Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

What Did Hamper Growth ‘In A Few Months’

What Did Hamper Growth ‘In A Few Months’18 Dec 2020

With No Second Half Rebound, Confirming The Squeeze29 Jan 2020

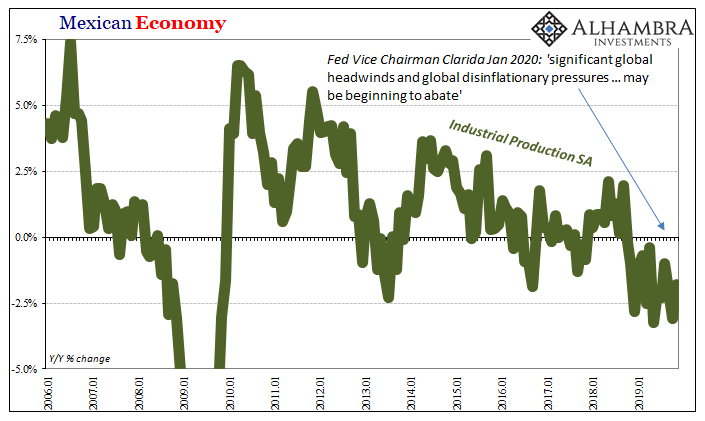

Not Abating, Not By A Longshot14 Jan 2020

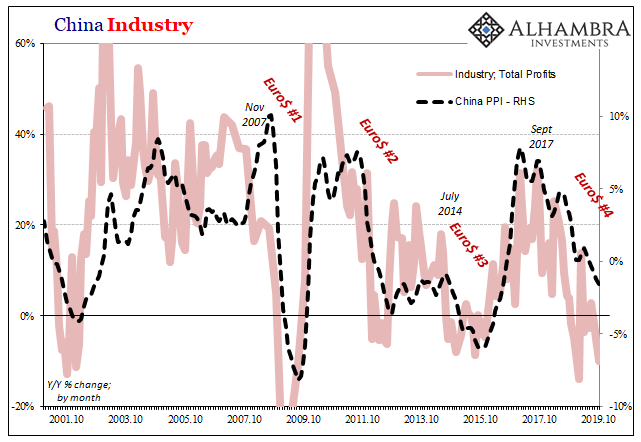

Nothing Good From A Chinese Industrial Recession30 Nov 2019

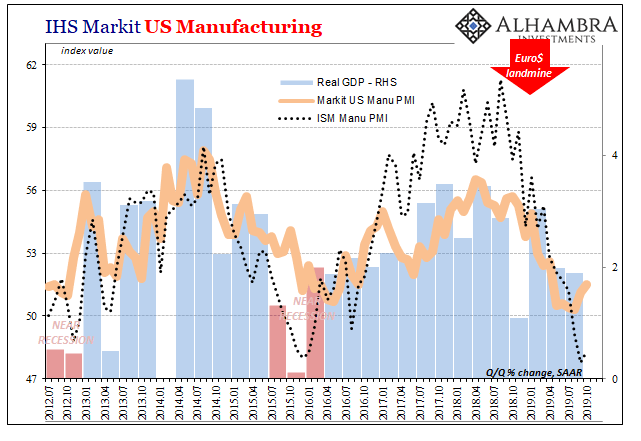

Still Stuck In Between9 Nov 2019

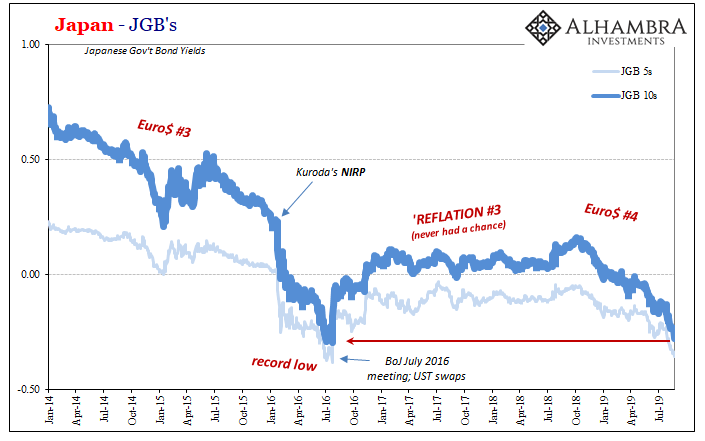

Japan: Fall Like Germany, Or Give Hope To The Rest of the World?29 Aug 2019

Green Shoot or Domestic Stall?17 Apr 2019

Slump, Downturn, Recession; All Add Up To Sideways22 Mar 2019

Meanwhile, Over In Asia2 Mar 2019

Industrial Fading19 Dec 2018

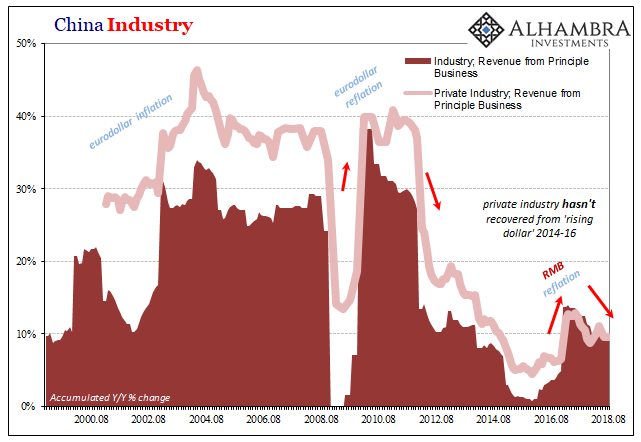

