Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

It’s the last week of August. Several economic reports will be released in the coming days. They include the US deflator of consumer expenditures that the Federal Reserve targets, China’s PMI, and the eurozone’s preliminary August CPI. It is not that the data do not matter, but investors realize the die is cast.

They are looking further afield. The next US tax increase on Chinese imports goes into effect on September 1, and Beijing has threatened to retaliate. The Federal Reserve and the ECB will ease policy in the coming weeks. The twice-delayed Japanese sales tax hike will be implemented in about five weeks.

A cartoon I saw recently seems to capture the sentiment in the market at the moment. One person was carrying a sign like the “end is nigh” and another person complains about the optimism, that this could last forever. Whether it is the protest in Hong Kong, negative interest rates, or the US-China trade conflict, many think the status quo is unsustainable, and others believe it can persist as in a “new normal.”

Paradoxically, both may be true. The market may have gone too far in the short-term, but it does not mean a return to the status quo ante. Some suspect that the collapse of Argentina’s 100-year bond that was oversubscribed when it was sold in 2017 ($9.75 bln of bids for the $2.75 bln offering) and the poor reception to Germany’s sale of a zero-coupon 30-year bond (which based on pricing was tantamount to a yield-to-maturity of -11 bp), is a turning point. It also coincides with a ratchet up in the decibel of arguments that monetary policy is exhausted and fiscal policy is required.

The poor data from northern Europe, and especially the slump in Germany, are fanning hopes that the purse strings will loosen. The Bundesbank acknowledged that the Germany economy may be contracting in the current quarter, which would be the third of the past five quarters. The year-over-year pace has been below 1% for the past three quarters. Germany is moving to end the Solidarity Tax for most, but there still is a reluctance to do anything meaningful in terms of new stimulus, which, as of last week, the Bundesbank thought unnecessary. Yet, even the amount that the German SPD Finance Minister suggested (~50 bln euros) seemed like a rounding error for the roughly 3.4 trillion euro economy.

In our big-picture narrative (See Political Economy of Tomorrow), the Great Financial Crisis was the end of strategy (cash register) lead by Reagan and Thatcher to overcome the economic challenges (stagflation) of the 1970s. We are in an interregnum period. The old has fallen before the new arises. The parallel is when Nixon unilaterally ended the dollar’s last ties to gold 48-years ago this month and announced wage and price controls. Little did anyone know that the Reagan-Thatcher strategy would take everyone in the exact opposite direction.

In this interregnum period, economists, investors, and armchair quarterbacks bounce between advocating monetary and fiscal policy to address the challenges. If monetary policy has been over-relied on in recent years, it is that many previously argued fiscal policy was exhausted. How can a debt crisis be addressed by more debt, cried a common refrain?

We are in between, and in that vacuum, economic nationalism stepped up. It could be a place holder, and perhaps it may not be clear until after 2020. Although the US does not have a monopoly on economic nationalism, a re-embracement of the multilateralism could go a long way toward arresting this movement. On the other hand, there is no reason that the next strategy must be in the liberal internationalist tradition.

China had put investors on notice that it would take action if the US escalated the trade conflict, and ahead of the weekend, it did just that. Like the US, it announced a set to begin on September 1 and another to be levied in mid-December. US crude oil and soy will be taxed by an extra 5% starting next month, for example, while the 25% tariff on US cars that had been previously suspended would be re-instituted. Some models would be hit with an additional 10% tax, in mid-December. All told, some US vehicles will have as much as a 50% tariff.

Investors voted with their wallets before the weekend in the same way they responded to the tweeted ended of the second tariff truce to start the month. The knock-on effect on the US economy is understood to mean slower growth, boosting risk of a recession, and dragging interest rates lower. The growth concerns and disruptive trade impulses weigh on equities more than lower interest rates help. The dollar weakens.

