Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

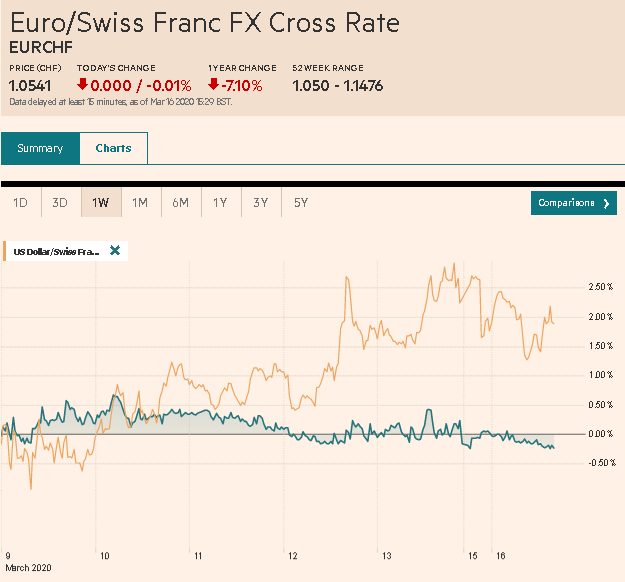

Swiss FrancThe Euro has fallen by 0.01% to 1.0541 |

EUR/CHF and USD/CHF, March 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The Federal Reserve and central banks in the Asia Pacific region acted forcefully, but were unable to ease the consternation of investors. The Reserve Bank of New Zealand cut key rates by 75 bp. The Bank of Japan appears to have doubled its ETF purchase target to JPY12 trillion, and the Reserve Bank of Australia is preparing for new measures that will be announced Thursday. The Fed returned to the zero-bound, resumes long-term asset purchases, and took other measures to boost funding for banks. The price of accessing the dollar-swap lines the Fed keeps with several major central banks was halved to 25 bp over overnight index swaps from 50 bp. All the action and the 9%+ rally the US before failed to stem the tide. Most Asia-Pacific bourses were down 3%-6%, and Australia bled more than 9% after losing almost 11% last week, led by energy, industrials, financials, and real estate. The Dow Jones Stoxx 600 crashed nearly 18.5% last week and is nearly 8% in late morning turnover, led by industrials, consumer discretionary, and financials. The S&P 500 is limited down in electronic trading. Benchmark yields are mixed. Australian, and especially New Zealand yields fell, though the yield on Japan’s 10-year yield firmed slightly. In Europe, periphery bonds are under pressure, where the yield is up around 13 bp. France is seeing its premium rise against Germany too. The US 10-year yield is slipping below 77 bp. Last week it fell to almost 55 bp. The dollar is mixed. The dollar-bloc currencies and the Norwegian krone are lower. he Bank of Canada and Norway’s Norges Bank cut rates by 50 bp before the weekend. The yen and Swiss franc are up more than 1.75% and nearly 1%, respectively. Most emerging market currencies are lower, led by more than 2% losses in Russia, Mexico, and South Africa. Gold’s early gains have dissipated and is extending last week’s near-record decline. It appears poised to possibly break below $1500. May WTI is off by 6% to approach $30 again. |