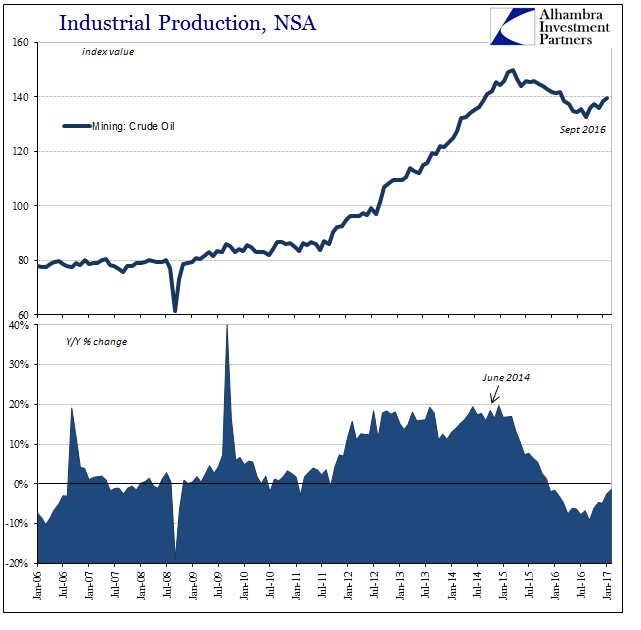

China’s Industrial Dollar3 Oct 2018

Globally Synchronized Asynchronous Growth26 May 2018

The Dismal Boom25 Jan 2018

Industrial production: The Chinese Appear To Be Rushed4 Jan 2018

The Economy Likes Its IP Less Lumpy23 Dec 2017

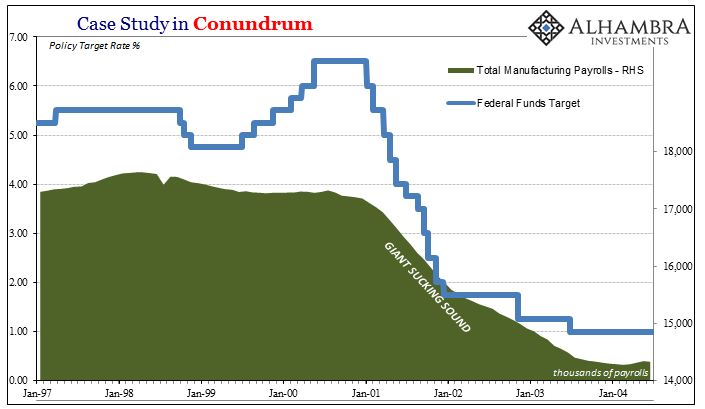

Giant Sucking Sound Sucks (Far) More Than US Industry Now11 Dec 2017

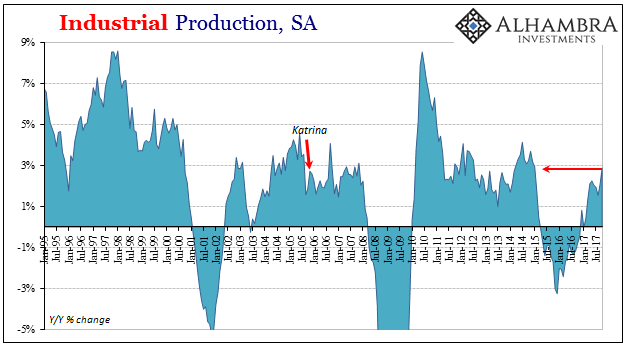

Industrial Production Still Reflating20 Nov 2017

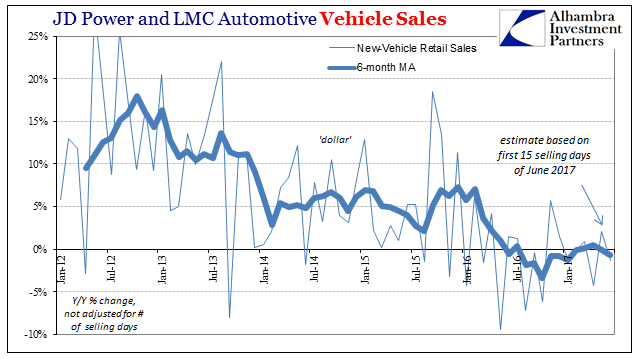

Vehicle Sales, Consumer Price Index and Average Weekly Hours: More Than Minor Auto Potential11 Jul 2017

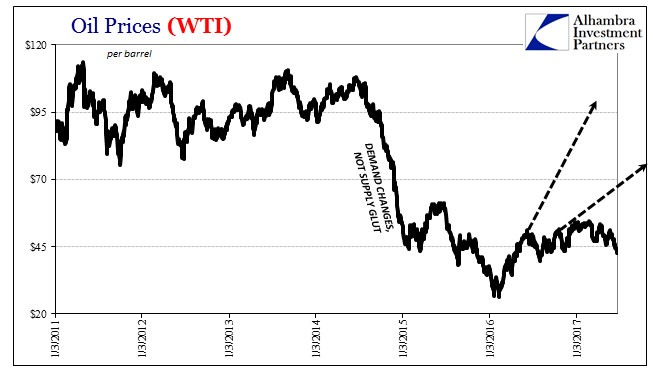

Oil Prices and Manufacturing PMI: No Backing Sentiment4 Jul 2017

Commodity and Oil Prices: Staying Suck24 May 2017