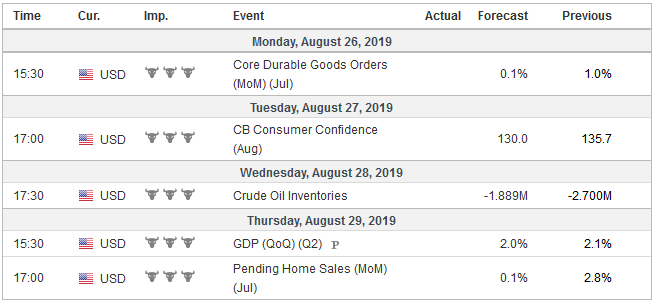

United StatesIn some ways, the US trade policy is driving Fed policy expectations. The Fed sees its job as sustaining the economic expansion by striving toward full employment and 2% PCE deflator (1.4% in June and July is due on August 31). Currently, the economy continues to appear to be growing around what the Fed forecasts suggest is trend (i.e., non-inflationary) growth. The labor market remains robust, and the decline in weekly jobless claims last week is notable because it covered the same week that the non-farm payroll survey was conducted. Consumption looks vigorous and July consumption expenditures, to be reported at the end of next week, are expected to have risen by 0.5% on the month. There are some signs of manufacturing weakness (the Aug flash PMI slipped to 49.9 from 50.0), and there are admittedly pockets of weakness, like business investment. The biggest risk to the expansion is the unintended but not unforeseeable consequences of the US trade policy. Prior to Powell’s speech and the presidential tweetstorm, the market had pulled away from its extreme aggressiveness. It has pushed the implied yield of the January 2020 fed funds futures 20 bp higher as the market moved away from expectations for three more cuts this year. However, following Trump’s aggressive tweets, the implied yield fell from 1.58% to 1.465%. The swing in policy expectations reflects a broad understanding of the Fed’s reaction function. It would be responding to the materialization of the risks it clearly recognized. |

Economic Events: United States, Week August 26 - Click to enlarge |

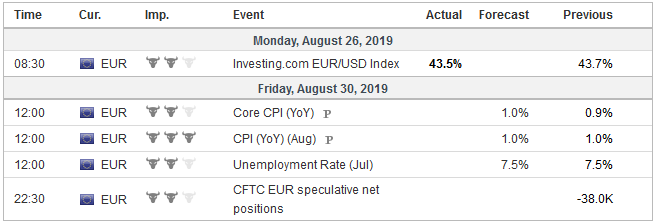

EurozoneThe European Central Bank may want to take a different approach. It sees its credibility on the line. It must demonstrate it can achieve its single mandate for close to but below 2% CPI over the medium-term. The preliminary estimate for August CPI may see both the headline and core rates converge at 1.0%. The problem so defined lends itself to a solution: jump ahead of market expectations, which operationally may mean shock and awe. However, it is more difficult done than said. The instruments are well known (rates, and possible tiering, asset purchases, loans, forward guidance), and the quantities are seen as limited. |

Economic Events: Eurozone, Week August 26 - Click to enlarge |

ChinaChina has had plenty of opportunities to ease monetary policy, including the re-animation of its prime loan facility. The fact that it has not does not mean it won’t, but it seems to reflect a lack of urgency, to say the same thing a bit different, it seems that officials have other priorities. The yuan has weakened against the dollar for the past seven sessions. The downside momentum appeared to have eased as the dollar approached CNY7.10. However, the escalation of the trade conflict saw the dollar rally against the offshore yuan (~CNH7.14), as the greenback weakened against the major currencies and strengthened against emerging market currencies. The risk is for further yuan weakness in the coming days, though the after a certain level, we suspect tariffs will be more symbolic than substantive. For example, a 25% tariff may make an imported good uncompetitive. Raising the tariff to 30% will likely have marginal impact. |

Economic Events: China, Week August 26 - Click to enlarge |

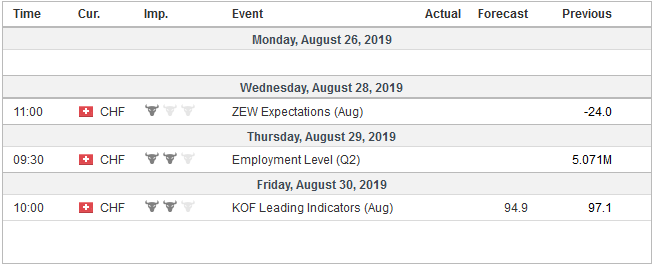

SwitzerlandThe pre-weekend escalation of the conflict saw triggered a sharp sell-off in US shares and a dramatic drop in interest rates. This will likely carry over into next week’s price action. The Japanese yen and Swiss franc were the strongest currencies. The Swiss National Bank appears to have been intervening in recent weeks, but besides warning that the MOF was watching yen movements closely a couple of weeks ago, Japan has been quiet about the yen’s appreciation. However, should the dollar fall through the JPY105 area, their protests may increase as the next main level is JPY100. Emerging markets, which typically do better with stronger prospects for the world economy, will continue to be shunned. The JP Morgan emerging market currency index fell to new lows for the year ahead of the weekend. The MSCI Emerging Markets equity index has fallen a little more than 6% this month and finished poorly ahead of the weekend. |

Economic Events: Switzerland, Week August 26 - Click to enlarge |

The week ahead is about the echo from this past week and the siren’s song of September.

Tags: #USD,$CNY,$EUR,Federal Reserve,newsletter,Trade