered nevertheless.

The “too many” Treasuries folks claimed that banks were and had been doing so because they were stuck, left with no other option; a statutory requirement to buy up what the feds sold no matter how disgustingly much. |

US Treasury and Auction Rates, Oct 2018 - Aug 2020(see more posts on U.S. Treasury, ) - Click to enlarge |

| Not only that, foreigners were also selling these things at an accelerating rate, apparently forcing banks to buy even more of them from their big overseas customers as a painful business courtesy.

And while all of that was true, it was only ever half the story. Less than half, really, because those things were, like the petroyuan, indicating something else than this emotionally driven bit of rationalized reverse engineering. The other half, the one with all the evidence, is what I wrote during that most “unexpected” Treasury rally:

Banks always had the option of selling their “unwanted” UST’s to the public in the secondary marketplace. While required by law to buy up paper sold at auction, there has never been any sort of restriction on what to do with the things after the auction gets completed. The financial system was always free, indeed encouraged, if what the “too many” Treasuries people said was true about how much trouble these were causing, to get rid of them! If being forced to hold these tarnished assets was a major problem in the repo, as many “experts” claimed, then there was every reason to pass them along with to the next sucker in line – the rest of the financial system and the public (more the former). Which the banking system could’ve easily done if it had ever wanted to. It didn’t once want to. And we know this for a fact. |

|

Even the guy everyone held up as the king of repo was finally forced to confess that, at least, banks were, yes, holding UST’s by choice. As I wrote back in December, these facts are indeed stubborn and Treasury prices both at auction and in the secondary market are the only facts.

|

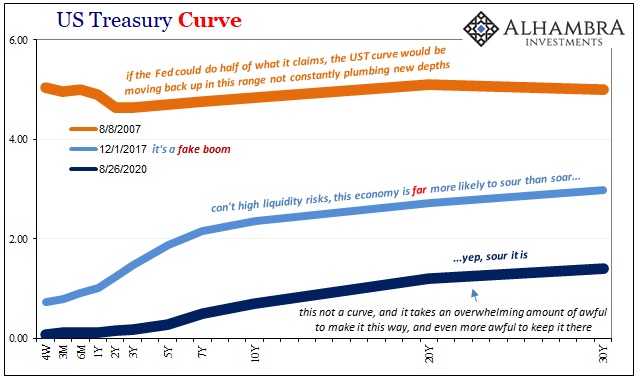

US Treasury Curve, 30 years - Click to enlarge |

| No, they really had chosen to hold that many bonds all along. It had never really made any sense to begin with, outside of more emotion than rational thinking:

And that’s right where we are now. The current curve is no longer inverted but only because the system experienced another GFC-level global dollar shortage spasm which has left it condensed down flat to an even more grotesque Japan-like state. This is no curve, not really, certainly not a natural one by any honest standard. It takes a whole lot of badness to distort it in such a way, and, more importantly, more such badness to keep it there. |

|

| Which means, again, overwhelming demand. The Fed does not factor; buying, running off, only buying T-bills (as during not-QE), only buying bonds and notes (during this QE6), these central bankers have inadvertently done us a favor by widely testing the premise varying these parameters if only to further rule them out.Here’s the thing: if the market really believes the Fed is required in order to keep rates low then the BOND ROUT!!!! would be taking place right now. Before right now; months ago. If Jay Powell (this guy) was truly the only thing standing between keeping rates low and the idea that demand has been only him, then the UST market would’ve put in a disaster already (1994-95 to shame).

But like the last “too many” Treasuries theory, yields are rangebound in a very narrow range at an extremely low level, prices still sky-high because demand hasn’t changed. |

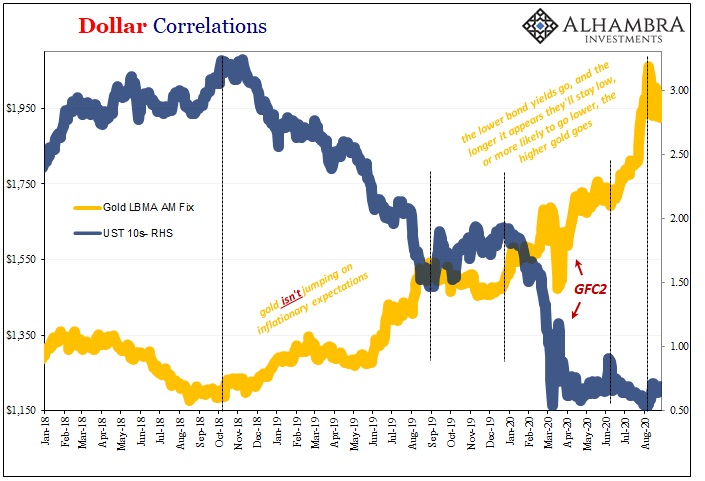

Dollar Correlations, Jan 2018 - Aug 2020 - Click to enlarge |

And demand hasn’t changed because the Fed is not a central bank.

Even the gold market agrees.

Full story here Are you the author?Tags: Bonds,collateral,commodities,currencies,economy,Featured,Federal Reserve/Monetary Policy,federal-reserve,Gold,jay powell,Markets,newsletter,Notes,QE,repo,T-Bills,U.S. Treasuries