Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

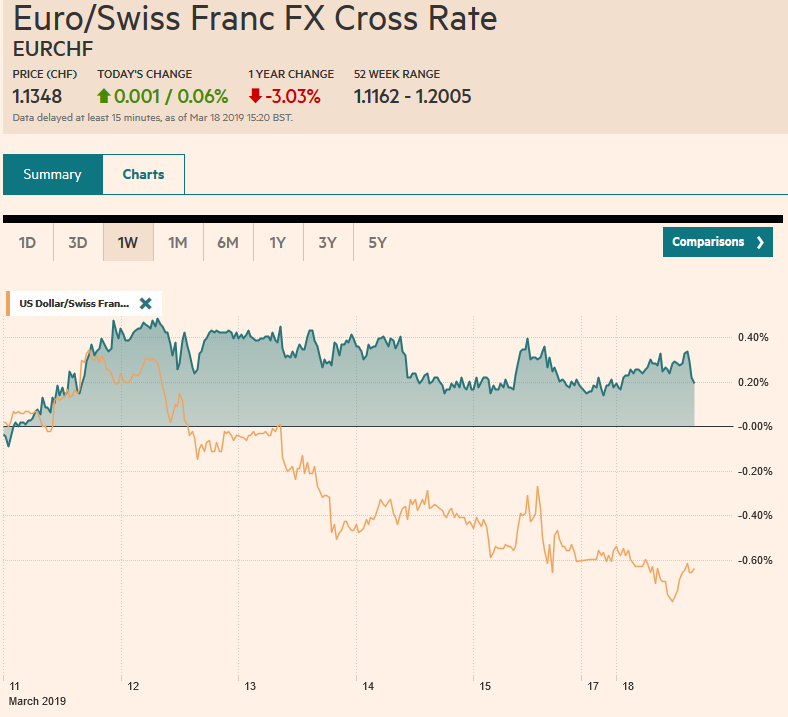

Swiss FrancThe Euro has risen by 0.06% at 1.1348 |

EUR/CHF and USD/CHF, March 18(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The eventful week has begun off slowly. After Wall Street’s best week in four months underpinned Asian’ equities, where all the markets but Thailand, advanced, led by the nearly 2.5% rally in Shanghai. Note that New Zealand’s S&P/NZX 50 rose to new record highs. European bourses are firmer, and the Dow Jones Stoxx has edged to a new high for the year, with the help of materials and energy. Benchmark 10-year yields are mostly firmer, though the US yield remains below 2.60% after disappointing industrial output/manufacturing production were reported before the weekend. The dollar is softer against most of the major currencies, with the yen and sterling struggling to stay positive, while the Antipodeans lead the way. Iron ore prices rose 3% on supply concerns following Vale’s output cut announcement. |

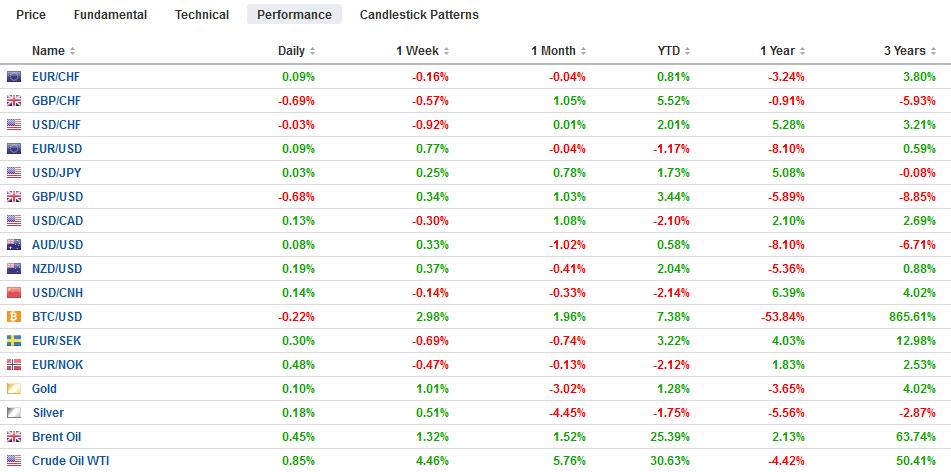

FX Performance, March 18 - Click to enlarge |

Asia Pacific

The anticipated meeting between the US and Chinese presidents that was hoped for the end of this month is now looking like May or June as the next possible window. The talks have produced more than a 100-page document. The innovation is thought to be the enforcement mechanism that moves away from the traditional mechanism of an independent panel to adjudicate. Instead, if a conflict cannot be resolved by official negotiations, the US reserves the right to retaliate proportionately.

After seasonal adjustments, Japan reported its first trade surplus since last June. The February surplus of JPY116 bln was about a third larger than expected. It was recorded despite a larger than expected fall in exports (-1.2%). It was the third month that exports fell on a year-over-year basis. Autos and semiconductors were the main culprits. The 14% decline in exports to South Korea, including a 60% drop in chipmaking equipment plays on fears of the slowing of the tech cycle. The source of improvement of the trade balance came from a 6.7% decline in imports after a revised 0.8% decline in January (initially -0.6%).

