Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

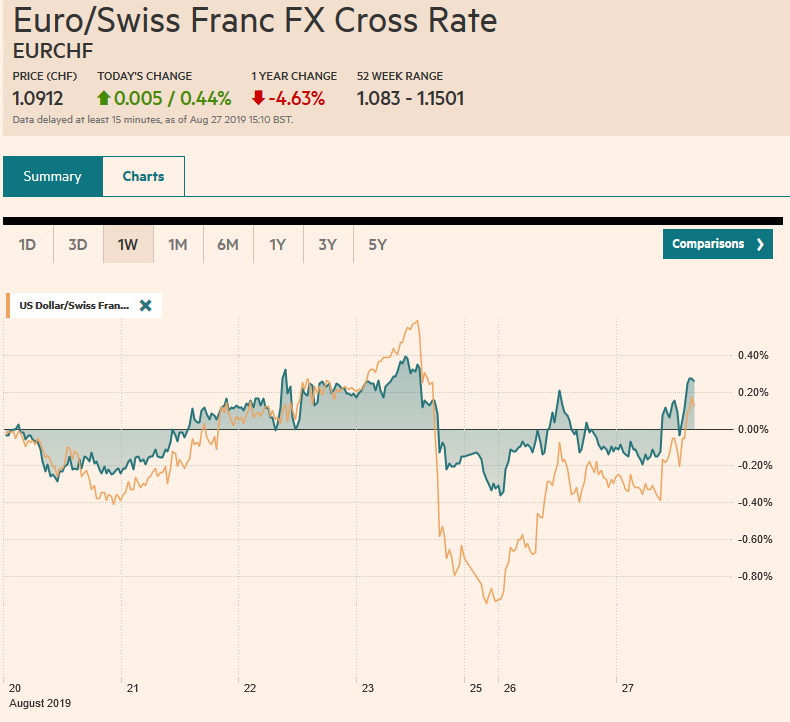

Swiss FrancThe Euro has risen by 0.44% to 1.0912 |

EUR/CHF and USD/CHF, August 27(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Hope triumphed over realism yesterday, and realism is fighting back toward. Asia Pacific markets, however, traded on the echo from the recovery in North America on Monday. The MSCI Asia Pacific recouped part of yesterday’s drop, led by Chinese markets. Hong Kong was the main exception. The enthusiasm faded by the European morning and the Dow Jones Stoxx is threating a fourth consecutive losing session, dragged down by communication, consumer staples, and health care sectors. US shares are trading lower in Europe, and the early call is for the S&P 500 to open about a little lower. Bonds yields edged higher in the Asia Pacific but are coming in lower in Europe. Hopes of a Five Star/PD government has sent Italian bonds sharply lower, though no deal has been announced and the early gains have been pared. The dollar is trading mixed, with the Antipodean currencies off about 0.3% and the yen and Swedish krona are battling for top honors and are up about 0.3%. The liquid and freely accessible emerging market currencies are trading 0.2%-0.4% lower. |

