Jeffrey P. Snider

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

In December 2006, just weeks before the outbreak of “unforeseen” crisis, then-Federal Reserve Chairman Ben Bernanke discussed the breathtaking advance of China’s economy. He was in Beijing for a monetary conference, and the unofficial theme of his speech, as I read it, was “you can do better.” While economic gains were substantial, he said, they were uneven.

To keep China going down the same path of rapid growth, Bernanke advised, as all Economists do, to stop undervaluing their currency. According to the mainstream view, the one taken from his “global savings glut”, CNY’s trade-weighted effective real exchange value had declined about 10% in about five years to that point.

Even though the PBOC had finally allowed a limited float for the value, Bernanke and Western Economists always wanted more. Not just for Western interests, but for the Chinese, as well.

Greater scope for market forces to determine the value of the RMB would also reduce an important distortion in the Chinese economy, namely, the effective subsidy that an undervalued currency provides for Chinese firms that focus on exporting rather than producing for the domestic market. A decrease in this effective subsidy would induce more firms to gear production toward the home market, benefiting domestic consumers and firms.

In other words, if Communist officials would just let CNY rise to its presumed equilibrium, voila, economic rebalancing and harmony around the entire global economy. He even counseled the Chinese people to save less, Economists hating savings in favor of unrestrained spending every time.

Over the next seven years, the first part happened or at least started to. CNY did rise, but not because of trade mechanics or some newfound spirit of fairness. It was that “global savings glut”, really eurodollar “hot money”, that pushed the exchange value upward against the dollar. Even in late 2013 when it finally peaked, there was practically no one who saw any danger of a reverse; and therefore the dangers arising from going in reverse.

If there was a big risk in his estimation, Bernanke was at least thinking ahead even if he really had no realistic basis for his opinions.

The United States must also do its part, in particular by increasing its own rate of national saving and by avoiding protectionism. With greater integration come greater interdependence and greater responsibility.

True, but again why? What was the specific agent of interdependence and integration? Bernanke would prove over and over during the chaos of his tenure he didn’t really know.

| Protectionism is an indirect consequence of getting monetary policy wrong for so long. To begin with, there isn’t any money in the Federal Reserve’s application of it. Hard to argue exchange mechanics without anything of value to exchange. It’s only after more than a decade of global economic suffering that everyone-for-themselves is finally starting to appear.

First comes prolonged stagnation, then politics. China’s real risk has always been eurodollars. Far from a savings glut, the Chinese system suffers from another looming “dollar” squeeze. In many ways, the last one never really ended. |

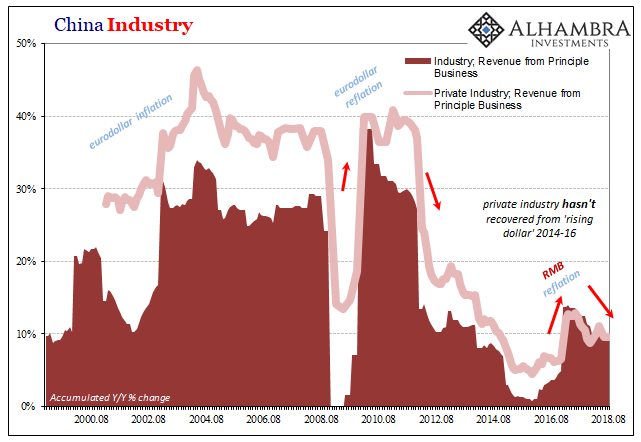

China Industry Revenue, Aug 2008 - 2018 - Click to enlarge |

| While they keep talking about, and waiting for, rebalancing, China’s industry continues to be the dominant global economic force. Unfortunately for the world, global trade is right where monetary problems strike first. Chinese industry has been slowing down again all year, particularly on the private side. |

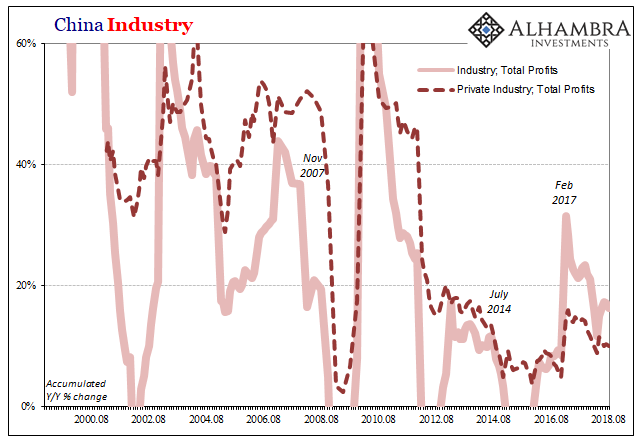

China Industry Profits, Aug 2000 - 2018 - Click to enlarge |

| China’s National Bureau of Statistics reports that in August 2018 accumulated (YTD Y/Y) profits at all industrial firms (above standard size) rose 16.2%. On a month-by-month basis, profits were up just 9.4% from August 2017. That’s the lowest increase (outside of Golden Week distortions in March) since December 2016. Rolling over.

In terms of industrial revenue, top line growth was 9.8% on an accumulated basis, down from 9.9% in July; on a monthly basis, revenue grew by 9.3% above August 2017, down from 9.7% in July. |

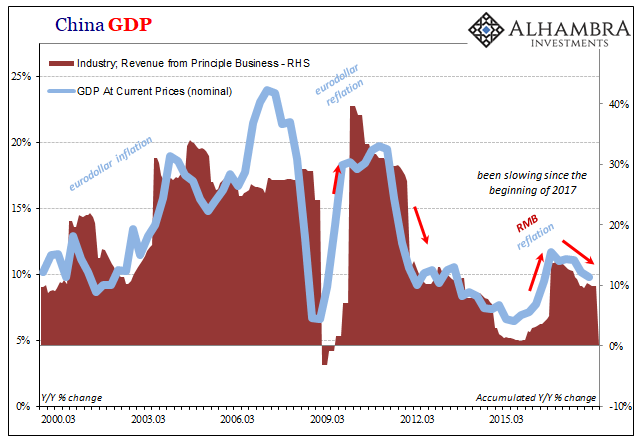

China Industry Revenue Nominal GDP, March 2000 - 2018 - Click to enlarge |

| Compared to levels reached when Bernanke was speaking in Beijing almost twelve years ago, China’s industrial economy has come to a screeching halt. It certainly wasn’t protectionism that stomped on the brakes, nor was it the persistently high savings rate for the Chinese people. The former Fed Chairman was right about the currency but for all the wrong reasons.

What happened to last year’s globally synchronized growth? It wasn’t really ever that much growth to begin with, China’s industrial firms demonstrating the hype better than anyone. Underneath it all the whole time were the same inherent flaws that in December 2006 (inverted eurodollar curve, for one) were only beginning to show. Twelve years later, growth is gone and they still have no idea why. Bernanke to this day still talks about a global savings glut. He now says it may have moderated. There’s nothing moderate about it, or him. |

China Industry CNY RRR, Jan 2000 - Aug 2018 - Click to enlarge |

China Industry CNY Ind Rev, Jan 2000 - Sep 2018 - Click to enlarge |

|

PBOC Currency, Aug 2007 - 2018 - Click to enlarge |

Tags: $CNY,Ben Bernanke,China,currencies,economy,EuroDollar,eurodollar system,exports,Federal Reserve/Monetary Policy,global trade,industrial profits,industry,Markets,money,newsletter