Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

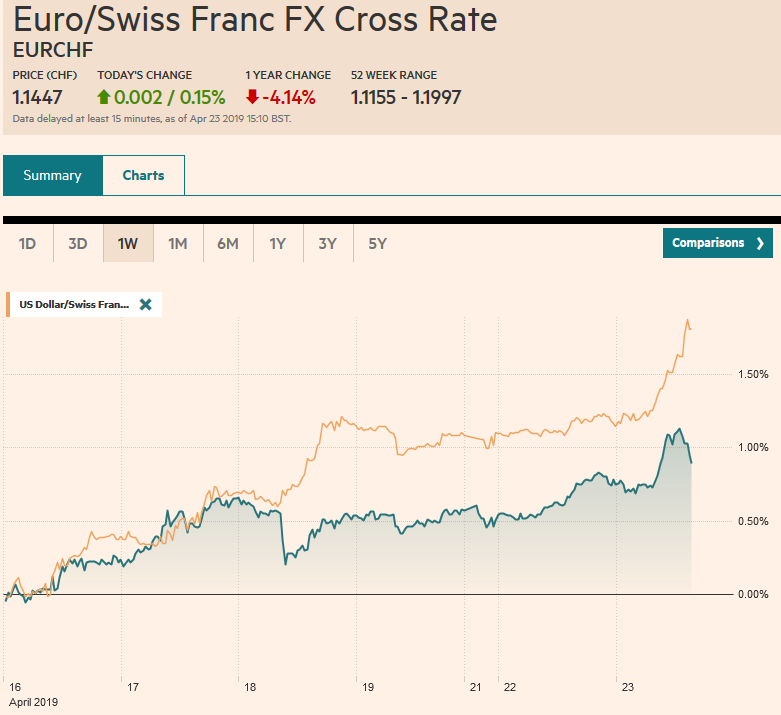

Swiss FrancThe Euro has risen by 0.15% at 1.1447 |

EUR/CHF and USD/CHF, April 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Financial centers that have been closed for the extended holiday have re-opened, but the news stream is light and market participants are digesting developments and positioning for this week’s central bank meetings and the first look at Q1 US GDP. The US decision to end exemptions to the embargo against Iran led to a surge in oil prices, which are extending gains to new six-highs today. Equities are mixed, and there is some concern that investors in China got a bit ahead of themselves. While more equity markets rose in Asia, China was an exception. The Shanghai Composite slipped 0.5% but was lower for the third session of the past four. European markets are mostly lower as financials (many banks report earnings this week), materials, and industrials are offsetting the gains from energy and health care. US shares are little changed. Benchmark 10-year yields fell in five basis points in Australia ahead of tomorrow’s Q1 CPI. China’s 10-year yield slipped a couple of basis points. European bond yields are mostly two-three basis points higher, though Italy’s benchmark is up nearly six basis points. The dollar is higher against most of the major currencies, with sterling the notable exception. Emerging market currencies are under modest pressures, though the rise in oil prices continue to underpin the Russian rouble. |

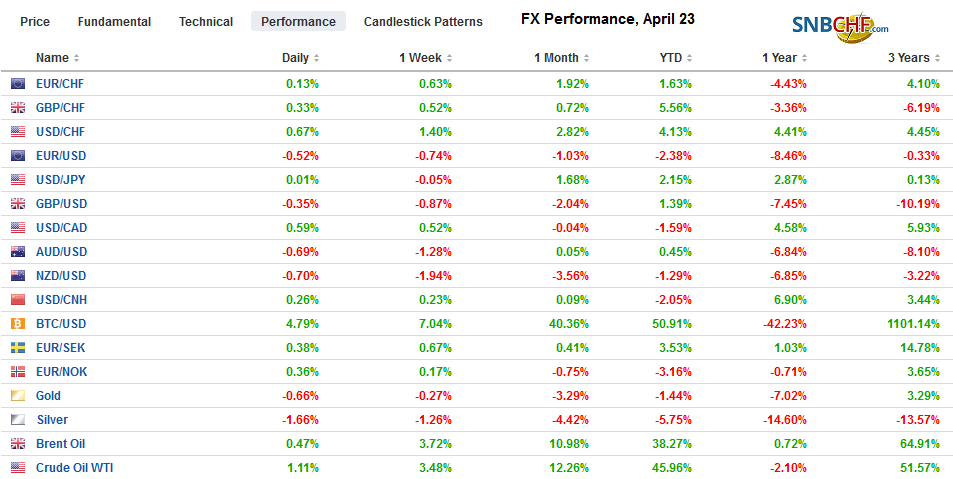

FX Performance, April 23 - Click to enlarge |

Asia Pacific

The main events lie ahead. Australia’s CPI is due early Wednesday in Sydney. Consumer prices rose 0.5% in Q4 and are expected to have risen by 0.2% in Q1. If true, this would see the year-over-year rate slip to 1.5% from 1.8%. The underlying rates also are expected to have eased. Softer price pressures will encourage expectations for a rate cut this year. Interpolating from the OIS, a rate cut looks to be mostly discounted in Q3. The implied forward seems to have priced in a reduction by October.

The BOJ begins its two-day meeting tomorrow. Despite better US and Chinese data, Japan appears to be a laggard. Japan will report its All Industries Activity Index tomorrow. It is a proxy for monthly GDP, and it is expected to have slipped 0.2% in February, the same as in January. The economy appears to have contracted by 0.3%-0.5% in Q1. While the BOJ is not expected to change policy, it may downgrade elements of its economic assessment. The real estate market was the subject of some concern in the recent financial stability report, and BOJ Governor Kuroda is expected to discuss it in his press conference after the BOJ meeting.