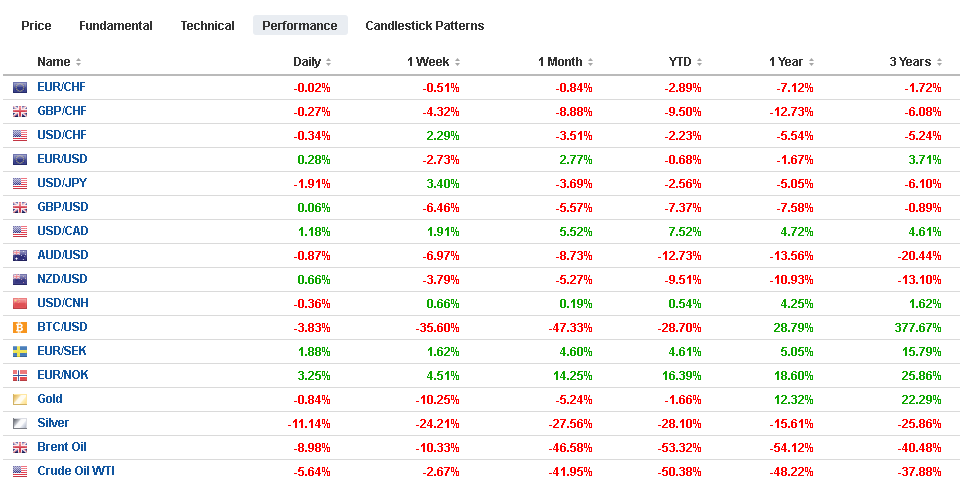

FX Performance, March 16 - Click to enlarge |

Asia Pacific

The BOJ’s doubling of its ETF target was the largest measure that Governor Kuroda announced, but he also indicated the purchases of corporate bonds will be increased too. A new zero-rate loan facility was also unveiled. As officials consider other steps, it should consider suspending the sales tax increase that went into effect last October. Abe had indicated at the time that only a Lehman-like event would persuade him to delay that tax increase, which had developed a political lift of its own outside of the fiscal goals.

The Reserve Bank of New Zealand announced a dramatic 75 bp rate cut before the markets opened to bring the cash rate to 0.25%. Once the news wires indicated that an announcement was pending, the Kiwi was marked down to about $0.5945 from last week’s settlement of about $0.6135. The other dollar-bloc currencies fell, but not nearly as much, and recall that the Bank of Canada surprised the market with a 50 bp cut before the weekend. The RBNZ also suspended for at least a year new capital requirements on banks, which would have tied up around NZ$47 bln. The central bank was clear that if additional monetary moves are necessary, it envisions asset purchases rather than negative rates. The government will announce new fiscal measures tomorrow. Separately, Australia, which cut rates on March 3, indicated it would make extra liquidity available in its funding markets.

Chinese data was horrific. The economic figures in February were considerably worse than expected and point to a dramatic contraction underway. Bloomberg economists estimate the economy may have contracted by 20% year-over-year in the January-February period. February industrial output fell 13.5%. Retail sales were off 20%, and fixed asset investment plunged by 24.5%. Unemployment, which was at 5.2% at the end of 2019, jumped to 6.2% in February.

After spiking to almost JPY108.50 ahead of the weekend, the dollar slumped to JPY105.75 in early turnover today. It firmed to about JPY107.55 later in Asia before drifting lower again in Europe. Initial support is seen in the JPY104.50-JPY105.00 area. The Australian dollar is extending its slide into the sixth session today. It recorded new lows for the move, a little below $0.6100. It looks like it is trying to carve out an intra-day bottom, but at around $0.6180, it is off about 0.35% after last week’s 6.5% plunge. The New Zealand dollar fell to about $0.5945 on the surprise rate cut. It recovered and is little changed in the European morning near $0.6050. The Chinese yuan was steady in narrow ranges inside last Friday’s range, which was inside the previous day’s range. The dollar was confined to about 80 pips on both sides of the CNY7.0 level. Lastly, the dollar traded at new four-year highs against the Korean won, after the surprise rate cut (~KRW1226).

Europe

More of Europe imposed lockdowns, including Ireland, Spain, Austria, and Norway. Italy and France had already done so. The virus continues to ravage the Continent. Cases in Spain jumped 35% yesterday, and the number of fatalities doubled. Switzerland saw more than a 60% jump in the number of infected people. In Italy, fatalities rose by more than 25%.

There is talk that the ECB could reactive its OMT facility (outright market transactions) to help support the peripheral bond markets, where yield spreads have widened sharply. The divergence in rates disrupts the transmission mechanism of monetary policy. Besides a stigma associated with the program, countries balk at the conditionality that is imposed, namely, austerity. However, under current conditions, the conditionality may be minor and surely not budget cuts or tax increases now. ECB President Lagarde misspoke about the diverging spreads last week. Although it was corrected and the spread between Italy and German narrowed ahead of the weekend, the market pressure remains acute as risk assets are shunned, and peripheral European bonds are seen as such.

