Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.10% at 1.1262 |

EUR/CHF and USD/CHF, November 28(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Global capital markets are relatively calm as investors gird for drama. The Bank of England reports its assessment of the impact of Brexit and the stress tests a little before Fed Chair Powell speaks at midday in NY. The G20 meeting begins Friday, and several bilateral meetings are taking the spotlight from the larger gathering. Asian equities advanced for a second consecutive session, with Greater China markets (China, Hong Kong, and Taiwan) and Japan’s Nikkei were up more than 1%. European shares are struggling to maintain the early upside momentum, and US shares are little changed. Benchmark 10-year yields are mostly 1-2 basis points lower, while oil and industrial metals are firmer. The dollar is in narrow ranges but mostly holding on to yesterday’s gains against most of the major currencies. The Australian and New Zealand dollars continue to outperform. |

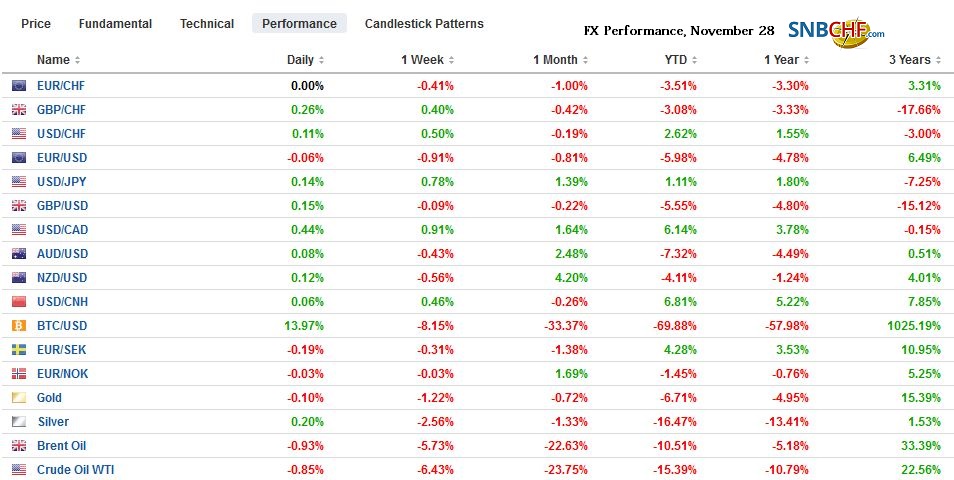

FX Performance, November 28 - Click to enlarge |

Asia Pacific

Presidents Trump and Xi will have dinner Saturday night. China’s Vice Premier Liu reiterated the pledge that China will open its markets. Most observers seem to agree that China is, in fact, doing this, but the issue is really the speed, not the direction. US economic adviser Kudlow says that Trump wants to make a deal but that China is not offering enough. It begs the question: Could China offer enough? The US criticism of China extends well beyond trade and commerce. The US appears to be demanding the end of Made in China 2025, which does not seem that different than the US import substitution strategy that is partly dressed up in America First. The US also objects to China’s One Belt One Road initiative.

There has been structured bilateral talks between the US and China under the past two US presidents, which were ended by the Trump Administration. A resumption of regular talks with China will likely be greeted as a success if agreed this weekend, but it simply returns the situation to the status quo ante. The real question after the G20 meeting is whether the US will go ahead with raising the 10% tariff on $200 bln of Chinese goods to 25% at the beginning of 2019 and if it signals the start of the process to levy a new tariff on the remaining roughly $265 bln of Chinese imports.

The dollar reached two-week highs against the yen (~JPY113.90) and Chinese yuan (~CNY6.9580). The greenback has been confined to less than a quarter of yen range through the European morning. There are chunky options set to expire today. These include $1.9 bln at JPY114.00, $777 mln at JPY113.70-80, and $2.33 bln at JPY113.50-55. The options market the yuan shows the biggest discount for one-week dollar calls over puts (25-delta risk reversal). Meanwhile, the Australian and New Zealand dollars are firm but within yesterday’s ranges.

Europe

The ECB reported money supply growth unexpectedly accelerated to 3.9% in October from a 3.6% pace in September. Household lending increased, but loans to non-financial businesses did not. Those are aggregate numbers, and there is much variance among the members. The most important report this week is the flash CPI for November, and it is due out ahead of the weekend. The headline is expected to slip (2.0% from 2.2%) while the core rate is forecast to be steady (1.1%).

Brexit remains front and center today. Toward the end of the European session, the Bank of England will share its assessment of the economic and fiscal impact of Brexit. Both sides in the debate will look to use it for their own purposes. At the same time, the results of the BOE stress test will be reported. BOE Governor Carney will hold a press briefing that will likely carry over into the beginning of Powell’s lunchtime address in NY.

Prime Minister May strategically retreated yesterday and will allow Parliament to attach amendments to the Withdrawal Bill that could include a second referendum, or insist on a customs union. Reports suggest that nearly 100 Tory MPs have publicly indicated their opposition as has the Democrat Unionist Party from Northern Ireland. The debate in Parliament will formally begin December 4 and last five days with a break December 7-9. A vote is planned for the London evening on December 11.

The euro is lower for the fourth consecutive session and reached a two-week low just above $1.1265. The low for the year was set earlier this month near $1.1215. There are nearly one billion euros in options between $1.1280 and $1.1300 that are expiring today. The intraday technical indicators suggest that the low may be in for the session. A move above $1.1300 could see a range extension toward $1.1340. For its part, sterling held above yesterday’s lows (~$1.2725) but remains well below yesterday’s highs ($1.2830). Although sterling firmed during the European morning, yesterday’s highs seem a bridge too far. The roughly GBP730 mln in expiring options in the $1.2775-$1.2800 area may check the gains.

North America

There will be several US economic reports before Powell speaks. The US advanced merchandise trade balance for October will be released, and some modest deterioration is expected. Some observers attribute the widening trade deficit to the strong dollar, but surely growth differentials, especially given the US fiscal stimulus is playing a role. Also, there is an attempt to stockpile Chinese goods ahead of more tariffs. This sets the stage for a reversal (US imports and Chinese exports) early next year. While economists will use the trade figures to fine-tune Q4 GDP estimates, the US will publish revisions to Q3 GDP. They are expected to be minor. The US reports October new home sales, and after a falling for four consecutive months, many are looking for a bounce. However, traders will likely look past the gain if it is largely a reflection of the recovery from Hurricane Florence. The EIA’s oil inventory estimate will be watched closely after the API reported an unexpected 3.45 mln barrel build. The Bloomberg survey found a median expectation for a less than a 600k barrel increase in the EIA’s figures.

President Trump continued with bombastic attacks on the Federal Reserve, inexplicably claiming that it is a bigger problem than China. The market is convinced that the seeming encroachment on the Fed’s independence will not impact policy. Powell is expected to offer a balanced view of the US economy, as he did in Dallas recently. There is a reason why the Fed’s risk assessment is balanced, even though Clarida said yesterday that the risk is less skewed to the downside. With the Fed funds target below the inflation rate and growth above trend, there is little reason not to continue to raise rates gradually. Some pundits played up the number of times that Clarida used the phrase “data dependent,” which incidentally was his topic. The 2019 Fed funds futures strip was unchanged yesterday, suggesting Clarida did not change expectations. More of the same from Powell is the most likely scenario.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$EUR,$JPY,EUR/CHF,FX Daily,newsletter,USD/CHF,yuan