Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

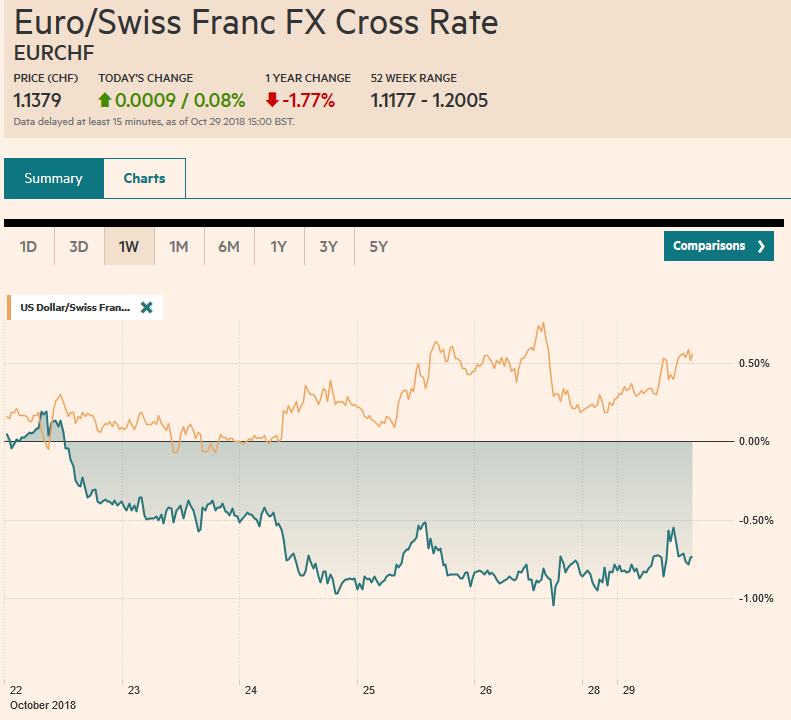

Swiss FrancThe Euro has risen by 0.08% at 1.1379 |

EUR/CHF and USD/CHF, October 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe Dollar index is trading within last Friday’s trading ranges. The year’s high, set on August 15, was just shy of 97.00. The euro continues to straddle the $1.14 level but is spending more time in Europe below there. There is a 1.5 bln euro option expiring today at $1.1350 and an almost 600 mln euro option at $1.1400 that will be cut. The dollar has been confined to about a 20 pip range on either side of JPY112, where an $885 mln option is expiring today. There are roughly $2 bln in options struck JPY112.65-JPY112.70 that also expire today. Sterling is flat around $1.2825 with practically no momentum. The dollar-bloc currencies are firm, but only the New Zealand dollar is showing any enthusiasm. It is the strongest currency today, gaining about 0.7% to return to the $0.6550 area after spiking to $0.6465 before the weekend. |