On his way to the US, Abe will meet with Europe’s Tusk and Juncker. Japan and the EU’s free-trade agreement went into effect at the start of February. Abe is to visit Washington with Finance Minister Aso to ostensibly formally launch trade talks. Although Abe has tried ingratiating himself to Trump, the strategy has not born much fruit. The steel and aluminum tariffs remain in place. Japan was not granted a new waiver to buy Iranian oil. The US continues to threaten tariffs on auto imports. The US two early asks seem to be uncontroversial. First, the US wants to ensure its agriculture is on the same playing field as others that Japan has struck a new trade agreement with, like the EU and TPP. Second, as the US did with NAFTA 2.0 and reportedly in the trade deal with China, sought protections against currency manipulation. Recall that after Abe was elected, the G7 had him sign a new commitment to market forces determining exchange rates.

The dollar was sold in early Asia, and that is when it touched a seven-day low near JPY111.65. After straddling JPY112 last week, it has not traded above there this week. There is a roughly $640 mln option struck there that expires today, and more in the coming days. Expiring options for nearly $1.2 bln are protecting the downside (JPY111.50-JPY111.65). The month-long uptrend remains intact, though a close below JPY111.50 would threaten it. The Australian dollar briefly poked above $0.7200 in the middle of last week. Today is it traded near 10-day lows a little ahead of $0.7100, which is the middle of the two-cent range it has been mostly confined to for the past two months. Important support is seen near $0.7080, and we expect a near-term test on it.

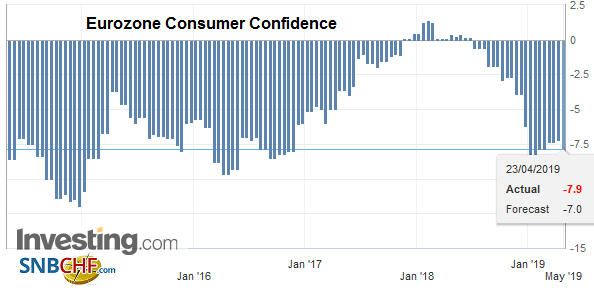

EuropeIf weak growth and price pressures push out the first ECB rate hike, then Draghi’s suggestion to look into the implications of the persistence of negative rates for long seems is reasonable. The initial focus seemed to be on tiering. This would be to exempt some deposits at the ECB of the full minus 40 bp rate. Several central banks with negative deposit rates have some kind of tiering system. In EMU, with the southern banks more likely the beneficiaries of a new targeted long-term refinancing operation (TLTRO), perhaps Draghi felt the need to secure support from the northern members, who typically have the excess reserves that are hit with the negative deposit rate. However, it seems as if there is little enthusiasm to tier the negative deposit rate in the eurozone. That said, European banks are reporting Q1 earnings figures in the coming days, and the interest rate margin is likely one of the headwinds many face. |

Eurozone Consumer Confidence, April 2019(see more posts on Eurozone Consumer Confidence, ) Source: investing.com - Click to enlarge |

With the end of the holiday, cross-party talks between the Tories and Labour resume in the UK. The main development in recent days is that the pressure on May to resign appears to be increasing. Reports suggest a group of 800 highest ranking Conservatives will meet shortly and conduct a non-binding poll of support for the Prime Minister. Recall that May survived a vote of confidence within the party at the end of last year. The rules prevent another vote within 12 months. Many of the Tories who argue that a new referendum is an insult to democracy apparently had no problem voting on the Withdrawal Bill three times and not threaten to change the party rules to challenge May again. The next immediate hurdle is the May 2 local elections. A sharp defeat for the Conservatives may give Labour less incentive to reach an agreement. Without an agreement, the UK will participate in the EU Parliament elections. While Farage’s new party appears to be doing well, Labour could emerge as an essential force in the EU elections and help decide the configuration of the next European Commission.

Despite the end of the holiday, the euro has been confined to about a 10-tick range on either side of $1.1250, where an option for 1.9 bln euros expires today. The euro bottomed last week after the diverging economic news of disappointing EMU flash PMI and a surge in US retail sales near $1.1225. The corrective targets are in the $1.1265-$1.1285 area. After not closing below $1.30 since February 18, sterling has done exactly that for the past three sessions. We have been reluctant to embrace this as a breakout. A close above $1.30 today would help lift the technical tone. Note that there is a modest GBP280 mln option struck at $1.30 that will be cut today.

United States

|

U.S. New Home Sales, March 2019(see more posts on U.S. New Home Sales, ) Source: investing.com - Click to enlarge |

The US decision to end exemptions to the embargo against Iran has renewed the rally in oil prices. Taiwan, Italy, and Greece had the waivers for the past six months but did not use it. They did not import Iranian oil, and so the end of the waivers mean little. Japan and South Korea have already lined up alternatives according to reports. For Turkey, this is just another flashpoint of conflicting interests with the US. China and India may be squeezed the most. Although the US wants to cut Iranian oil exports from 1.1 mln barrels a day that it averaged in the first half of the month, with efforts to circumvent the US sanctions, many suspect that a little more than half of Iran’s oil will be impacted. Meanwhile, Saudi Arabia and UAE, the real swing producers in OPEC, could boost output by as much as 1.4-1.5 mln barrels a day if needed. This will likely be the key issue at next month’s OPEC+ meeting.

The US dollar remains in a CAD1.33-CAD1.34 trading range. Ahead of tomorrow’s Bank of Canada meeting, players may have little incentive to break the range. The range also may be reinforced today by the option for nearly $630 mln at CAD1.34. The dollar appears to be carving out a bottom against the Mexican peso. A move above MXN19.00, last week’s high and the 20-day moving average, would lift the greenback’s tone.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Bank of Japan,Brexit,EUR/CHF,Eurozone Consumer Confidence,FX Daily,newsletter,OIL,U.S. New Home Sales,USD/CHF