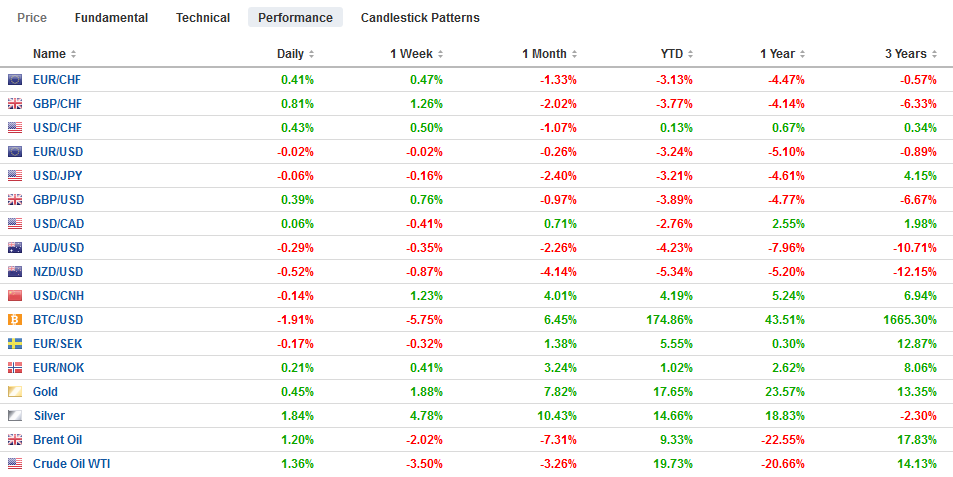

FX Performance, August 27 - Click to enlarge |

Asia Pacific

The PBOC set the dollar’s reference rate at CNY7.0810. A Reuters survey found a median forecast for CNY7.1055 This illustrates that the PBOC continues to temper the market pressure. The pressure remains, and the dollar is trading above CNY7.16 in late mainland dealings. The offshore yuan is weaker still, and the dollar is a little below CNH7.18. It is the ninth consecutive decline for CNY. Separately, China reported a 2.6% rise in July industrial profits after a 3.1% slump in June. Year-to-date, profits are off 1.7%.

Some observers are looking at how China responded to the latest round of US tariffs and are concluding that it is running out of leverage. We think this is mistaken. First, there are more commercial steps China could take, including targeting US companies for which there is a strong European alternative, such as aircraft. It could also expand the list of companies on its “unreliable entity list.” Second, and more importantly, if the US dominates the trade escalation ladder, and we assume a rational actor, then China could be expected to move to a different escalation ladder.

Two developments in Japan are noteworthy. First, Trump conditioned his decision not to levy new auto tariffs on Japan by reserving the right to do so in the future. This does not sit well with Japanese officials, and they will seek to block this in the final agreement expected next month. Second, South Korea indicated that if a rapprochement with Japan can be struck before the current intelligence-sharing pact ends on November 23, it can be renewed. The tension between the two remains high.

Yesterday’s dollar gains against the yen are being halved today. The session high is near JPY106.20 compared with JPY106.40 yesterday. It trended gently lower through Asia and found support near JPY105.60 in late Asia and in the European morning. We suspect it will struggle to rise above JPY106.00, where a $1.2 bln option is set to expire today. The next area of support is seen near JPY105.30. The Australian dollar traded on both sides of the pre-weekend range but failed to close above the previous high, and this neutralized the bullish impulse. The Aussie has been confined to the upper half of yesterday’s range and drifted toward $0.6750. The intraday technicals suggest it may be finding support today ahead of the North American session.

Eurozone

Merkel may be among the most astute politicians of our day, but that day is drawing to a close. The fiscal austerity asphyxiated public investment and allowed the infrastructure to deteriorate. Politically, she has overseen the weakening of the center, and this may be driven home in the weekend state elections in Saxony and Brandenberg. Like the federal government, Saxony is governed by a CDU-SPD coalition. The CDU has been part of Saxony’s government for 30 years. Brandenberg, in the east, has seen an SPD-led government since unification in 1990, and in the past 10-years, it has been in a coalition with Left Party. The polls give the nationalist, anti-immigration party, the AfD in both Saxony and Brandenberg. There would likely be national ramifications for an AfD victory. A poor showing for the CDU could force Merkel to reconsider her succession planning as her hand-picked successor AKK (Annegret Kramp Karrenbauer)’s was already beginning to look strained. The CDU may shift to the right to try to capture the defectors to the AfD. In Brandenberg, which surrounds the capital, the SPD could come in fourth place behind the AfD, CDU, and Greens. Such results would rally those forces that want the SPD to pull out of the national coalition with Merkel’s CDU, which if successful, would trigger a political crisis.

It is Italian politics, though, that is front and center today. The Five Star Movement (M5S) and the center-left PD are in talks to form a coalition. There seem to be two stumbling blocks. M5S is insisting on Conte remaining Prime Minister, and the PD is insisting that M5S accepts its 2020 budget proposals. The issue is whether their desire not to risk an election now that could see a right coalition led by Salvini take charge is greater than their animosity for each other. From the outside, it looks like a close call.