Singapore is a commercial hub, and its economic performance often is looked at for regional trends. It reported 16% in non-oil exports in February, snapping a three-month slide. The median Bloomberg survey forecast was for a 4.3% increase. However, electronic exports fell 8%, which is half the pace seen in January (-15.9%). Non-oil exports rose 4.9% year-over-year after a 10.1% decline in January.

Four Asian central banks meet this week: the Philippines, Indonesia, Thailand, and Taiwan. None are expected to change policy. The Australian dollar is extending its recovery. It successfully held above $0.7000 earlier this month and today has traded to $0.7120. The 20-day moving average is near $0.7100, and the Aussie has not closed above it this month. The next objective is near $0.7150. The dollar has been confined to less than a quarter of a yen range through the European morning. There are a little more than a billion dollars in options struck between JPY111.55 and JPY111.60 that expire today. The Indian rupee is the strongest currency in the world today, rising 0.8% against the dollar. The greenback is at its lowest level since August 2018. Optimism about the trajectory of the economy and the election continues to draw foreign interest in the equity market.

Europe

UK Prime Minister May wants the Withdrawal Bill to get another hearing before she heads up to the EC Summit with hat in hand, hoping the terms of extension are not too onerous. Indeed, May has signaled an unwillingness to submit the Withdrawal Bill again unless there is a greater chance of passing. The third vote looks likely to get more than it did in the first two attempts. The prospects of a long extension are being depicted as a likely reversal of the 2016 non-binding referendum. More than three dozen MPs that support Brexit have reportedly offered to support the Withdrawal Bill provided May resigns next month.

The potential combination of Deutsche Bank and Commerzbank have long been rumored, and now it is official. Talks are underway. In some ways, this illustrates several underlying weakness in Europe. First, the merger of two weak domestic banks is not an obvious way to make a strong bank. Second, the union representatives on both boards are opposed. An estimated 20k-30k jobs could be lost in combination. The Social Democrat finance minister has agreed not to object, which seems to be another step of the SPD away from its labor roots. In the latest polls, the SPD continues to run well behind the CDU and is threatening to slip in third place nationally behind the Greens. Third, by trying to make a “national champions,” an opportunity is forgone to make EU champions.

IG Metall, one of the largest and most important unions in Germany, appears to have reached a settlement for its 72k members. A 3.7% pay increase was secured and an extra 1000 euros a year this year and next, that could be swapped for five days of paid leave. Although pattern bargaining has waned in Germany in recent years, other negotiations may still be compared with these results. Separately, Germany is going forward with its 5G auction starting tomorrow, while Switzerland has become the latest European country to push back against US demands to ban Huawei.

The euro is rising for the sixth of seven sessions since the ECB’s pessimism briefly drove the single currency to its lowest level since the middle of last year. Disappointing US data (job growth on March 8 and industrial/manufacturing output on March 15) helped spur the short-covering rally. It reached $1.1350 in the European morning, its best level since March 4. We continue to look for a test on the middle of the old $1.13-$1.15 range. Only a break of $1.1280 would undermine this near-term constructive outlook. Sterling is trading within the pre-weekend range (~$1.3200-$1.3300). Sterling has risen against the dollar for the past three months, which is the longest streak since 2012. It is virtually flat here March.

America

The economic calendar is light in North America today. Canada reports January portfolio flows following foreigners record bond sales in December. Canadian political scandals are somewhat unique. Prime Minister Trudeau is not in trouble for illegal activity but rather using the power of his office to influence a judicial matter. He is expected to announce a cabinet reshuffle later today.

The FOMC meeting is the highlight of the week. No one expects a change in policy. However, everyone is looking for a further shift in the dot plot. There is some talk that former Fed Chair Bernanke told a private audience that he expects the median dot to be lowered to no change this year from two hikes anticipated in December. It is difficult to argue against him, but 11 officials saw 2-3 hikes this year, and it may be a challenge for these to be completely unwound based on the economic data. Moreover, financial conditions have unwound the Q4 tightening and yields remain lower.

The Canadian dollar is trading inside the pre-weekend range. The 20-day moving average (~CAD1.3285) offers support. The US dollar has not closed below it this month. The prospects that the Bank of Canada adopts an easier bias after the recent string of disappointing data may help underpin the greenback. Initial resistance is seen near CAD1.3380. The Mexican peso is at its best level this month, as the dollar slipped through MXN19.20. Trendline support is seen near MXN19.10. The Dollar Index is holding just above last week’s lows. The 96.25 area may offer mild support, while the low from the end of February around 95.80 is more significant.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$AUD,$CAD $GBP,$EUR,$JPY,EUR/CHF and USD/CHF,MXN,newsletter