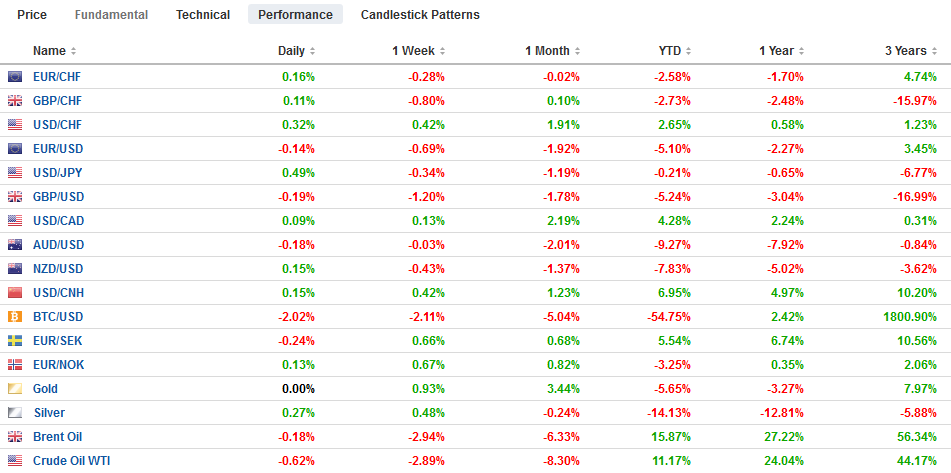

FX Performance, October 29 - Click to enlarge |

Overview: The capital markets appear to be waiting for US leadership for direction. The dollar is mostly slightly firmer against the major currencies, though the dollar bloc is firm. Among emerging market currencies mixed, though the high beta Turkish lira and South African rand are posting modest gains. The weakest is the Mexican peso. It is off about 1.5% as the market responds to news that Mexican voters preferred, by a clear majority (~70%), upgrading the existing international airport rather than building a new one in Mexico City. Many large equity markets in Asia eased, but the rout in China continued to a 2% drop and South Korea’s Kospi eased 1.5%. India, Australia, Hong Kong, and several smaller bourses edged higher. European bourses were firmer, led by Italy (~1.3%). The Dow Jones Stoxx 600 was up about 0.5% near midday. Interest rates are.lower. A less than hawkish central bank of Korea saw the 10-year benchmark yield fall eight basis points. The move was matched in Europe by Italy. Core European yields are slightly lower, while the periphery is outperforming. US 10-year yields are pinned near last week’s low near 3.05%, as US stocks trade with a heavier bias in Europe.

China

Many investors expect Chinese officials to take more steps, including reducing interest rates, to support the economy. In addition to the focus on the domestic policy response to the equity market slide and economic slowdown, the trade conflict with the US is set to intensify. First, while Trump and Xi may still meet at the end of next month on the sidelines of the G20 meeting, reports suggest the White House may take trade off the agenda. Second, the WTO dispute settlement body will hear US charges on China’s violation of intellectual property rights today. Third, the 10% tariff on $200 bln of Chinese goods is still set to increase to 25% as on January 1.

There are three main stories from Europe today. First, S&P kept Italy’s rating at BBB, two steps into investment grade, but shifted the outlook to negative from stable. This was very much in line with expectations and reinforces our idea that Italy is not on the verge of losing this status. Still, investors have responded favorably to this and to some signals from Italy’s Prime Minister Conte that there may be some flexibility within the government. Specifically, he seemed to suggest that the tax cuts be implemented quickly (League) but that the citizen’s income (Five Star Movement) and the pension reform (both) could have a later implementation. Separately, Italy will sell nine billion bills and notes this week, testing the market’s appetite.

United Kingdom

Second, UK’s Hammond will unveil the new budget proposals. He is expected to bring forward tax cuts and introduce more public spending. However, it all appears at the mercy of Brexit and whether an agreement is struck. Remember, investors continue to handicap three scenarios: A soft Brexit that keeps the UK closer for longer with the EU. A hard Brexit which is a more complete break from the EU. A Brexit with no agreement is not just another version of a hard Brexit, but it would not most disruptive and would not include a transition period.

Germany

The third development is German politics. The main political parties continued to see their support erode in Hesse. However, the outcome was not quite as poor as had been feared. The current coalition of the CDU and Greens appear to have held on to the slimmest of majorities. Still, there will be a price to be paid. The Social Democrats want to shake up the national coalition and set specific goals for the next six months (into the run-up of the European Parliament elections) and reviewed the coalition then. Merkel, who faces a leadership challenge at the CDU convention in December, has indicated she will not seek re-election. She will remain Chancellor.

United States

US Q3 GDP report before the weekend steals the thunder from today’s personal income and consumption data. The GDP report showed that the quarterly core PCE deflator slowed to 1.6% from 2.1%. Economists had expected the monthly core PCE deflator to remains steady at 2.0%, the Fed’s target. The data highlight for the week includes auto sales and the employment report. After weather-induced weakness in September, non-farm payrolls are expected to have recovered toward the recent averages, while the base effect could see hourly earnings jump over 3% from a year ago.

Canada’s economic calendar begins off light this week, but tomorrow is the August GDP. Canada also reports jobs and trade at the end of the week.

Brazil’s Bolsonaro was elected president in the second round yesterday. Brazilian equities and currency have rallied on expectations of his victory, but are expected to benefit from follow-through interest The US dollar finished last week just above the 200-day moving average which is found near BRL3.6340. The next big chart point is seen near BRL3.54. The Mexican peso is going in the opposite direction. The US dollar has popped through last month’s high near MXN19.6860 in thin turnover in Asia, but a move through there in when the domestic market opens signals a test on MXN19.80-MXN20.00

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,brl,EUR/CHF,newsletter,USD/CHF