The ECB’s asset purchases, which now are around 33 bln euros a month, are less than half of the amount being bought at the peak of the sovereign crisis and can be scaled up. The ECB has to self-imposed caps, one is the capital key, which is a function of the size of the member’s economy, and the other is a 33% issuer limited. While there is some flexibility around the capital key, it 33% issuer limit, which is not pressing now for Italy, for example, can be waived in an emergency. This would seem to qualify.

The euro has traded on both sides of its pre-weekend range (~$1.1055-$1.1220). The high was recorded in Europe, but the upside momentum stalled, and a move back toward $1.1100 in North American session is possible. Initial support may be seen near $1.1150. Sterling is struggling to sustain even modest upticks. Recall that before the weekend, it peaked around $1.26 before slumping to $1.2265. It made a low by $1.2250 in Asia before recovering to $1.2425 but is on its back foot in the European morning. A break of $1.22 would encourage a test on $1.20.

America

The Federal Reserve went all-in before the markets opened earlier today in Asia. It slashed the fed funds rate by 100 bp to bring the target to the zero-bound (0-0.25%) and announced a new asset purchase plan ($500 bln of Treasuries and $200 bln of mortgage-back securities. It removed capital reserve requirements and, in conjunction with other central banks, reduced the cost of the currency swap lines to only 25 bp on top of OIS rather than 50 bp. The interest on reserves chopped to 10 bp, a cut of 100 bp. Banks will be allowed to borrow from the now-25 bp discount window for up to three months. Cleveland Fed’s Mester cast the lone dissenting vote, preferring a 75 bp rate cut. The Fed’s statement indicated rates would remain near zero until officials were convinced the economy had “weathered the storm,” which some say may not be known until next winter. In any event, low for longer.

The Fed’s move preempt and replace this week’s FOMC meeting. No updated forecasts (Summary of Economic Projections–“the dot plot) will be provided. Fed Chair Powell was clear that the situation is too much in flux for such forecasts, though he acknowledged that Q2 will be quite weak. The large-scale action announced three days ahead of the scheduled meeting is seen as a signal that the Fed is bracing for some exceptionally negative news and developments. While there will not be an FOMC meeting this week, Powell is expected to hold the scheduled press conference. During the Great Financial Crisis, the Fed often seemed to want to keep separate monetary policy proper from other measures. The press conference may provide a forum to announce re-opening facilities to support commercial paper and maybe asset-back securities issuance.

The G7 will hold a video conference call today. Given steps announced by a number of countries, it begs the question of what is left to coordinate and why the plethora of measures was not announced together. We suggested three areas that do lend themselves to coordination. A bank holiday that would close the markets, a ban or limits on short-selling (which South Korea introduced for six-months) and foreign exchange intervention. None seem particularly likely. Mnuchin seemed to rule out a coordinated market shutdown, but the cost-benefits are arguable changing. The Fed announced the cut in the swap lines with other central banks (to 25 bp on top of overnight index swaps, rather than 50 bp). This could have been announced after the G7 call instead of by the Fed, which suggests the still shallowness of the cooperation. News that the US was trying to buy a German company that is working on a vaccine has further antagonized the US-Europe relationship. In an unusual step, the EU rebuked the US last week for its unilateral imposition of travel restrictions with Europe, which were not preceded by consultations or notification.

The US dollar initially continued to pullback against the Canadian dollar after reaching almost CAD1.40 before the weekend and before the Bank of Canada’s emergency 50 bp rate cut. The greenback, however, has bounced off CAD1.3735 and is back straddling CAD1.39 in the European morning. Given the drop in oil prices and the broader de-risking, a retest on the CAD1.40 area cannot be ruled out. That is more or less the story of the Mexican peso too. The US dollar pulled back after reaching a record high near MXN22.50 and found support near MXN21.37. It is recording an outside up day and is rechallenging the MXN22.50 area. It is in uncharted waters, but the next target being discussed is around MXN23.50.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Bank of Japan,COVID-19,Currency Movement,ECB,EUR/CHF,federal-reserve,newsletter,RBNZ,USD/CHF