UK Prime Minister seems to be touting the possibility that the EC is softening its position on Brexit. However, it seems like a case of hearing what one wants. France’s Macron has been explicit. EU negotiator Barnier is authorized to make only technical modifications to the agreement. Besides rejecting the backstop, the Johnson government has still not offered concrete alternatives. PredictIt.Org is showing about a 50/50 chance of an election called by the end of October and leans 52/48 to the UK leaving at the end of October.

The euro is steady in a narrow 20-tick range around the middle of the two-day range, a little above $1.1100, where a 1.3 bln euro expires tomorrow. We suspect the euro will find offers in front of $1.1130, leaving the option for nearly 510 mln euros at $1.1155 out of play ahead of its expiration today. Sterling is holding above $1.22 as it did yesterday, but the upside has been capped near $1.2260 compared with $1.2285 yesterday. If the high of the day is not in place, we suspect it came close.

United States

Investors are concluding that US President Trump is very sensitive to the stock market gyrations and in the face of the pre-weekend slide, he tempered his rhetoric. In four areas, he seemed to have softened his tone. The “phone call” from China was one such signal, but Trump also suggested that under the right conditions, he would meet with Iran’s President. A compromise was found on the digital tax with France, and Trump retreated from his threat to raise the tariff on French wines. The framework of an agreement with Japan was struck and, as noted above, Trump ruled out extra tariffs on Japanese auto and part imports.

US economic data today consists of house prices, the Richmond Fed’s August manufacturing survey, and the Conference Board’s consumer confidence. Even in the best of times, these reports typically do not move the markets. The API estimate of US oil inventory will be reported late in the session, and a decline (2.25 mln barrels) are forecast for the government’s estimate tomorrow. October WTI is trading firmer to threaten a four-day nearly 5% slide in prices. Canada’s economic calendar is bare, while Mexico will report July trade balance (expected to slip back into deficit) and unemployment (forecast to tick up).

An IMF team is in Argentina to assess the situation ahead of a $5.3 bln tranche of its package. Such a review is now required before each installment on such large packages (the IMF granted Argentina a record $57.1 bln loan package a little less than a year ago, to be disbursed over the following three years). Argentina has appeared to be on track, from the IMF’s point of view, until the recent response to the election results, in which President Macri’s austerity was rejected. The drop in the peso and the jump in interest rates means that the market no longer has confidence that another debt restructuring can be avoided. Government bonds maturing in 2028 were trading around 50 cents on the dollar yesterday. Macri appears to be capitulating and promised to lower workers’ income taxes and the sales tax on necessities and boost welfare subsidies. Rather than run a primary budget (excluding interest rate payments), Fitch estimates that Argentina may have a 1% deficit. If the IMF decides to disburse the funds, it may not avoid a restructuring, but it can buy some time. If the IMF does not make the payment, Argentina forces a restructuring (which is what happened in 2001). The hurdle around the corner for Argentine is in Q2 20 when official data shows that a $20 bln debt payment is required (up from $5.6 bln in Q1 20). Today Argentina short-term peso and dollar debt that needs to be rolled. If the $1.6 bln (Letes) debt fully rolled over, then is precious reserves will be drawn down further. If the ARS50 bln (~$905 mln) is not fully rolled, then some of that liquidity may look to move into dollars, weighing directly on the currency.

The US dollar closed yesterday below its 20-day moving average against the Canadian dollar for the first time since July 19 yesterday, and there has been follow-through selling today. The greenback is at two-week lows near CAD1.3230. Initial resistance is seen now by CAD1.3250. However, headway below the figure may be difficult with a large $1.3 bln option struck there (CAD1.32) that expires today. Meanwhile, the US dollar continues to straddle the MXN20.00 level. It had pushed above MXN20.12 yesterday but closed a little below MXN20.00. The dollar is also at its best level of year against the Brazil real, reaching almost BRL4.17 yesterday. Last year’s high, recorded in August, was near BRL4.2150, and represents the next major target.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,ARS,Currency Movements,EUR/CHF and USD/CHF,Germany,Italy,newsletter